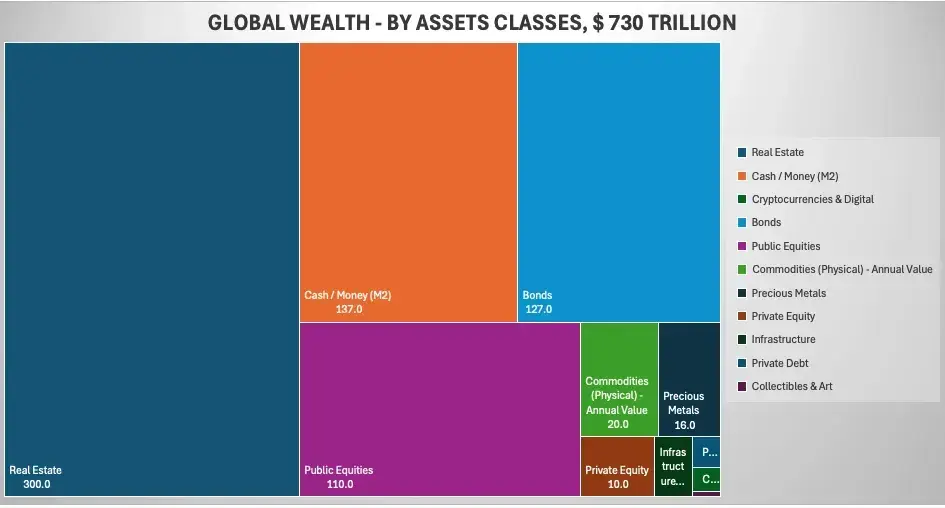

Liquidity serves as the foundational substrate of finance, with everything else essentially amounting to user experience enhancements. Throughout monetary history, each innovation has addressed underlying forms of fragmentation in how value is stored, transferred, and utilised, progressively unifying disparate systems into more cohesive networks. Direct barter suffered from the fragmentation of mismatched wants and needs, which commodity money overcame by introducing standardised, divisible stores of value that bridged isolated exchanges. Physical commodities, in turn, were fragmented by issues of portability, security, and scalability, prompting the rise of paper currency and central banking to consolidate trust and expand liquidity across broader economies. Even then, transactions remained fragmented by time, distance, and manual processes, leading to card networks and online payment systems that reduced latency and synchronized value flows in near-real time.

Today, blockchains represent the next logical evolutionary step, tackling the pervasive fragmentation of global finance—silos defined by jurisdictions, asset classes, and intermediaries—to forge a truly unified, borderless ledger. Capital markets remain divided into jurisdiction-specific silos, each governed by distinct rules and lacking composability, where a handful of entities capture maximum extractable value from isolated liquidity pools.

Today, blockchains represent the next logical evolutionary step, tackling the pervasive fragmentation of global finance—silos defined by jurisdictions, asset classes, and intermediaries—to forge a truly unified, borderless ledger. Capital markets remain divided into jurisdiction-specific silos, each governed by distinct rules and lacking composability, where a handful of entities capture maximum extractable value from isolated liquidity pools.

The inevitable progression leads toward a global, real-time, unified asset ledger—a single central marketplace encompassing all assets. As these fragmented pools merge into one cohesive system, price discovery transforms into a truly global process, capital formation gains unprecedented speed, and market access shifts from being the privilege of elites to a universal opportunity. This is what blockchains are building, and it is precisely what blockchain development should prioritise.

At its essence, "cryptocurrencies" primary offering is not decentralisation but synchronization: a singular ledger and state machine where assets transcend national boundaries and reside on a chain that's equally accessible by anyone. In the 21st century, capital formation will culminate in a world where companies bypass traditional exchanges like the NYSE to launch initial public offerings directly online, atomic swaps enable seamless asset exchanges across continents, and the processes of value creation, liquidity provision, and trading converge into a fully composable framework.

Imagine a teenager in Lagos earning tokenised equity in a cooperative AI venture via useful work, a pension fund in Tokyo acquiring tokenised farmland in Uruguay, leveraging zero-knowledge proofs of authenticity issued by the local administration, or a startup from South Africa raising capital from within 30 seconds tapping into the global pool of capital on a futarchy launchpad. These scenarios signal the end of "foreign" markets as we know them, collapsing everything into a unified asset ledger.

