This article assumes a basic understanding of Pendle’s mechanics, PT/YT markets, and the broader yield-bearing stablecoin landscape. Building on this foundation, the piece focuses on forward-looking cash flow dynamics and protocol-specific inflection points - particularly Pendle’s expansion into interest rate derivatives - and how they reshape the protocol’s long-term economic profile and valuations.

Our goal is not to arrive at a single “fair value”, but to build a framework for thinking about what needs to be true for Pendle to justify an 8-10x valuation move over time.

Our goal is not to arrive at a single “fair value”, but to build a framework for thinking about what needs to be true for Pendle to justify an 8-10x valuation move over time.

Thesis summary

- Pendle is the leading yield-stripping and yield-trading platform in crypto, deeply integrated across DeFi and structurally well positioned to benefit from the continued growth of yield-bearing crypto assets, particularly yield-bearing stablecoins, LSTs/LRTs, money markets deposits, as well as funding rates across perpetual futures markets.

- Pendle has emerged as the premier go-to-market venue for yield-bearing asset issuers to bootstrap TVL and distribute yield exposure. The protocol simultaneously serves traders, asset issuers, and money markets, creating a self-reinforcing liquidity network effect that is difficult to replicate. With the stablecoin market expanding and yield-bearing variants taking a bigger slice, Pendle has claimed an outsized share of yield-related flows and trading.

- At a deeper level, Pendle’s traction reflects a broader structural shift in crypto markets. As the ecosystem matures, yield increasingly stops being an incidental byproduct of incentives and becomes a strategic variable. Rather than being observed after the fact as realized APY, yield is increasingly priced in advance, traded, hedged, and embedded directly into balance-sheet decisions. Once yield becomes a forward-looking, tradable variable, it begins to shape leverage, collateral usage, and capital allocation across DeFi.

- This shift creates demand for infrastructure capable of expressing expectations about rates and coordinating capital around those expectations at scale, within a derivatives market that is potentially orders of magnitude larger than underlying spot yield markets. Boros, Pendle’s interest rate derivatives product, addresses this demand by turning yield into a first-class, tradable financial object and establishing the core primitives required for swap rate markets. Launched in August 2025, Boros has already demonstrated early traction, reaching approximately $237m in open interest by January 2026, and has the potential to become a meaningful contributor to the protocol’s future cash flows.

- Pendle’s strategic advantage lies in rejecting horizontal product sprawl for new users and building a vertical “yield stack” that creates structural lock-in via two complementary engines. Pendle V2 anchors billions in sticky TVL as the inventory layer. Boros captures the high-velocity futures market for funding rates as the volatility layer. This lets Pendle monetize simultaneously as a balance sheet manager, extracting value from yield-bearing inventory, and as a velocity actor, collecting aggressive swap fees and margin interest from traders. Both revenue streams feed into a single vePENDLE/sPENDLE sink, forming a self-reinforcing gravity well. Sticky V2 capital provides essential pricing for Boros. High-frequency fees from Boros subsidize rewards that lock capital in place. This positions Pendle as the permanent two-sided central bank of on-chain interest rates. The products are deliberately complementary and mutually reinforce user ownership and entrenchment.

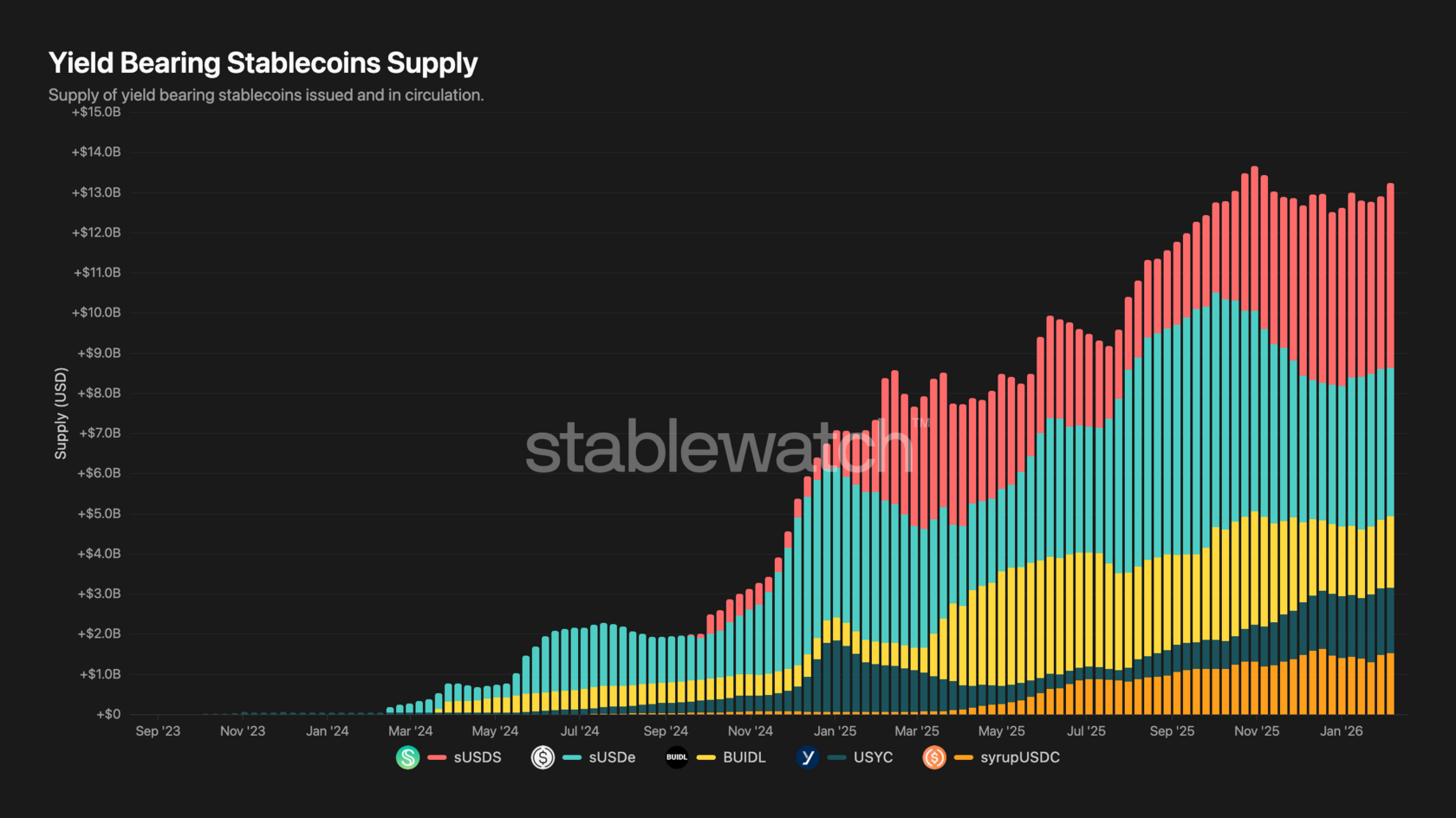

- The stablecoin market remains dominated by non-yielding incumbents carrying inertia from a regulatory era where providing a simple unit of account was a sufficient value prop. These legacy players built massive liquidity and profitability without sharing yields because they didn't have to. Today, the dynamic has shifted: yield-bearing stablecoins have surged from 1% of the market in early 2024 to 7-10% today. As stablecoin issuance proliferates into a red ocean of high customer acquisition costs, new protocols must share yield to survive. Pendle sits at the intersection of these trends, serving as the essential gatekeeper to a yield-hungry user base and the primary infrastructure through which new issuers will distribute returns.

