1. Higher for Risk Assets

Prediction:

- S&P 500 hits 8,000

- Bitcoin tags $200,000

- U.S. rates glide to ~3.5%

- Drivers: liquidity, ETF/halving tailwinds, and post-2022 reflexivity

What happened:

- Bitcoin (~$90k): It’s doubled off the lows but fell short of escape velocity. The halving and ETF flows helped, but the market ran out of breath somewhere in the $90Ks. So far, this looks more like a slow grind than a euphoric melt-up.

- S&P 500 (~6,950): A solid year, but not the face-melting rally that 8,000 implied. Investors are still feeling around in the fog — bullish, but not brave. Every bounce seems to come with a foot on the brake.

- Fed Funds (~3.25%): A rare case of the glidepath going to plan. Short rates have eased more or less as expected even if mortgage rates are still stuck in the 6s, putting a lid on rate-sensitive risk. Call this one a quiet win.

- Liquidity (tempered): The juice has been there, just not the squeeze. Flows have stabilised markets, but we haven’t seen the self-reinforcing upside that reflexivity promised. Every rally meets resistance — not disbelief, but caution.

Outcome: Partial miss ❌

The structure was right, the scale was off. Risk assets are higher, but the rally hasn’t gone reflexive — at least not yet and not for broader crypto assets.

2. Solana

Prediction:

- Non‑vote TPS >1,500 by end‑2025

- On‑chain app revenue breaks all‑time records

- U.S.‑listed Solana ETF launches with Ethereum‑level inflows

What happened:

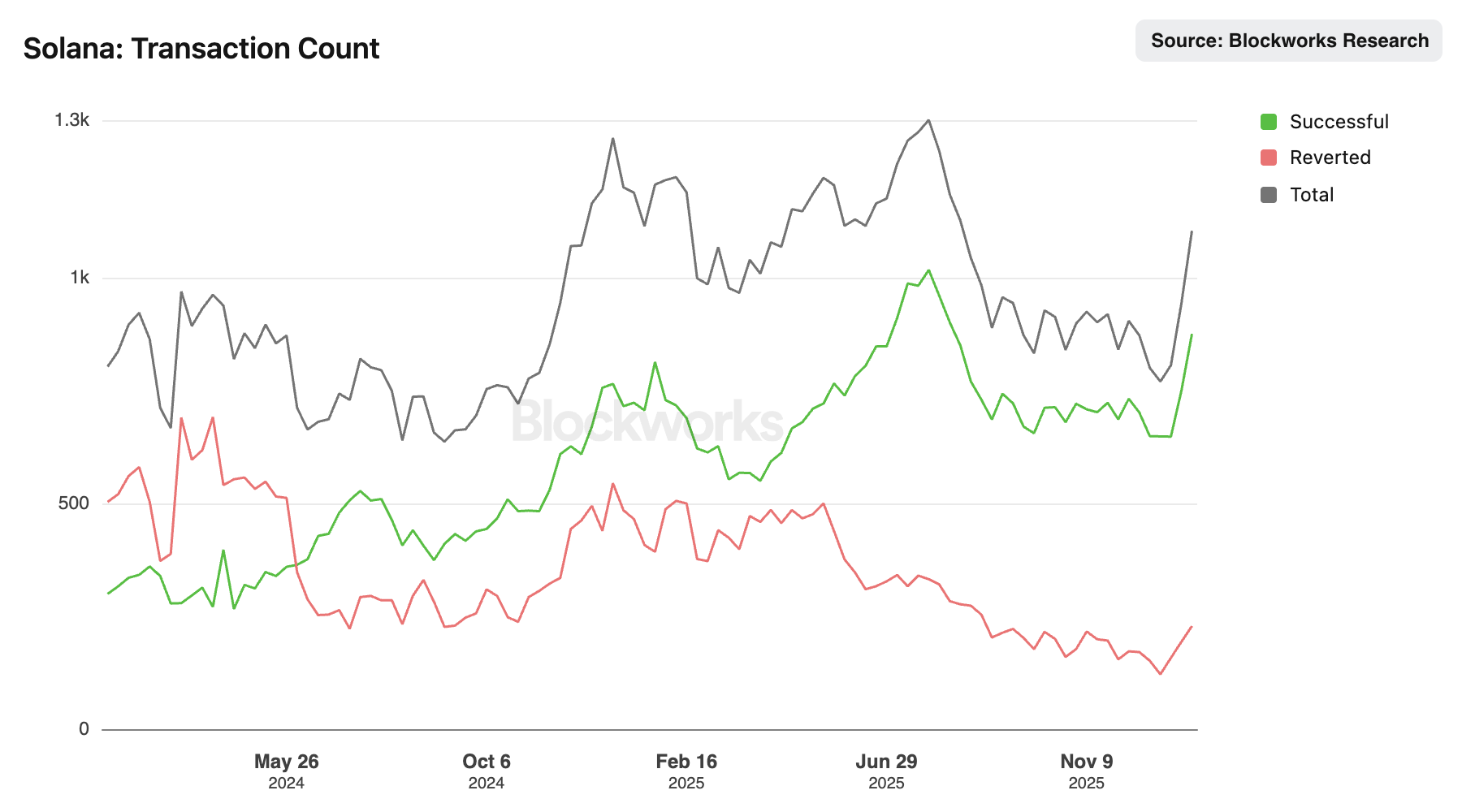

- Transaction Throughput (Non‑vote TPS ~1,000): Solana never quite hit a sustained 1,500 non‑vote TPS, but it’s consistently sat near ~1,000 with sporadic spikes above that mark, sometimes well above. That puts the prediction directionally right but shy of the specific target. More importantly, the network’s success rate has improved and failure rates fallen, so throughput isn’t just high, it’s reliable on real‑world workloads.