- Pendle is Hodor. The most compelling high-conviction play for Pendle is the defensive entrenchment of its existing incumbency. As yield-bearing stablecoins climb beyond 10% market share, Pendle’s primary objective is to maintain its status as the definitive gatekeeper for rate discovery and yield distribution. Success in this scenario is not defined by chasing new niches, but by "holding the door" — preserving its position as the critical infrastructure through which all new issuers must pass to access liquidity. By successfully defending this territory, Pendle evolves from a speculative tool into a systemic utility, acting as an immovable toll booth that captures the compounding flows of a stablecoin market trending toward $500B.

- Finally, Pendle’s valuation has declined materially following the market peak. The token currently trades at approximately $430m in fully diluted valuation (team fully vested), representing a 4x contraction from Aug-Sep 2025 levels, when the protocol reached peak TVL of approximately $13bn, comparing to 3.2bn now (30 Jan 2025). As the yield-bearing stablecoin market continues to expand and the protocol progresses along its roadmap, we expect Pendle’s fundamentals to strengthen over time, supporting 8-10x valuation growth ($4.0bn FDV under a base case scenario), even under conservative assumptions.

Valuation Overview

- We publish this report following the release of several analytical studies on Pendle (Pendle: Yield King and DeFi's Trifecta: Ethena, Pendle, & Aave by Blockworks and Pendle: The Era of Stablecoin Expansion by Spartan Group and Modular Capital). Each of these pieces applies its own methodology and planning horizon, resulting in different perspectives on Pendle’s valuation, particularly with respect to Boros and its potential contribution to protocol revenues.

- In this report, we present an independent valuation framework with a different analytical focus. Rather than emphasizing short-term trends, we base our analysis on Pendle’s long-term cash flow outlook, using 2030 as the primary forecast horizon. We anchor the model in 2025, relying on observed data for TVL, trading volumes, yield levels, and protocol monetization to reconstruct current market shares and unit economics. The 2030 endpoint captures our vision for the cumulative impact of stablecoin growth, yield-bearing asset adoption, and the development of onchain interest rate markets.

- While our model includes projections for 2026, we do not explicitly reference that year throughout the report. The purpose of the 2026 forecast is to act as a consistency check, ensuring that growth trajectories between 2025 and 2030 are gradual and internally coherent, rather than driven by unrealistic step changes. In other words, 2026 is used to validate the path of the model, not to introduce an additional valuation reference point.

- To reflect uncertainty around the terminal outcome, we apply a scenario-based framework to the 2030 results. Bear, Base, and Bull cases are constructed by applying valuation multiples of 15x, 20x, and 25x to forecasted revenue. These scenarios are not intended to represent precise price targets, but rather to illustrate the sensitivity of Pendle’s valuation to assumptions around market maturity, competitive dynamics, and monetization.

- In addition, our valuation framework reflects Pendle’s updated tokenomics. Under the recently updated design, 80% of protocol revenues are used for Pendle buybacks and distributed to active sPendle holders. Accordingly, our terminal valuation is based on 80% of forecasted 2030 revenues, reflecting the share of economic value directly captured by sPendle holders.

- Our revenue forecasts for Pendle are built around two core products - Pendle V2 and Boros:

- Pendle V2 generates revenue through a combination of yield-based fees and trading activity across its PT/YT markets. The protocol earns a fixed take rate on the yield generated by assets deployed on the platform. In addition, Pendle V2 captures trading fees from PT/YT markets, with volumes typically peaking around expiries, changes in rates or incentive programs.

- Boros represents a distinct revenue stream. As an interest rate derivatives venue, Boros generates fees from both trading activity and open interest. Unlike Pendle V2, Boros is not constrained by the supply or growth of specific yield-bearing assets. It can reference any rate that can be reliably measured via oracles — including funding rates, lending rates, and staking yields. This decouples Pendle’s long-term revenue potential from individual issuers or asset classes and shifts the protocol’s exposure toward system-wide interest rate dynamics across DeFi.

- We believe the timing of this valuation is particularly relevant. Early traction from Boros suggests that Pendle has moved beyond the purely experimental stage and is beginning to demonstrate tangible market validation for onchain rate trading. As a result, Pendle is evolving from a yield optimization protocol into a rate infrastructure layer within Internet-native capital markets, with emerging revenues, identifiable growth drivers, and a scalable economic structure — albeit with appropriate caution given the early stage of Boros and the broader maturity of crypto rate markets.

- Looking ahead, our base-case framework assumes that Boros accounts for an increasing share of Pendle’s revenues over time. While yield-based fees and spot trading activity remain important in the near to medium term, interest rate derivatives offer materially higher scalability if adoption continues. By the end of the decade, we expect Boros to drive approximately 50% of Pendle’s total revenues, reflecting a broader transition in crypto markets from passive yield extraction toward active management of interest rate risk.

- If you would like to explore our assumptions in more detail, we have attached our calculation model here. We have intentionally left all calculations visible, so the readers can easily follow our model and understand the logic and data behind our projections.

Pendle V2 and the Stablecoin Market Overview

- We assume Pendle V2 is structurally exposed to stablecoin growth through its deep integration with yield-bearing stablecoins (YBS), mediated by PT–YT markets, points incentives, and TVL bootstrapping dynamics.

- Stablecoins have quietly become one of the largest and most structurally important asset classes in crypto. By late 2025, total outstanding stablecoin supply reached roughly $300bn — a level that, until recently, would have seemed implausible outside of peak bull-market conditions. Unlike prior cycles, this growth was not primarily driven by speculative leverage. Instead, stablecoins increasingly function as settlement infrastructure, treasury assets, and liquidity rails embedded across both onchain and offchain financial systems.

- As the market has matured, stablecoins have begun to fragment along functional lines. On one side sit transactional stablecoins — USDT- and USDC-like instruments optimized for liquidity, settlement speed, and minimal volatility. On the other side is a rapidly emerging category: yield-bearing stablecoins, designed to capture “cash at rest.”

- We expect total stablecoin supply to expand toward $1.9–2.0t by 2030, broadly in line with the forecasts from the large institutions such as Citi, McKinsey and JPMorgan. Within that growth, the composition of supply changes meaningfully. We assume yield-bearing stablecoins grow to ~15% by 2026, and further to ~30% by 2030, implying a yield-bearing stablecoin market of approximately $570bn by the end of the decade.

- This transition is central to our broader Pendle investment thesis. Yield-bearing stablecoins are not merely another asset category. As stablecoins increasingly resemble interest-bearing cash rather than inert settlement tokens, the demand for instruments that price, trade, and hedge yield becomes structural rather than optional.

Pendle V2: Revenue Forecast

- Pendle V2 economics are driven by two primary revenue streams: yield-based fees on assets deployed to the protocol and trading fees generated by activity across PT/YT markets. Both streams scale with different dimensions of adoption and market dynamics, giving Pendle V2 a revenue profile that is leveraged to yield levels, rate volatility, and trading intensity rather than static TVL alone.

Yield-based fees

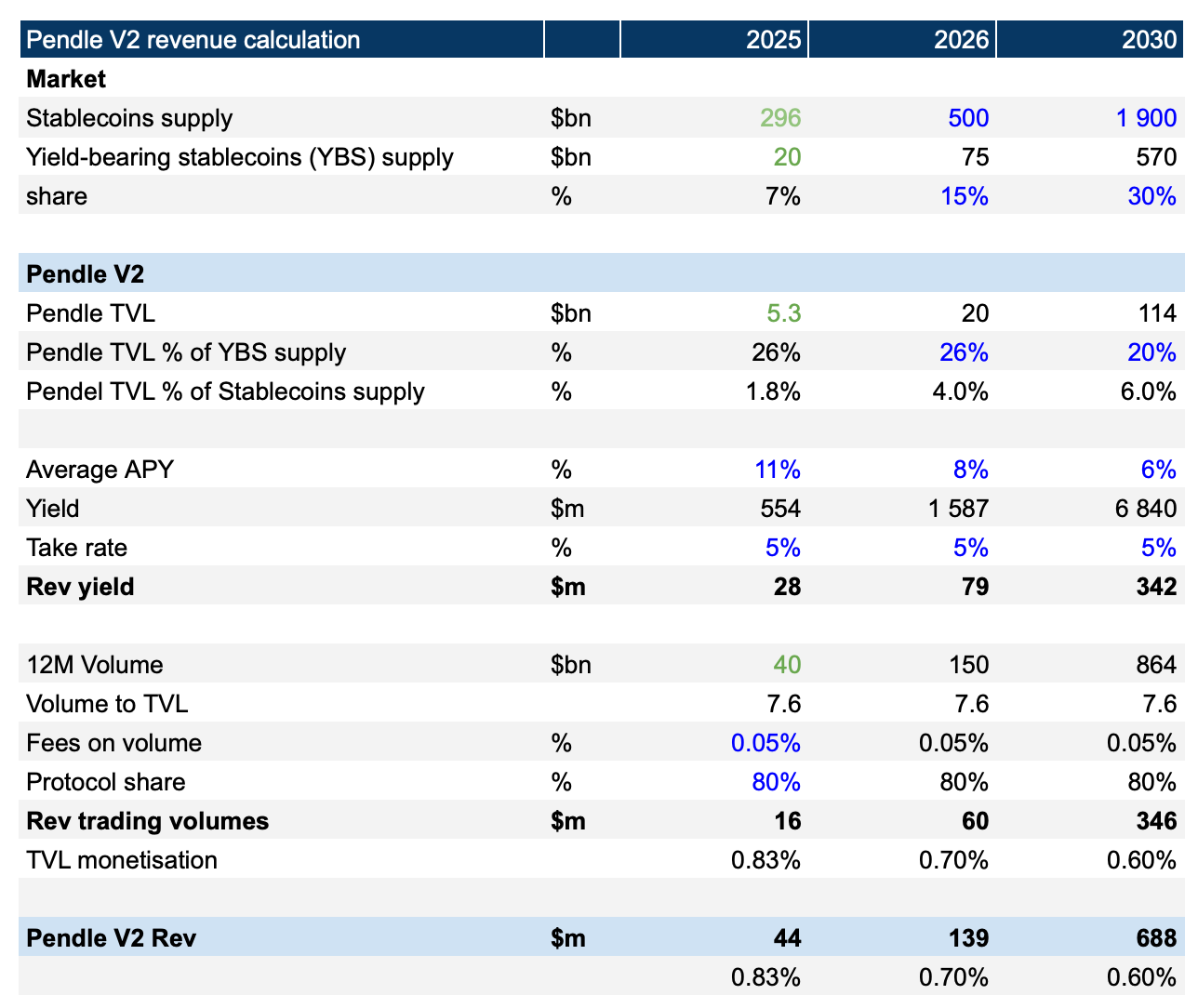

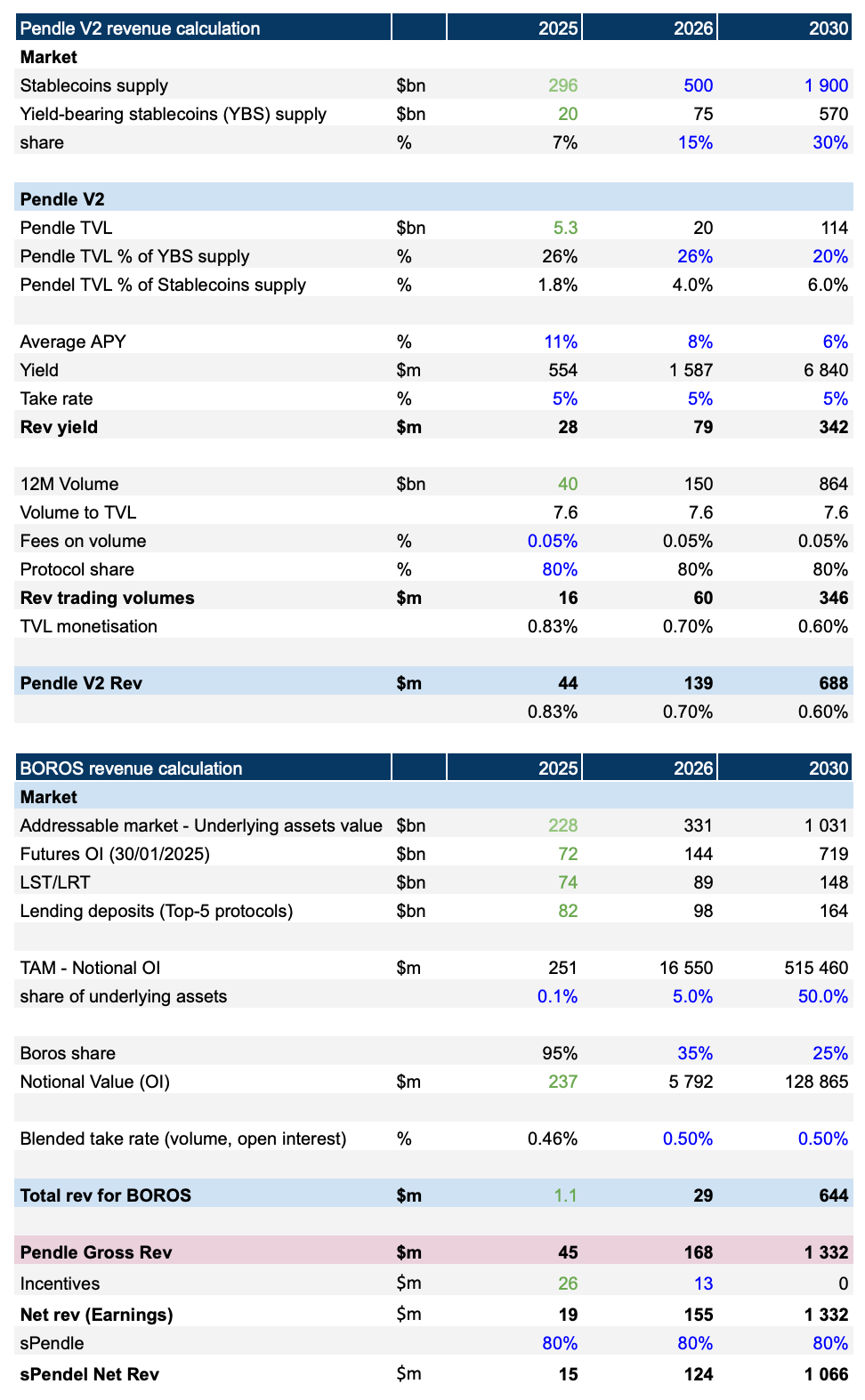

- On the yield side, Pendle captures a fixed 5% take rate on the yield generated by assets deposited on the platform. As a result, revenue is a function of three variables: total active TVL, the average yield of underlying assets, and the protocol’s take rate.