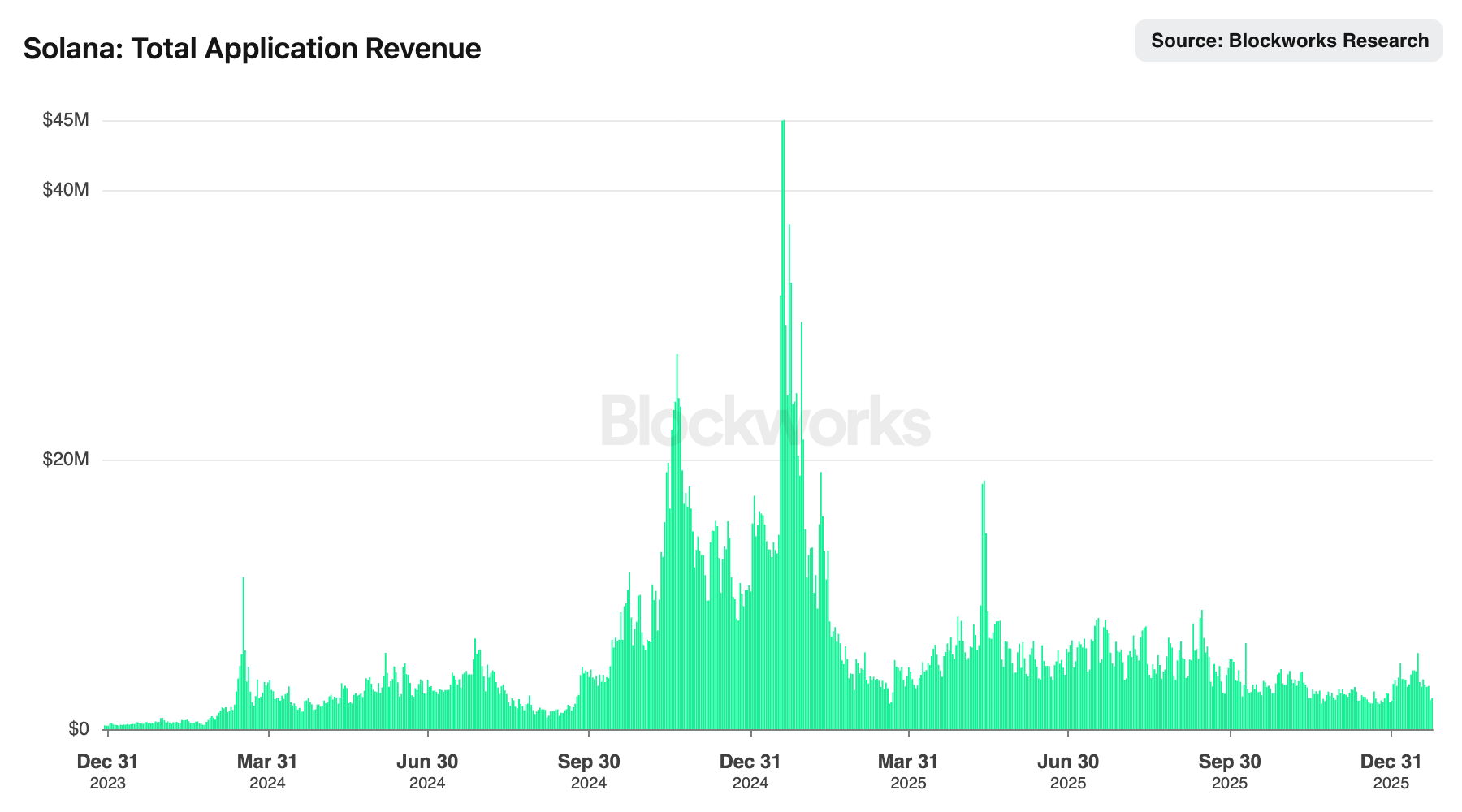

- App Revenue ($2.36B in 2025): Solana didn’t break its all-time daily revenue record — the $54.3M high still stands — and the top day in 2025 came in around $18M. So on a technical level, that’s a miss. But annual revenue tells a different story: $2.36B in 2025, up >40% from $1.64B in 2024, as more apps printed more consistently and pushed beyond the meme-shaped use cases that defined prior cycles.

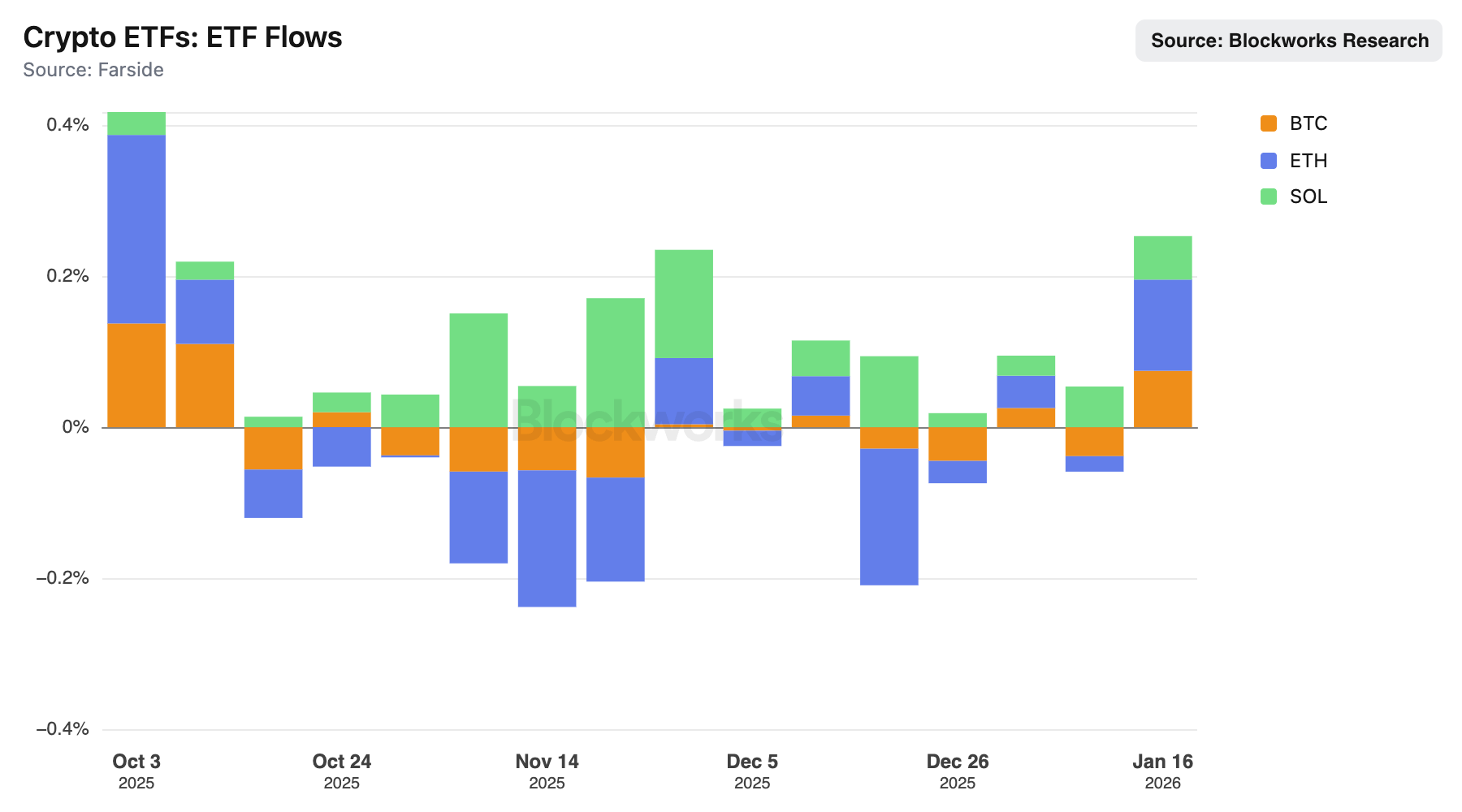

- ETF Inflows (rivaling ETH): The prediction landed smack in late October, when Bitwise launched its SOL ETF — a product that has, until just last week, consistently outperformed both BTC and ETH ETFs on a market cap–adjusted basis. Flows remained net positive through January, with weekly inflows peaking near $500M and daily contributions from products like Fidelity’s FSOL keeping the momentum up. Whether the recent pause marks a plateau or just a breather remains to be seen, but Solana’s arrival in the ETF era is no longer a hypothetical — it’s happened, and it's working.