- In 2025 Pendle captures a significant share of this segment, with $5.3bn in TVL (average TVL for last 12 months), representing 26% of the yield-bearing stablecoin market and 1.8% of total stablecoin supply. With an average yield of ~11%, the assets deployed on Pendle generate approximately $554m in annual yield, translating into $28m of protocol revenue from yield.

- Looking forward, we assume continued growth in both stablecoin supply and the penetration of yield-bearing formats. By 2030, yield-bearing stablecoins reach $570bn (30% of supply), while Pendle TVL grows to $114bn, implying a 20% market share within yield-bearing stablecoins. Despite assumed yield compression from 11% in 2025 to 6% by 2030, the expansion in TVL drives yield-based revenues to approximately $79m in 2026 and $342m by 2030.

Trading fees

- In parallel, Pendle V2 generates revenue from trading activity across PT/YT markets. Trading volumes on Pendle are structurally episodic, clustering around expiries, rollovers, and shifts in yield or incentive regimes. This results in high turnover relative to TVL. With historical annual trading volume of $40bn, this implies a volume-to-TVL multiple of ~7.6x.

- Applying this multiple, we estimate $864bn annual trading volume in 2030. Pendle charges a 5 bps fee on trading volume, of which 80% accrues to the protocol, with the remainder distributed to liquidity providers. Under these assumptions, trading activity generates approximately $16m in revenue in 2025 and $346m by 2030.

- Combining yield-based fees and trading fees, Pendle V2 generates approximately $44m in revenue in 2025, scaling to $688m by 2030. Over this period, TVL monetization declines from ~0.83% to ~0.6%, reflecting conservative assumptions around yield compression and competitive dynamics, even as absolute revenues grow materially.

- Taken together, these dynamics position Pendle V2 among the more meaningfully monetized infrastructure protocols in DeFi today. At the same time, they highlight an important limitation: Pendle V2 revenues remain tied to asset-specific TVL, yield levels, and trading intensity. This distinction becomes critical when projecting the protocol’s longer-term economics.

Interest rate swaps market overview

- Crypto today is finally breaking out of the spot-only era we saw in prior cycles. For the first time, we are rapidly developing deep, sophisticated price markets - perpetual futures, options, and beyond - while onchain lending protocols are evolving at an accelerating pace and starting to show real complexity. What we are still lacking is a native, scalable interest rate market. Rates exist everywhere, and yet nowhere at the same time. Funding rates on perpetual futures, borrow rates on money markets, and yields on stablecoins and staking products all shape capital allocation. However, in most cases, these rates are not meaningfully tradable, hedgable, or transferable.

- Market participants largely observe rates after the fact. They cannot easily lock them in, express views on their future path, or manage duration and convexity in a systematic way. In traditional finance, interest rate markets are not a niche - they are the largest derivatives market by notional volume. Interest rates sit upstream of leverage, valuation, and capital allocation decisions across the entire financial system. The absence of an equivalent layer in crypto reflects missing infrastructure, not a lack of economic demand.

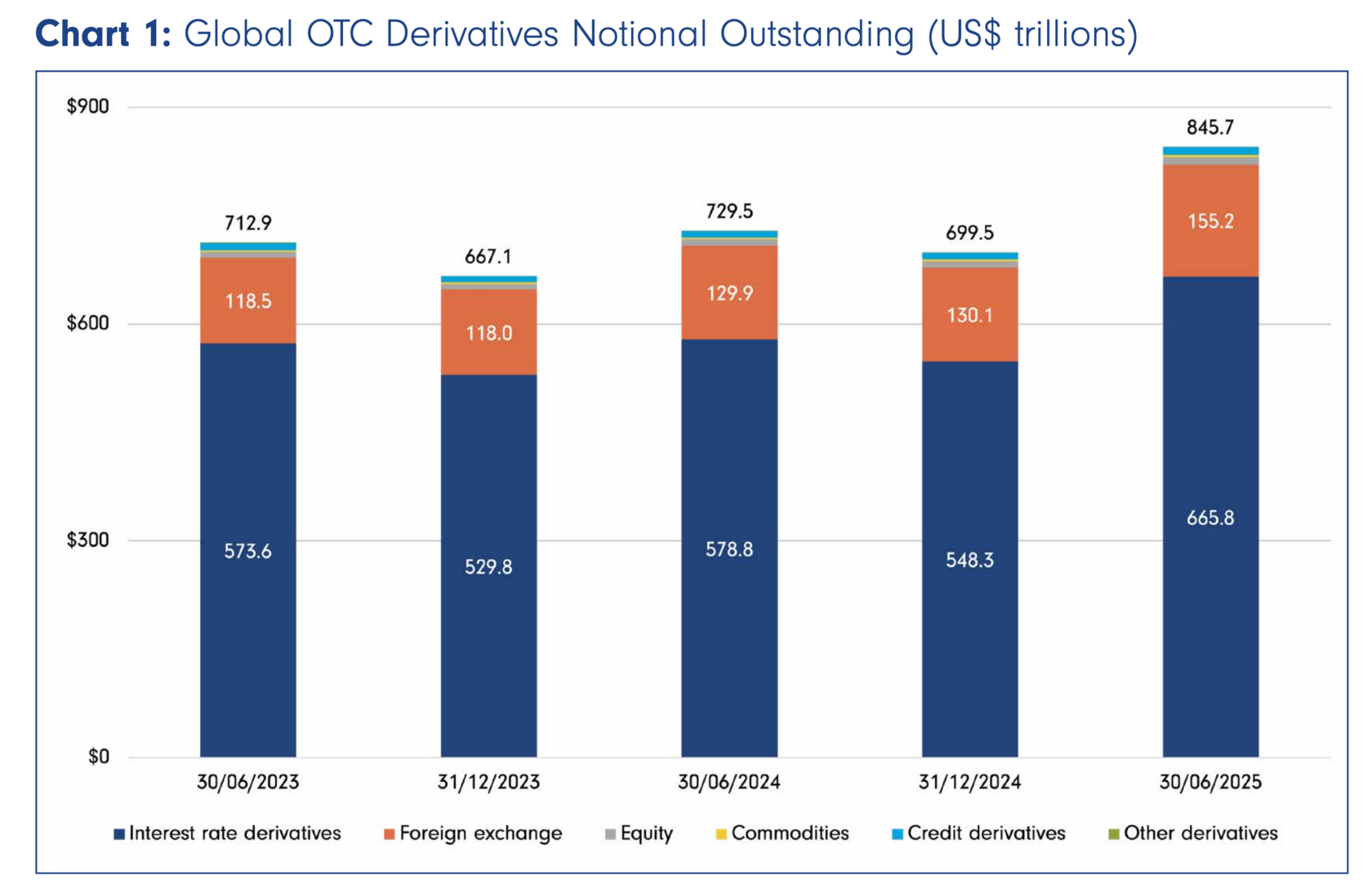

- Traditional interest rate swap markets provide a useful benchmark for the potential scale of this opportunity. Globally, interest rate derivatives settle around $665.8t in notional outstanding at the end of June 2025, up 15% year-on-year from $578.8t in June 2024.