Outcome: Strong hit ✅

While it didn’t clear the non-vote TPS target on a sustained basis, it came close — and did so with resilience that would’ve been unthinkable a year prior. App revenue didn’t break daily records, but annual growth was undeniable. ETF performance hit squarely, with Bitwise’s product outperforming BTC and ETH on a per-MC basis until just last week. Across infrastructure, usage, and institutional access, Solana didn’t just meet the moment — it exceeded it.

3. ETFs

Prediction:

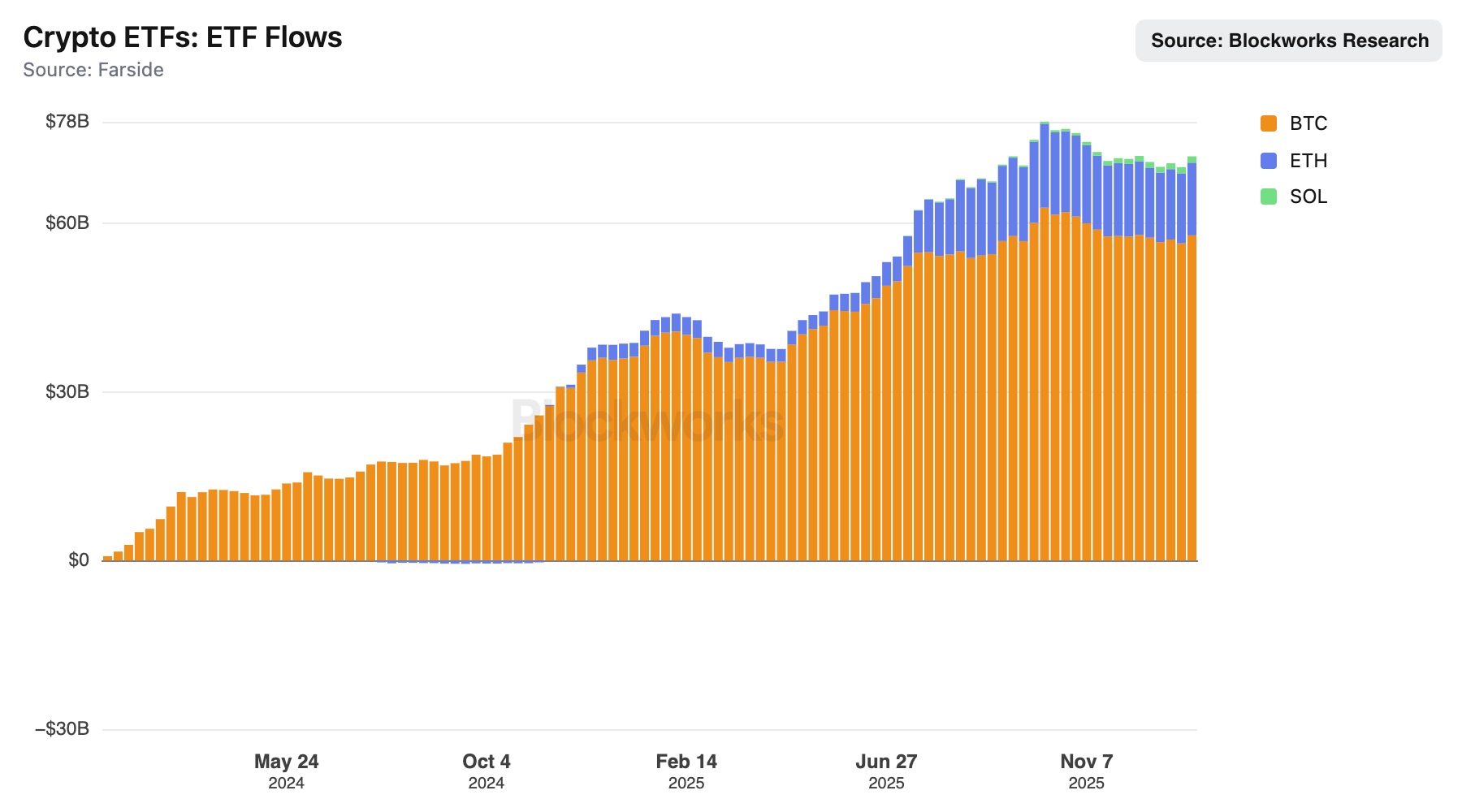

- U.S. crypto ETF count doubles to >50 products

- Includes spot BTC/ETH/SOL, multi-asset, staking, and thematic offerings

What happened:

- Product Count (100+ registered): The prediction hit right on the nose and then some. There are now over 100 crypto ETFs registered in the U.S., spanning spot Bitcoin and Ethereum, futures-based products, Solana and XRP exposure, as well as broader crypto industry funds. The menu is full and growing with a crowded 2026 pipeline suggesting the expansion isn’t slowing down.

- Institutional Flow (Net Positive): Flows have been broadly constructive, especially given the backdrop. SOL ETFs have outperformed on a per-market-cap basis, while BTC and ETH products remain steady allocation vehicles. Institutional appetite is no longer theoretical — it’s moving capital.

Outcome: Strong hit ✅

The prediction called both the breadth and direction of the trend. Crypto ETFs are no longer waiting at the gates — they’re flooding in.

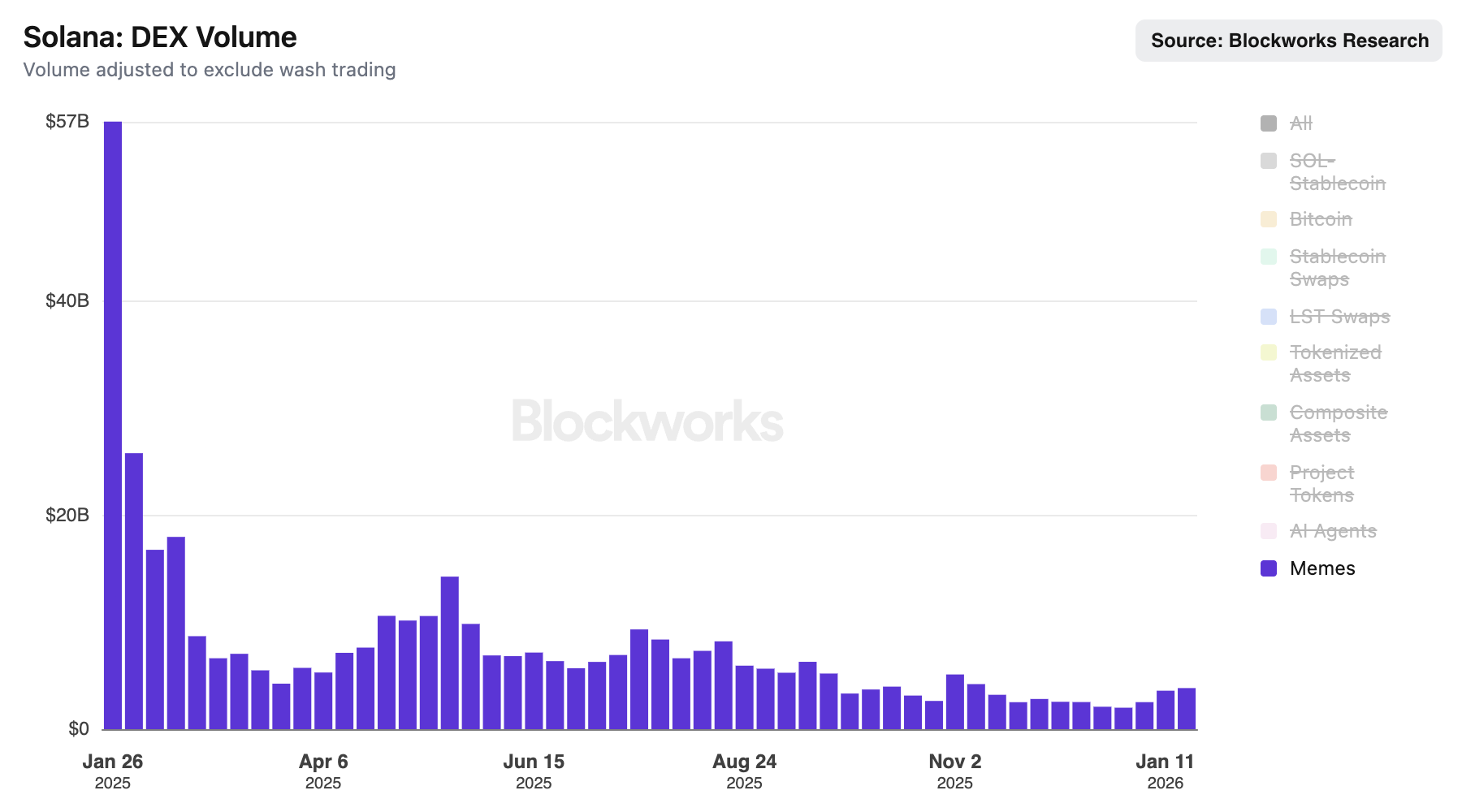

4. Memecoins Come Back in Style

Prediction:

- Aggregate memecoin market cap breaks $200B before Q1 2026

- DOGE and PENGU ETFs approved

- PumpSwap (or similar) DEX volumes 10x to $5B+ daily peaks

What happened:

- Market Cap (~$47B): No bid, no bounce. Just a twitch in the rubble. The memecoin space remains devastated, with total cap stuck well below prior highs and miles from the $200B mark. A brief blip in early 2026 didn’t change the broader picture: sentiment is shot, and most of the momentum traders have moved on.

- ETF Approvals (DOGE yes, PENGU tbd): DOGE got its ticker. The SEC approved a Nasdaq-listed ETF backed by 21Shares and the Dogecoin Foundation, which now trades with all the seriousness that only irony can command. PENGU, meanwhile, is still in meme purgatory — no approval, no momentum, no signal.

- PumpSwap Volumes ($1.28B daily peak): PumpSwap flirted with the forecast but didn’t marry it. Daily volumes peaked at $1.28B, weekly hit $6.6B, but it never sustained the $5B+ rhythm predicted. The Solana memecoin craze gave it a jolt, not a trend.

Outcome: Total miss ❌

DOGE got its suit and tie, but the rest of the space stayed in pajamas. Volume flared, capital fled, and the $200B target is still a distant dream, if anyone’s still dreaming.

5. DePIN

Prediction:

- Monthly sector revenue clears $100M by February 2026 (~5x from then-current levels)

- Energy and solar projects lead the charge

What happened:

- Revenue (~$100M a year, not a month): The $100M/month goal hasn't been confirmed. Yet, Helium alone is starting to carry real weight. Daily revenues rose sharply in the back half of 2025, peaking north of $70K/day and holding a ~$60K/day run rate for months - that’s ~$1.8M/month from just one DePIN project. Add Geodnet’s $700K/month and others we can’t yet fully track, and it’s clear: the sector hasn’t hit the mark, but it’s warming up. Fast.

- Energy Adoption & Fundraising (No revenue, but real money): The energy vertical didn’t lead in revenue but it did lead in capital raised and mindshare. Fuse Energy pulled in $70M at a ~$5B valuation, while Daylight secured a $75M round led by Framework Ventures. That’s not nothing. It’s serious money backing real infrastructure plays — even if monetisation still feels like a later-stage conversation.

- Adoption (Getting there, slowly): You can feel the energy — DePIN is where crypto meets real-world infrastructure — but most of the current traction is about potential, not throughput. Verifiable usage data is thin. We’re still in the promise stage of the product cycle.

Outcome: Ongoing / miss ❌

The thesis is still breathing, but the benchmark wasn’t hit. Plenty of noise, not enough numbers — for now, DePIN is still running on hope and inflation.

6. Decentralized Compute

Prediction:

- Render, Akash, io.net, etc. collectively 10x revenue by February 2026

- Growth fuelled by surging AI inference demand and spillover from centralized bottlenecks

What happened:

- Revenue (io.net ~$20M run rate, per reporting): io.net has reportedly reached a $20M annualised revenue pace by late 2025 — a sharp jump from its earlier ~$2M baseline. But without full transparency or confirmation from other players, that alone doesn’t carry the 10x call across the sector. The data’s partial, the figures uneven, and the weight of the proof still feels light.

- Capacity & Growth (Akash +700% GPU supply): Akash expanded its GPU supply by more than 700% since 2023, which is impressive — but more a supply-side story than a revenue one. Infrastructure is being laid, but the monetisation curve hasn’t steepened yet. Scaling, yes — returns, not yet.

- Aggregate Data (Still foggy): We’re flying blind on consolidated revenue numbers. Render, Akash, and others haven’t put forward detailed disclosures, and what’s visible doesn’t add up to a confirmed 10x. Demand is there, interest is rising — but the receipts aren’t.

Outcome: Miss ❌

There’s plenty of momentum and a compelling narrative, but the hard numbers didn’t materialize. The sector’s building but the revenue’s still buffering, and the tokens have been flushed down the deepest toilet imaginable.

7. Gaming

Prediction:

- Likely disappoints — no breakout AI-native or Web3 title redefines the space

- Execution challenges and friction continue to dominate

What happened:

- No Breakout Title (Still waiting): The year came and went with no GTA moment. Lists of “top Web3 games” still lean on relics like Axie or trailers for titles that haven’t shipped. Execution remains hard, distribution is fragmented, and user experience is still one wallet pop-up too many.

- Industry Maturity (Stabilising, not surging): The gaming x crypto crossover didn’t regress — it just didn’t evolve either. Studios are maturing, tooling is improving, and infra is being laid down, but the genre-defining title that makes it all click still hasn’t shown up. We’re in the pre-album mixtape phase.