- Importantly, these markets operate at multiples of the underlying asset base. For example, while the global bond market is approximately $130t in size, a substantial share of the $665.8t in global interest rate derivatives outstanding is economically linked to bond yields, implying an estimated 3–4x multiple relative to the underlying asset base. Historically, around 3–4% of this notional open interest turns over as daily trading volume.

- Pendle is the first protocol that meaningfully addresses this gap in crypto. Through its evolution from Pendle V2 into Boros, the protocol is positioning itself as foundational infrastructure for crypto-native interest rate markets — enabling yield, duration, and rate risk to become first-class, tradable objects onchain.

Boros Forecast

- Unlike PT/YT markets, which are constrained by the supply and maturity structure of specific yield-bearing assets, Boros references interest rates directly, enabling it to scale across multiple sources of rate risk. As a result, its addressable market extends well beyond yield-bearing stablecoins to include perpetual futures funding rates, staking and restaking yields (LSTs/LRTs), and rates embedded in large onchain lending markets.

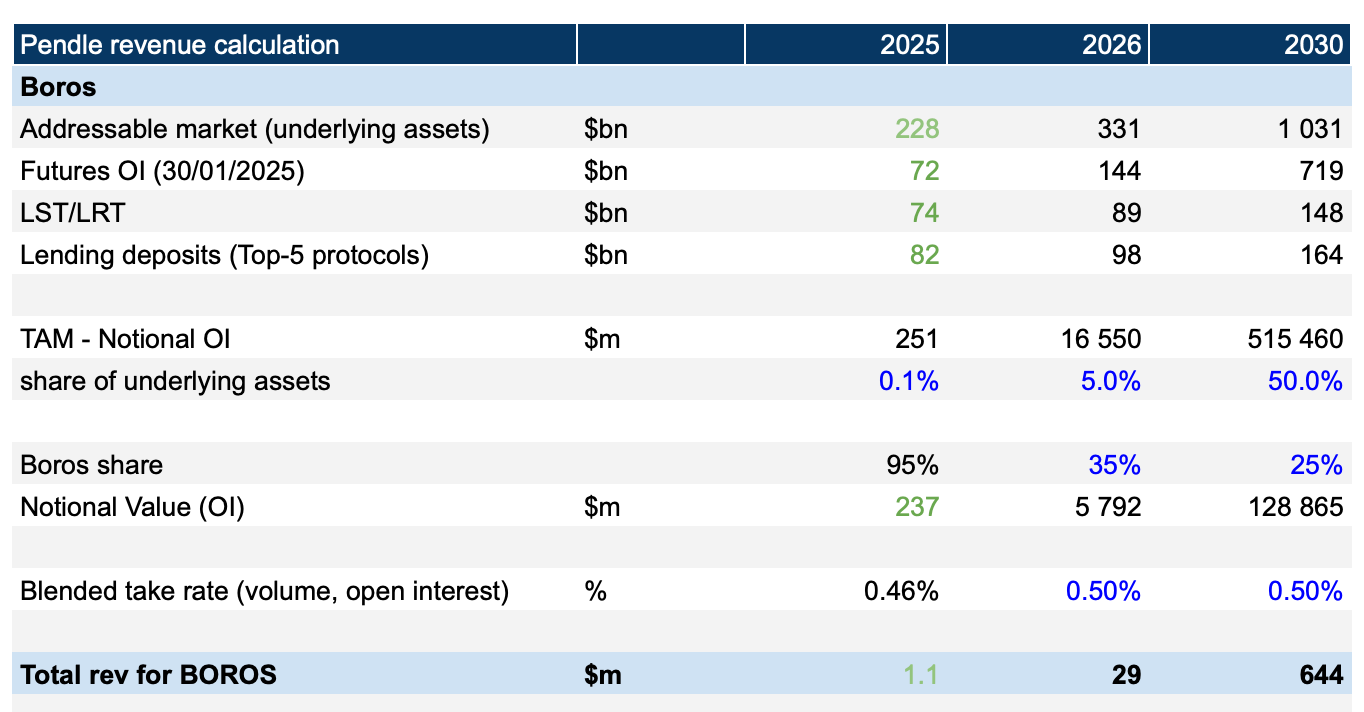

- We estimate Boros’ addressable market by aggregating pools of capital where interest rate risk already exists but remains largely unmanaged. As of year-end 2025, this base totals approximately $228bn in underlying assets, composed of $72bn in perpetual futures open interest, $74bn in LST/LRT market capitalization, and $82bn in deposits across the top-5 onchain lending protocols. Under our growth assumptions, this underlying base expands to $331bn in 2026 and exceeds $1.0t in 2030, reflecting the continued growth of leverage, staking, and onchain credit markets. We assume a 5x expansion in perpetual futures open interest and a 2x expansion in both LST/LRT market capitalization and lending deposits over this 5-year period.

- Boros does not need to intermediate the full notional of these markets to become economically meaningful. We model interest rate derivatives open interest as a share of underlying assets, growing from just 0.1% in 2025 to 50% by 2030. While ambitious in absolute terms, these penetration levels remain below traditional finance analogues, where interest rate derivatives routinely exceed the size of underlying asset bases. Under these assumptions, total notional open interest across onchain rate markets grows from approximately $0.25bn in 2025 to $17bn in 2026 and $515bn by 2030.

- Within this expanding market, we assume Boros’ share declines over time as competition increases — from approximately 95% in the early launch phase to 25% by 2030. Under these assumptions, Boros-specific open interest grows from approximately $237m in the initial months following launch in 2025 to $129bn by 2030.

- Boros monetizes activity through two complementary channels. First, it charges a 0.05% fee on trading volume generated by rate swap activity, which can be substantial relative to posted collateral given the margined nature of the product. Second, it collects a settlement fee on open interest, charging a flat 0.1% fee on the fixed-rate leg of each position at settlement. In addition, Boros applies a small fixed operational fee on the first transaction and then intermittently (approximately every ~50 transactions) thereafter.

- Together, these mechanisms align protocol revenues with both trading intensity and the duration and size of outstanding positions. Based on observed early traction — approximately $1.1m in fees generated on $237m of open interest during the initial launch period — this implies a blended effective take rate of 0.46%. To reflect uncertainty at this stage, we applied a blended take rate of 0.5% on open interest in our forward projections. Under these assumptions, Boros generates $29m in annual revenue in 2026 and approximately $644m in 2030.

- Accordingly, in our financial model, Boros revenues remain modest in the near term, reflecting the early stage of the product. Over the medium term, however, we expect meaningful growth as onchain interest rate derivatives markets develop and begin to converge toward the structural relationship observed in traditional finance between derivatives markets and their underlying asset bases.

- As this transition unfolds, Boros accounts for an increasing share of total protocol revenues and, under our base-case assumptions, is expected to contribute ~50% of Pendle’s total revenues by the end of the decade.

- Critically, this revenue upside is structurally decoupled from any single issuer or asset class. Boros’ growth depends not on the success of a particular stablecoin or yield strategy, but on the maturation of crypto markets themselves. As capital bases expand and rate volatility persists, the lack of native tools to hedge and express interest rate exposure becomes increasingly untenable — creating a durable foundation for Boros’ long-term growth.

Valuation Summary

In summary, our key valuation assumptions for Pendle are as follows:

- We assume total stablecoin supply grows from approximately $300bn in 2025 to $1.9–2.0t by 2030, broadly in line with forecasts from institutions such as Citi, McKinsey and JPMorgan.

- Yield-bearing stablecoins currently represent roughly 7% of total stablecoin supply (~$20bn). We assume their share increases to 30% by 2030, implying a yield-bearing stablecoin market of approximately $570bn by the end of the decade. This assumption remains conservative relative to some institutional expectations that see yield-bearing stablecoins reaching up to 50% of supply over the long term.

- Pendle V2’s TVL is modeled as capturing 20% of the yield-bearing stablecoin market by 2030, down from 26% on a trailing basis today, reflecting increased competition and market maturity. This implies $114bn of Pendle V2 TVL in 2030, corresponding to roughly 6% of total stablecoin supply.

- Pendle V2 captures a 5% take rate on yield generated by assets on its platform. While average yields across Pendle markets were approximately 11% in 2025, we assume yield compression over time and model a decline to 6% by 2030. Applied to forecasted TVL, this results in approximately $342m of yield-based revenue for Pendle V2 in 2030.

- Pendle V2 trading volumes are modeled as a function of TVL, based on a historical volume-to-TVL multiple of 7.6x. Applying this multiple to forecasted 2030 TVL implies approximately $864bn in annual trading volume. At an average fee of 5 bps, with 80% accruing to the protocol (20% to LPs), this generates approximately $342m of trading-related fees in 2030.

- Combining yield-based fees and trading fees, we project $688m of Pendle V2 revenue in 2030, up from approximately $44m in 2025. Notably, our model assumes a decline in revenue-to-TVL from ~0.83% in 2025 to ~0.6% by 2030, reflecting conservative assumptions around yield compression and competitive dynamics.

- For Boros, we estimate an addressable market of $228bn in underlying rate-bearing assets in 2025, including $72bn in perpetual futures open interest, $74bn in LST/LRT market capitalisation, and $82bn in deposits across the top-5 onchain lending protocols. Applying different growth assumptions, we project this base expands to approximately $1.0t by 2030.

- We assume interest rate derivative open interest (OI) grows from ~0.1% of underlying assets in 2025 to 50% by 2030, still well below traditional finance analogues. This implies a total onchain interest rate derivatives market of approximately $515bn in open interest by 2030.

- While Boros currently represents the vast majority of onchain rate swap activity, we assume increased competition over time and model Boros capturing 25% of total onchain interest rate derivatives open interest by 2030, or approximately $129bn. Applying a 0.5% blended fee take rate, we estimate $644m of Boros revenue in 2030.

- Combining Pendle V2 and Boros, we forecast $1.3bn in total Pendle protocol revenue by 2030. We do not explicitly deduct incentives (points) in the terminal year, assuming a more mature and less subsidy-dependent protocol environment.

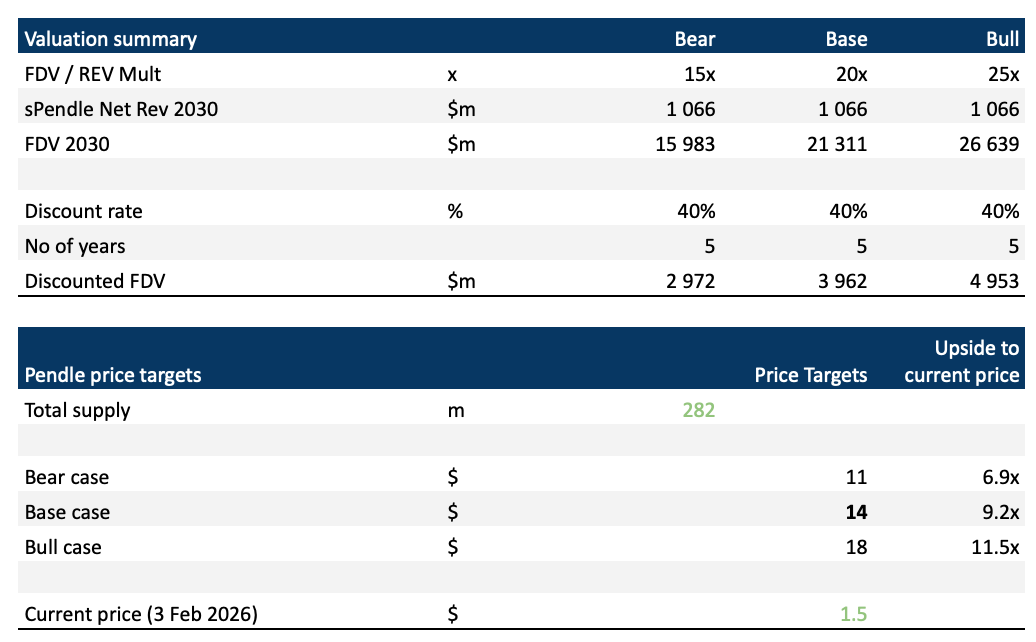

- Under the current tokenomics, approximately 80% of protocol revenues accrue to staked sPendle holders, implying $1bn of cash flows attributable to sPendle holders in 2030.

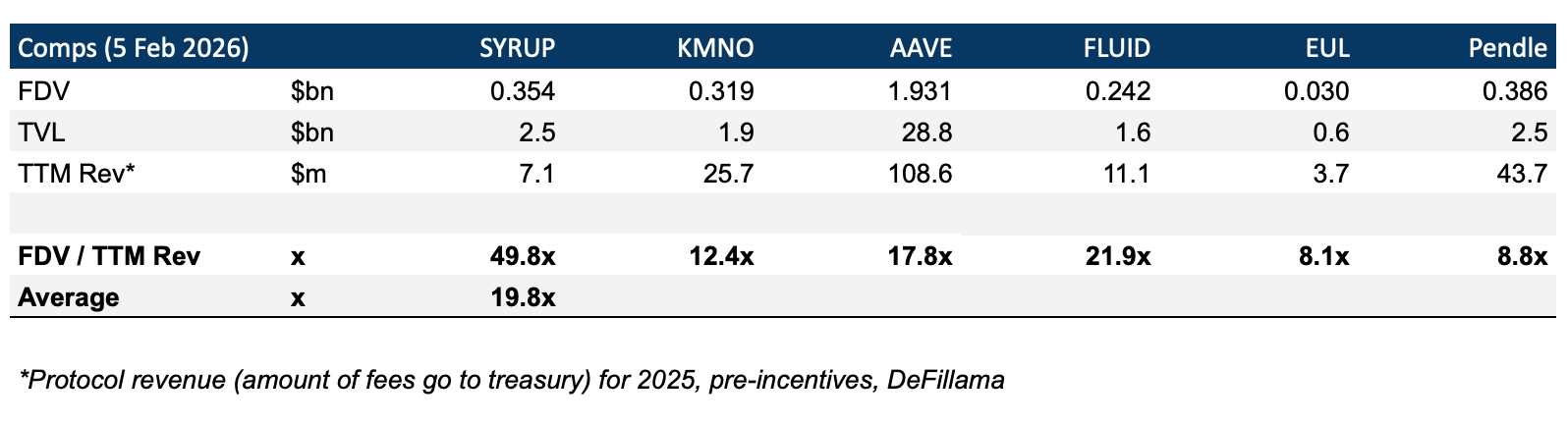

- For valuation purposes, we apply a 20x FDV/Revenue multiple in our base case, broadly consistent with comparable DeFi protocols. In the bear and bull scenarios, we adjust the revenue multiple to 15x and 25x, respectively, while keeping other assumptions constant.