Outcome: Hit ✅

The prediction was for disappointment and the industry delivered. There’s no breakout, no buzz, and no banner year. Just more friction and more waiting.

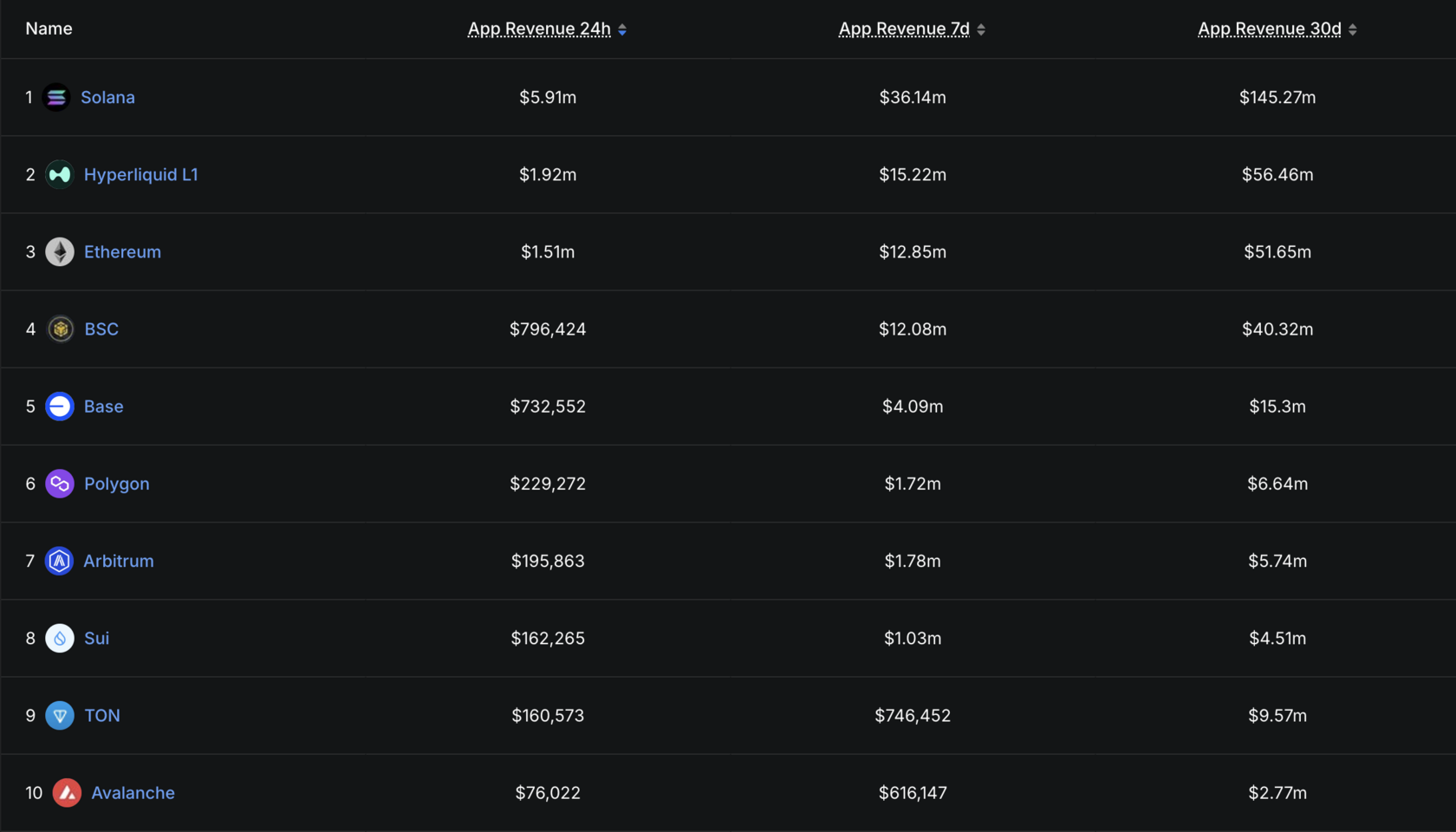

8. L1s and L2s

Prediction:

- Chain count explodes, but traction concentrates in a few dominant general-purpose layers

- App-specific and enterprise chains underwhelm

What happened:

- Power-Law in Action (Solana leads — decisively): App revenue tells the story: Solana is lapping the field with over $145M in 30-day app revenue, more than double its nearest decentralized peer. With the exception of Hyperliquid and BSC, both centralised and/or closed-source, Solana and Ethereum are the only sufficiently decentralised execution environments with real traction.

- The Long Tail (Still long, still trailing): L2s like Base, Arbitrum, and Polygon are posting numbers, but none are close to breaking out. The user and developer gravity remains stubbornly concentrated. Everyone’s building, but only a few are winning.

Outcome: Hit ✅

The chain map keeps expanding, but activity is consolidating around the usual suspects. It’s still a multi-chain world — it just runs on two of them.

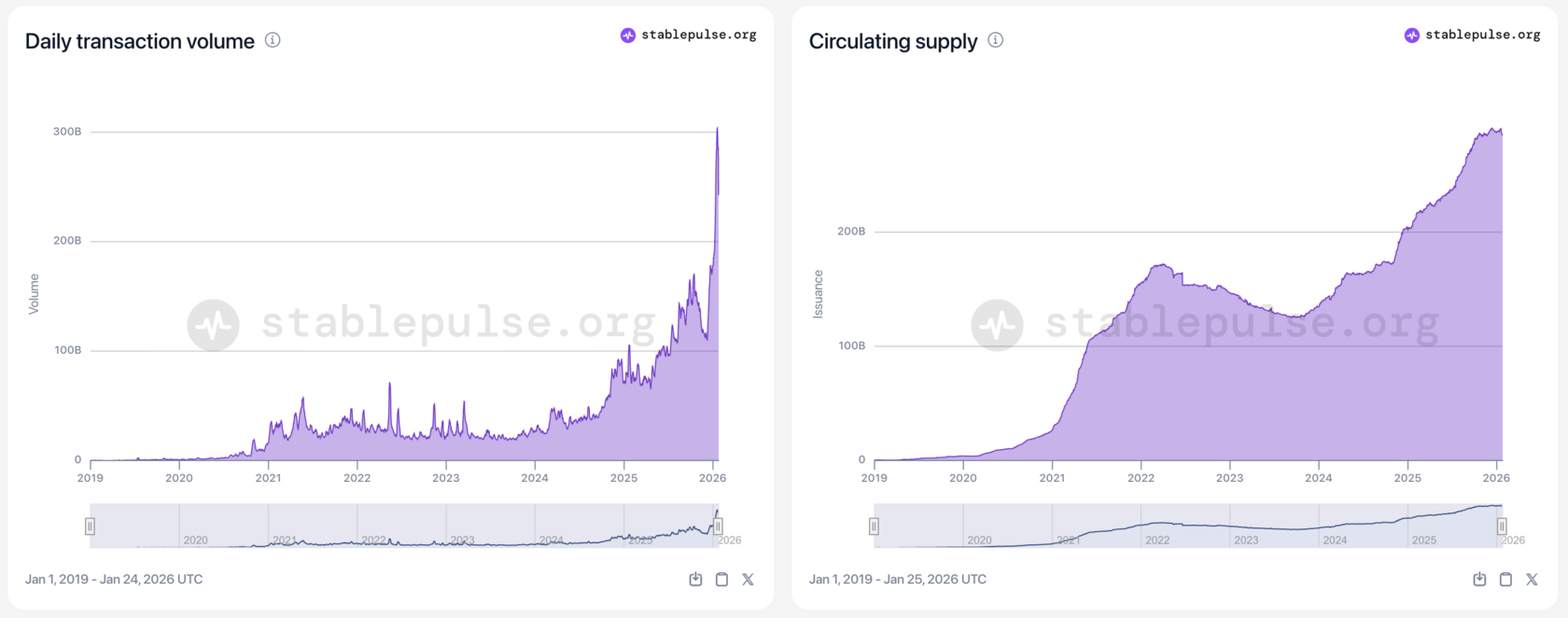

9. Stablecoins

Prediction:

- Combined USDC + USDT market cap exceeds the combined market cap of the two largest volatile assets (e.g., ETH + SOL) by end‑2025

What happened:

- Stablecoin Supply (Strong, but not dominant): USDT and USDC ended 2025 at ~$187B and ~$75B respectively, for a combined ~$262B -- a massive footprint and an all-time high for the sector. It reflects enduring demand for blockspace-backed dollars, even in a sideways market.

- ETH + SOL (Still on top): ETH and SOL held a combined market cap well above $262B — Ethereum alone remained north of $300B at times.

- Narrative vs. Numbers: In practice, stablecoins did cement their role as the default settlement layer and the most used assets in crypto. But the prediction wasn’t about narrative strength — it was a strict market cap comparison. On that front, it didn’t land.

Outcome: Miss (but spiritually accurate) 🙈

Stablecoins are the most used, most demanded, and most defensible assets in crypto, just not the largest by cap. The story was right, the numbers weren’t.

10. SocialFi

Prediction:

- A crypto-native social app (not trading-disguised) cracks $100M in annualized revenue

- Presence, identity, gated access, and native UX on Solana drive a breakout

- At least one app ranks in crypto’s top 15 by revenue — signaling a real consumer moment

What happened:

- No Breakout App (Still waiting): The $100M revenue milestone wasn’t just missed — it wasn’t even approached. Zora briefly flashed activity but never scaled, and most apps that aimed to prioritise identity or presence couldn’t get past the bootstrap phase. Revenue wasn’t generated — it was imagined.

- Solana's Social Layer (Some signals, no explosions): Solana saw real movement on the distribution and engagement front. Seeker emerged as one of the most successful consumer apps in the space with strong retention. Collector Crypt and the Crypto Fantasy League brought niche but sticky engagement models, and overall Solana SocialFi felt more alive than dead, just not yet financially material.

- One Exit, No Entrants: Farcaster, once Ethereum’s flagship hope for decentralized social, was officially sunset - a reminder that good design and thoughtful principles don’t always translate into scale. Its end capped a year in which many tried, few shipped, and none broke through.

Outcome: Miss ❌

The infrastructure showed up. A handful of promising apps did too. But the breakout moment -- $100M in revenue, top-15 ranking, consumer pull -- never arrived. The spirit of the prediction was clear. The reality is still loading.

That helps a lot — with those details, here’s the updated Futarchy section, properly grounded in what actually happened:

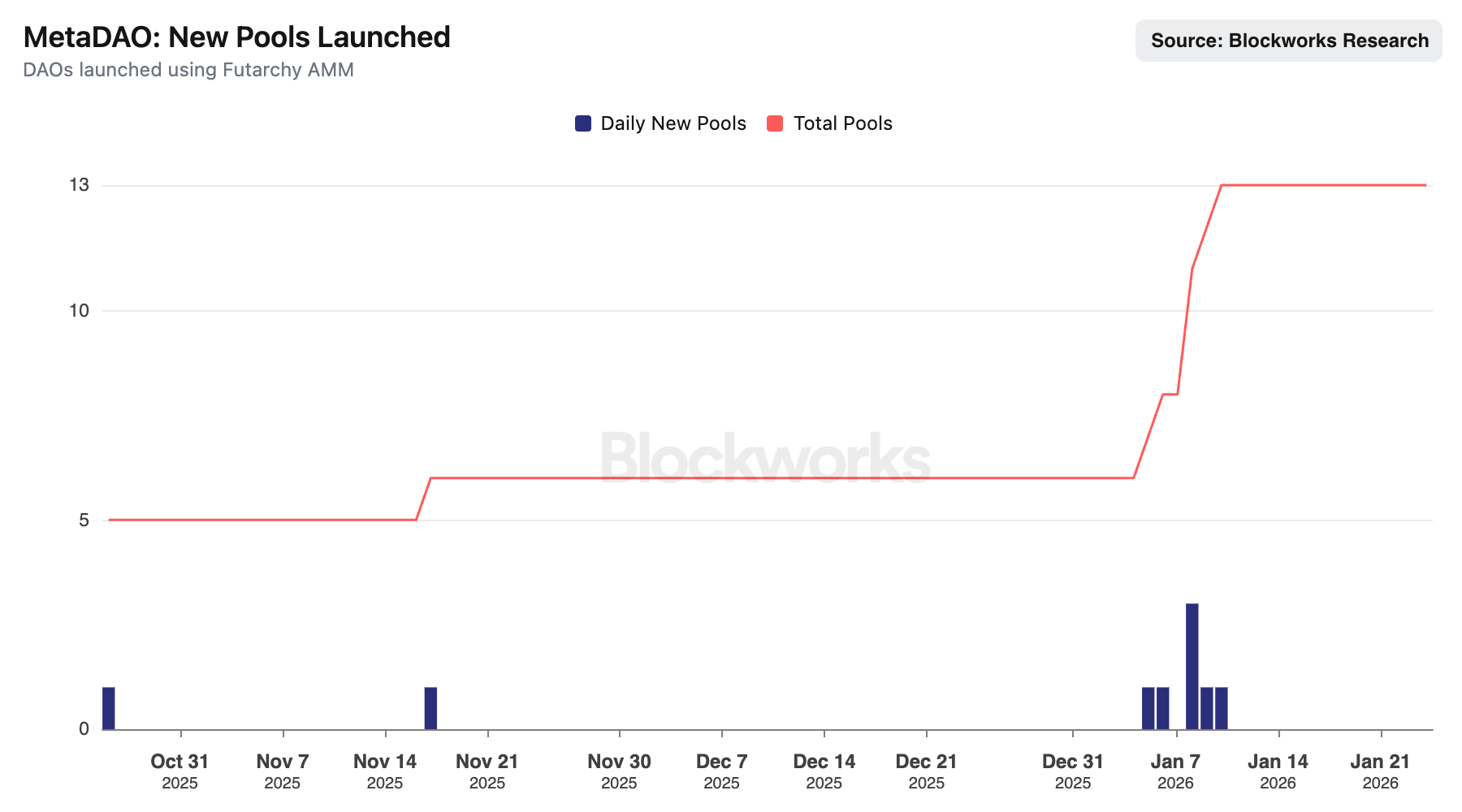

11. Futarchy

Prediction:

- Futarchy shifts from fringe theory to emerging best practice in 2025

- Prediction markets increasingly guide key governance decisions

- The number of projects using futarchy doubles to at least 20

- $META breaks into the top 200 by market cap

- Market-based signaling becomes a serious input in governance

What happened:

- Adoption (Quiet but growing): Futarchy didn’t go mainstream, but it stopped being hypothetical. Over 20 projects including 9 ownership coins are now experimenting with prediction-based governance via MetaDAO - from funding decisions to upgrade signalling. It’s still early, but it’s not fringe anymore.

- $META (Top 200, briefly): $META cracked the top 200 by market cap at least once in 2025 - not a sustained run, but a credible signal that the market is beginning to take futarchy-linked assets seriously. It hasn’t held that level, but it’s been there.

- Governance Culture (Less ironic, more serious): Decision markets are no longer just governance cosplay. DAOs aren’t replacing voting with markets but they are learning how to integrate signals from conditional markets and ownership coin trading into their decision flows. It’s not the default yet, but it’s showing up.

Outcome: Hit (modest, but real) ✅

Futarchy didn’t explode — but it arrived. The project count crossed the threshold, $META touched the top 200, and prediction-based governance moved from theory to tooling. It’s not yet a best practice, but it’s no longer just a thought experiment.

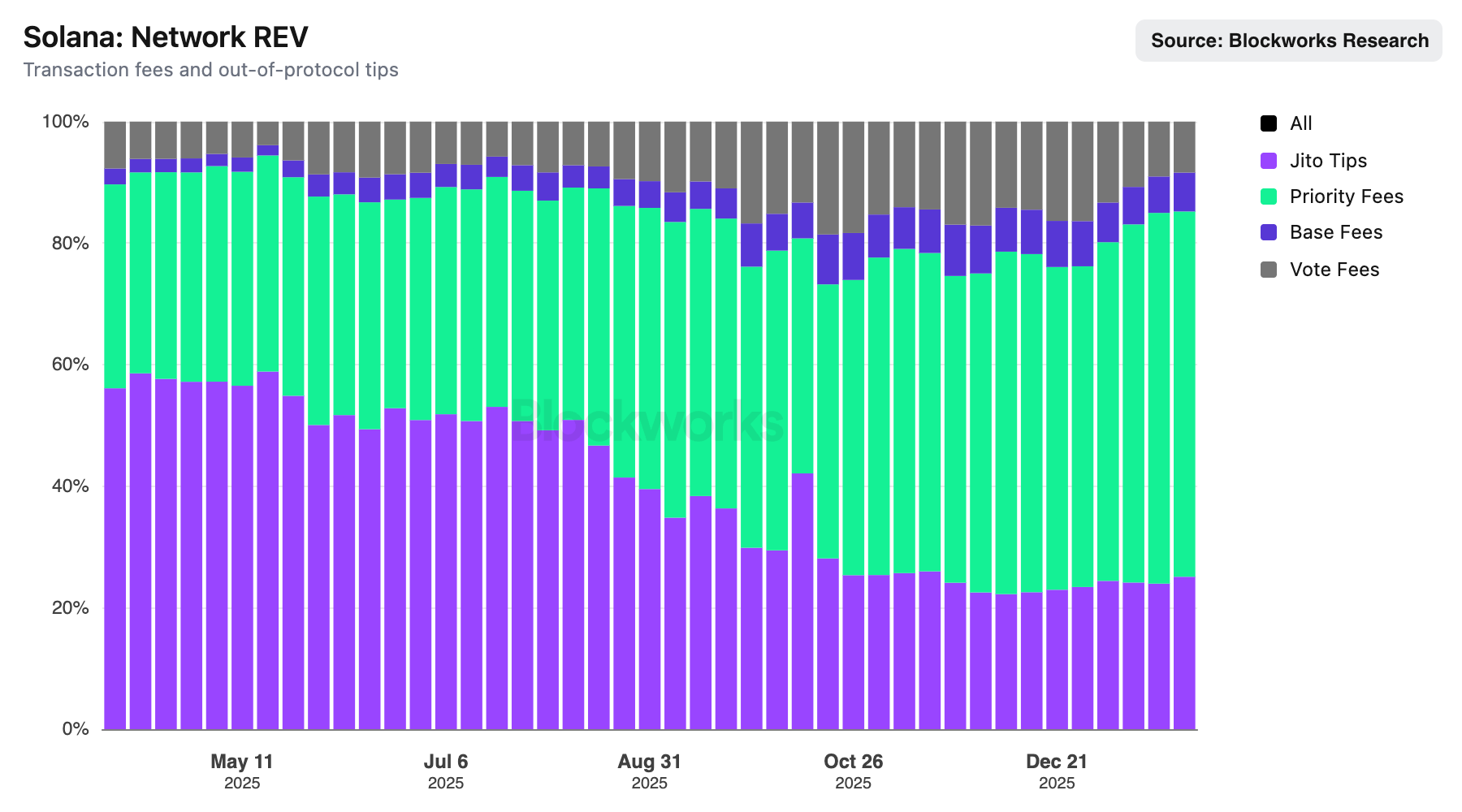

12. MEV

Prediction:

- MEV becomes a visible layer of protocol design, shifting from extraction to alignment

- DFlow gains adoption across major DEXs

- Jito faces pressure but maintains dominance through adaptation

What happened:

- MEV Goes Visible: MEV evolved from backend chaos to protocol design input. Solana, in particular, saw block construction and order flow become competitive markets, not accidents.

- Harmonic Enters, Open Sourcing the Game: Paradigm-backed Harmonic introduced open block building, allowing validators to select among competing builders based on custom policies — revenue, fairness, or app preference. It formalises MEV as a design surface, not a side effect.

- Jito Holds the Line: Jito, long dominant, finally faced pressure — and adapted. BAM is aimed to keep them in the lead, but the presence of credible competitors confirmed the prediction: the moat was tested, and it held.

- DFlow Breaks Through: DFlow went from <1% to over 6% of DEX aggregator volume, surpassing OKX Router and powering every major Solana DEX and purpose-built AMM.

Outcome: Hit ✅

The prediction nailed all major shifts: MEV became architecture, DFlow gained real market share, and Jito faced — and survived — its first real competition. Alignment over extraction isn’t theory anymore — it’s throughput.