- We then discount these values from 2030 to early 2026, applying a 40% annual discount rate to reflect execution, competitive, and regulatory risks. The discount factor is (1 + 0.4)^5 = 5.38

- Across all three valuation scenarios, Pendle appears undervalued:

- Bear case (15x multiple) → implied discounted FDV of $3.0bn, corresponding to a $11 Pendle price target (6.9x upside).

- Base case (20x multiple) → implied discounted FDV of $4.0bn, or a $14 Pendle price target (9.2x upside).

- Bull case (25x multiple) → implied discounted FDV of $5.0bn, or a $18 Pendle price target (11.5x upside).

Sensitivity Analysis

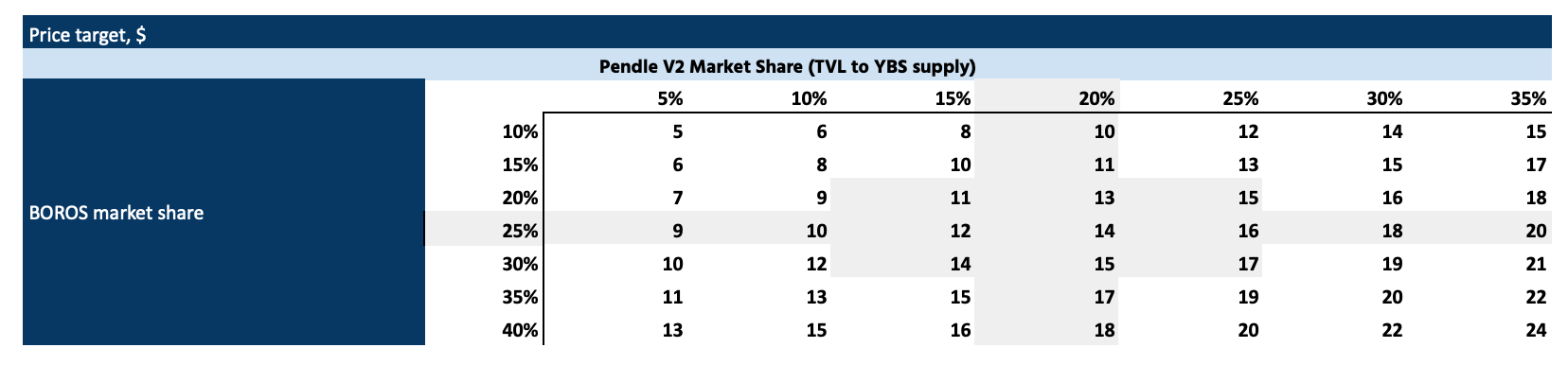

- We stress-tested our valuation model by varying two key inputs — Pendle V2 market share in 2030 (TVL to YBS supply) and Boros market share — to evaluate the sensitivity of Pendle’s token price under different growth scenarios.

- Under more downside-oriented assumptions — with Pendle V2 capturing 5% of the yield-bearing stablecoin market and Boros capturing 10% of onchain interest rate derivatives market— the model implies a Pendle token price of approximately $5 or around 3x relative to the current price.

- For readers interested in exploring the assumptions in more detail, we have attached our full calculation model here. All calculations are intentionally left fully transparent to allow readers to follow the logic and underlying data behind our projections.

Upside potential

While our valuation already implies meaningful upside relative to current market pricing, we believe that several assumptions could evolve more favourably over time. These factors represent sources of upside that could materially enhance Pendle’s long-term economics.

Upward revisions to stablecoin supply forecasts:

- Our projections anchor on a total stablecoin supply of approximately $1.9t by 2030, consistent with the base case outlined in Citi’s latest stablecoin outlook. We intentionally adopt this estimate as a restrained reference point. Notably, Citi recently revised its forecasts upward, citing strong recent market growth and a growing pipeline of announced projects, with its bull case now implying stablecoin supply of up to $4.0t over the same horizon. The gap between the base and bull scenarios highlights uncertainty around long-term adoption, with upside skewed toward larger outcomes.

- If stablecoins continue to establish themselves as a core layer of financial infrastructure, aggregate supply could exceed our base-case assumptions by a wide margin. Given Pendle V2’s role in yield discovery and TVL formation for yield-bearing assets, higher stablecoin penetration would directly translate into a larger addressable market without requiring changes to Pendle’s competitive positioning.

Faster adoption of yield-bearing stablecoins:

- In our model, we assume yield-bearing stablecoins grow from roughly 7% of total stablecoin supply today to 30% by 2030. This assumption is conservative relative to some institutional research, which suggests yield-bearing formats could ultimately represent up to 50% of stablecoin supply as tokenized MMFs, yield-generating deposits, and onchain cash equivalents become more prevalent.

- This shift is already being actively supported by new issuance and distribution models, for example Ethena whitelabel stablecoin-as-a service platform, which enables chains and applications to issue yield-bearing stablecoins backed by USDe and USDtb. Early traction following its announcement, including adoption by issuers such as MegaETH, Jupiter, and Sui, illustrates the potential for such programs to catalyze renewed growth in the Pendle ecosystem.

- If this transition accelerates, the impact on Pendle would be multiplicative rather than linear. Yield-bearing stablecoins increase the demand for fixed-rate exposure, yield hedging and duration management — all of which directly expand Pendle V2’s economic potential.

Higher sustained TVL share and monetization efficiency on Pendle V2:

- Our base case assumes a gradual decline in Pendle’s TVL share of the yield-bearing stablecoin supply over time to 20% (TVL relative to YBS supply), reflecting increased competition and market maturation. However, Pendle’s current positioning — as the dominant yield-stripping venue with deep integrations across money markets, vaults, and incentive programs — suggests it may be able to defend a higher steady-state share than modeled. At present, Pendle maintains a substantial lead in both TLV and liquidity depth relative to competing protocols.

- In addition, our assumptions around TVL monetization remain deliberately conservative. We model a gradual decline in revenue-to-TVL toward approximately 0.6% over time. By contrast, Blockworks suggests that Pendle’s proximity to end users and its central role in yield distribution could support higher monetization, potentially approaching 1%, particularly as incentive-driven activity gives way to more structural yield and interest rate management.

Expansion into additional rate markets and derivatives market penetration:

- Boros benefits from a structurally expanding addressable universe of rate-driven markets. Unlike Pendle V2, which is tied to the issuance and maturity structure of specific yield-bearing assets, Boros can reference any rate that can be reliably observed via oracle feeds. This includes, but is not limited to, perpetual futures funding rates, PoS staking and restaking yields, and borrow rates across large onchain money markets.

- As DeFi matures, new categories of rate-sensitive capital are likely to emerge — including tokenized deposits, structured yield products, and hybrid CeFi–DeFi instruments. In addition, the tokenization of equities and other real-world assets could materially expand the universe of onchain perpetual futures and associated funding rates, significantly increasing the size and diversity of rate markets that Boros can reference.

- Beyond growth in underlying assets, our model also assumes a gradual increase in the penetration of crypto-native interest rate derivatives. We forecast onchain rate derivatives open interest reaching approximately 50% of underlying assets by 2030, a level that remains conservative relative to traditional finance, where interest rate derivatives commonly exceed underlying cash markets by 3–4x. This structural gap highlights how early crypto rate markets remain and suggests meaningful upside from increased derivatives penetration alone, independent of further growth in underlying assets.

Upside from higher monetization of open interest on Boros:

- An additional upside lever relates to monetization efficiency rather than market size alone. In our model, we apply a blended take rate of approximately 0.5% on Boros open interest, reflecting early observed fees and accounting for product immaturity. This assumption remains conservative relative to external benchmarks. For example, Blockworks assumes a higher blended take rate, reaching up to 1.0% in its bull case scenario.

Risks

While our analysis suggests that Pendle appears undervalued under a range of conservative assumptions, it is important to recognize that both Pendle and, in particular, Boros remain at an early stage of development. As a result, the protocol’s long-term potential is accompanied by a set of meaningful risks that should be considered alongside the valuation.

Exposure to market volatility and TVL sensitivity

Recent market volatility (Jan-Feb, 2026) has weighed on the broader crypto market and has been especially visible in metrics such as TVL across yield-oriented protocols, including Pendle. As a yield-driven protocol, Pendle remains sensitive to shifts in risk appetite, leverage, and liquidity, which can lead to short-term volatility in activity and revenues, even if long-term fundamentals remain intact.

Sensitivity to yield levels and market cycles

Pendle’s revenues are structurally sensitive to yield levels, incentive programs, and trading activity around expiries, making the protocol more volatile than simple TVL-driven infrastructure. Periods of compressed yields, reduced leverage demand, or lower rate dispersion can lead to sharp drawdowns in activity and revenues across both Pendle V2 and Boros.

Dependence on rate dispersion and volatility

Demand for interest rate trading and hedging depends not only on the level of yields, but also on rate dispersion and volatility. A prolonged environment of low rate volatility or compressed funding spreads could dampen hedging demand and trading activity, particularly impacting Boros’ adoption and monetization.

Concentration risk in yield-bearing assets

While Pendle has diversified meaningfully beyond its early reliance on individual issuers, portions of TVL and activity remain concentrated in a limited number of high-yield assets and strategies. As of today, sUSDe, USDe, sUSDai, and USDai account for approximately 70.3% of assets deployed on the platform. Adverse developments affecting a major issuer, stablecoin, or yield source could temporarily impact protocol activity, revenue stability, and market sentiment.

Boros adoption and product complexity risk

Boros represents a meaningful expansion in scope and product complexity. Although it addresses a clear structural gap, crypto-native interest rate markets remain at an early stage of development. Achieving sustained liquidity, tight spreads, and consistent participation across maturities is non-trivial, and adoption may progress more slowly than modeled, particularly given the conceptual complexity of rate swaps, margining, and settlement mechanics.

Competitive pressure in onchain rate markets

As yield-bearing assets and interest rate trading become more central to DeFi, competitive pressure is likely to intensify. Both new entrants and existing derivatives venues — such as HyENA, Exponent or RateX — may attempt to capture portions of the onchain rate market. While Pendle currently benefits from strong network effects and early-mover advantages, these advantages may erode over time.

Recent market volatility (Jan-Feb, 2026) has weighed on the broader crypto market and has been especially visible in metrics such as TVL across yield-oriented protocols, including Pendle. As a yield-driven protocol, Pendle remains sensitive to shifts in risk appetite, leverage, and liquidity, which can lead to short-term volatility in activity and revenues, even if long-term fundamentals remain intact.

Sensitivity to yield levels and market cycles

Pendle’s revenues are structurally sensitive to yield levels, incentive programs, and trading activity around expiries, making the protocol more volatile than simple TVL-driven infrastructure. Periods of compressed yields, reduced leverage demand, or lower rate dispersion can lead to sharp drawdowns in activity and revenues across both Pendle V2 and Boros.

Dependence on rate dispersion and volatility

Demand for interest rate trading and hedging depends not only on the level of yields, but also on rate dispersion and volatility. A prolonged environment of low rate volatility or compressed funding spreads could dampen hedging demand and trading activity, particularly impacting Boros’ adoption and monetization.

Concentration risk in yield-bearing assets

While Pendle has diversified meaningfully beyond its early reliance on individual issuers, portions of TVL and activity remain concentrated in a limited number of high-yield assets and strategies. As of today, sUSDe, USDe, sUSDai, and USDai account for approximately 70.3% of assets deployed on the platform. Adverse developments affecting a major issuer, stablecoin, or yield source could temporarily impact protocol activity, revenue stability, and market sentiment.

Boros adoption and product complexity risk

Boros represents a meaningful expansion in scope and product complexity. Although it addresses a clear structural gap, crypto-native interest rate markets remain at an early stage of development. Achieving sustained liquidity, tight spreads, and consistent participation across maturities is non-trivial, and adoption may progress more slowly than modeled, particularly given the conceptual complexity of rate swaps, margining, and settlement mechanics.

Competitive pressure in onchain rate markets

As yield-bearing assets and interest rate trading become more central to DeFi, competitive pressure is likely to intensify. Both new entrants and existing derivatives venues — such as HyENA, Exponent or RateX — may attempt to capture portions of the onchain rate market. While Pendle currently benefits from strong network effects and early-mover advantages, these advantages may erode over time.

Final Thoughts

- Pendle began as a niche protocol focused on yield optimization, but has evolved into infrastructure for pricing, trading, and managing yield and interest rate risk onchain. This reflects a broader shift in crypto markets: yield is no longer just a side effect of incentives, but an input that increasingly shapes how capital is allocated, leveraged, and managed. By turning yield into tradable building blocks, Pendle has become a central venue for this transition, particularly as yield-bearing stablecoins grow in importance.

- The launch of Boros extends this role beyond individual yield markets and into interest rate derivatives. While still early, Boros introduces the basic components needed for onchain rate markets to function, including leverage, margining, ongoing settlement, and rates that are not tied to a single issuer. Even under cautious assumptions, Boros significantly expands Pendle’s potential revenue base and adds a source of upside that would be difficult to achieve through incremental product changes alone.

- Our valuation framework deliberately relies on cautious assumptions around market growth, monetization, and adoption, while highlighting where upside may emerge. The key question is not whether Pendle benefits from short-term yield cycles, but whether crypto develops widely used tools to manage interest rate risk. If that happens, Pendle is already well positioned to play a central role in that market.

P.S. Since finalizing this report, the market price of the Pendle token has declined to approximately $1.2, implying an even larger valuation discount relative to our estimates. Despite recent market volatility, we have not revised the core assumptions underlying our analysis and continue to view them as appropriate for assessing Pendle’s long-term fundamentals.