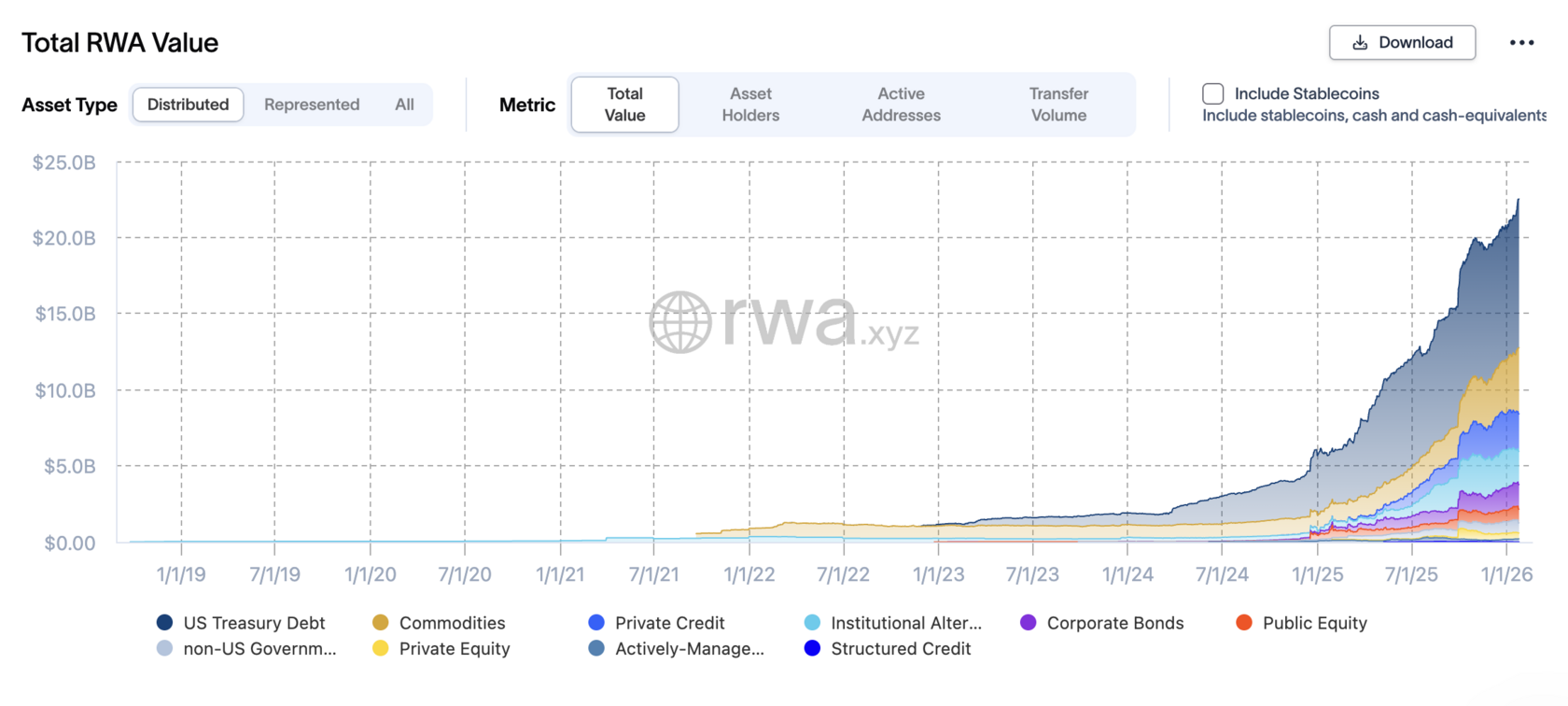

13. Tokenisation

Prediction:

- The total value of tokenised real-world assets (RWAs) will triple by end‑2025

- Tokenised equities emerge, led by Base and Coinbase

- Crypto-native companies explore on-chain IPOs (e.g., Phantom)

- Tokenisation gains traction as global markets inch onchain

What happened:

- RWA Market More Than Tripled: Whether due to real demand or revised accounting, the onchain RWA market grew from ~$5B to well over $20B in 2025 — a clear 3x+ expansion of distributed value. That growth came mostly from tokenised treasuries, credit, and institutional debt products — not the equity side, but it counts.

- Tokenised Equities (Still Early): The idea advanced, but adoption didn’t. There was no Base‑hosted COIN token, and tokenised equities remain a small, thinly traded slice of the RWA stack.

- Onchain IPOs (Still Vapour): Phantom didn’t go public, onchain or otherwise. The notion of crypto-native IPOs remains an aspiration, not a reality.

Outcome: Hit (with caveats) ✅

The prediction called for RWAs to triple — and they did. Tokenised equities and onchain IPOs didn’t arrive, but the core thesis - that more real-world capital would move onchain - clearly played out.

Fair — the prediction was specific: a new U.S.-based centralized exchange. And that didn’t materialize. What we got instead was arguably better, but not what was written.

Here’s the final, honest version with a balanced judgment call:

14. A New US CEX

Prediction:

- A new U.S.-based centralized exchange emerges to challenge Coinbase

- Fast onboarding, retail-first UX, lower fees, crypto-native narrative

- Coinbase faces real competition for the first time in years

- Hyperliquid

What happened:

- No New U.S. CEX — But Solana Became the Exchange: We didn’t get a new U.S.-licensed exchange. But we did get something bigger and better, and more exciting: Solana outpaced every centralised exchange in spot volume in 2025 except for Binance. That’s not just a blockchain. That’s an exchange, a settlement layer, and a distribution channel all in one. The everything exchange.

- Hyperliquid Emerged — Just Not in the US: Hyperliquid delivered on the UX and narrative promise: a performant, onchain perps venue with CEX-like polish. It didn’t check the regulatory box, but it absolutely pulled order flow and attention. We did mention Hyperliquid in the prediction. Were we joking?

- Coinbase Faced Real Pressure — Just Not From Where Expected: The prediction got the pressure right. It just missed the source. Instead of a startup in Miami, it came from blockspace and low-latency CLOBs onchain.

Outcome: Miss (but eclipsed by reality). 🙈

The forecast was for a new U.S. CEX and that didn’t happen. What did happen was bigger: Solana became the second-largest venue in crypto by spot volume. The challenger showed up, it just didn’t file with FinCEN.

Absolutely — here’s the Byron-style wrap-up:

15. JLP $10

Prediction:

- JLP becomes a high-beta dark horse, riding Solana and Jupiter’s breakout

- $10 moves from meme to momentum

What happened:

Absolute disaster. JLP didn’t ride anything except the floor. No comment on this one.

Outcome: ❌

Postlogue

Looking back, the hits were rarely clean, the misses often instructive, and the curveballs — as always — came out of nowhere.

The final score: 7 hits, 6 misses, and 2 monkeys that be interpreted both ways. Not bad for a year that tried its best to destroy the crypto sector forever, as usual.

2025 was acutely described by Michael Ippolito as "the best worst year." If it proved anything, it’s that directional accuracy beats timestamped certainty. And if 2026 plays out the same way, we’ll get a few more wrong — hopefully for all the right reasons.