To understand this shift, consider the historical trajectory of cryptocurrency itself. In its early days, Bitcoin's whitepaper in 2008 framed the narrative around decentralisation as a rebellion against centralised financial institutions, emphasising peer-to-peer electronic cash free from trusted third parties. This ethos fuelled the cypherpunk movement, where ideals of privacy, censorship resistance, and distributed control dominated discussions. Ethereum expanded this in 2015 by introducing smart contracts, positioning decentralization as the core innovation for building "unstoppable" applications immune to shutdowns by governments or corporations. Projects like DAO hacks and the proliferation of decentralized exchanges (DEXs) in the 2017 ICO boom reinforced this: crypto was sold as a tool for disintermediation, empowering individuals over intermediaries.

Yet as the ecosystem matured, decentralization's costs became apparent. The 2020 DeFi summer on Ethereum highlighted the problem: users chased yields across siloed platforms like Uniswap and Aave, but fragmented liquidity, cross-chain friction, and congestion-driven fees created more barriers than traditional finance. Solana's 2021 rise with projects like Serum's onchain order book demonstrated an alternative path—sacrificing some decentralisation for synchronization, enabling liquidity aggregation that Ethereum couldn't achieve.

However, scaling issues plagued most networks through 2022-2023, from Solana's outages to Ethereum's continued prohibitive gas costs. As these technical problems gradually resolved - Solana's infrastructure stabilised, layer-2s matured, and new architectures emerged - a clearer picture has crystallised. The networks that prioritized synchronization over pure "decentralisation" consistently captured more real-world adoption. Hyperliquid's 2024-2025 dominance in derivatives represents the logical endpoint: a hyper-efficient, globally accesible venue that pools liquidity into one state machine, even at the cost of decentralisation.

At its essence, "cryptocurrencies" primary offering is not decentralisation but synchronization: a singular ledger and state machine where assets transcend national boundaries and reside on a chain that's equally accessible by anyone. In the 21st century, capital formation will culminate in a world where companies bypass traditional exchanges like the NYSE to launch initial public offerings directly online, atomic swaps enable seamless asset exchanges across continents, and the processes of value creation, liquidity provision, and trading converge into a fully composable framework.

Imagine a teenager in Lagos earning tokenised equity in a cooperative AI venture via useful work, a pension fund in Tokyo acquiring tokenised farmland in Uruguay, leveraging zero-knowledge proofs of authenticity issued by the local administration, or a startup from South Africa raising capital from within 30 seconds tapping into the global pool of capital on a futarchy launchpad. These scenarios signal the end of "foreign" markets as we know them, collapsing everything into a unified asset ledger.

To understand this shift, consider the historical trajectory of cryptocurrency itself. In its early days, Bitcoin's whitepaper in 2008 framed the narrative around decentralisation as a rebellion against centralised financial institutions, emphasising peer-to-peer electronic cash free from trusted third parties. This ethos fuelled the cypherpunk movement, where ideals of privacy, censorship resistance, and distributed control dominated discussions. Ethereum expanded this in 2015 by introducing smart contracts, positioning decentralization as the core innovation for building "unstoppable" applications immune to shutdowns by governments or corporations. Projects like DAO hacks and the proliferation of decentralized exchanges (DEXs) in the 2017 ICO boom reinforced this: crypto was sold as a tool for disintermediation, empowering individuals over intermediaries.

Yet as the ecosystem matured, decentralization's costs became apparent. The 2020 DeFi summer on Ethereum highlighted the problem: users chased yields across siloed platforms like Uniswap and Aave, but fragmented liquidity, cross-chain friction, and congestion-driven fees created more barriers than traditional finance. Solana's 2021 rise with projects like Serum's onchain order book demonstrated an alternative path—sacrificing some decentralisation for synchronization, enabling liquidity aggregation that Ethereum couldn't achieve.

However, scaling issues plagued most networks through 2022-2023, from Solana's outages to Ethereum's continued prohibitive gas costs. As these technical problems gradually resolved - Solana's infrastructure stabilised, layer-2s matured, and new architectures emerged - a clearer picture has crystallised. The networks that prioritized synchronization over pure "decentralisation" consistently captured more real-world adoption. Hyperliquid's 2024-2025 dominance in derivatives represents the logical endpoint: a hyper-efficient, globally accesible venue that pools liquidity into one state machine, even at the cost of decentralisation.

This trend for optimising towards synchronization profoundly improves global finance across key dimensions:

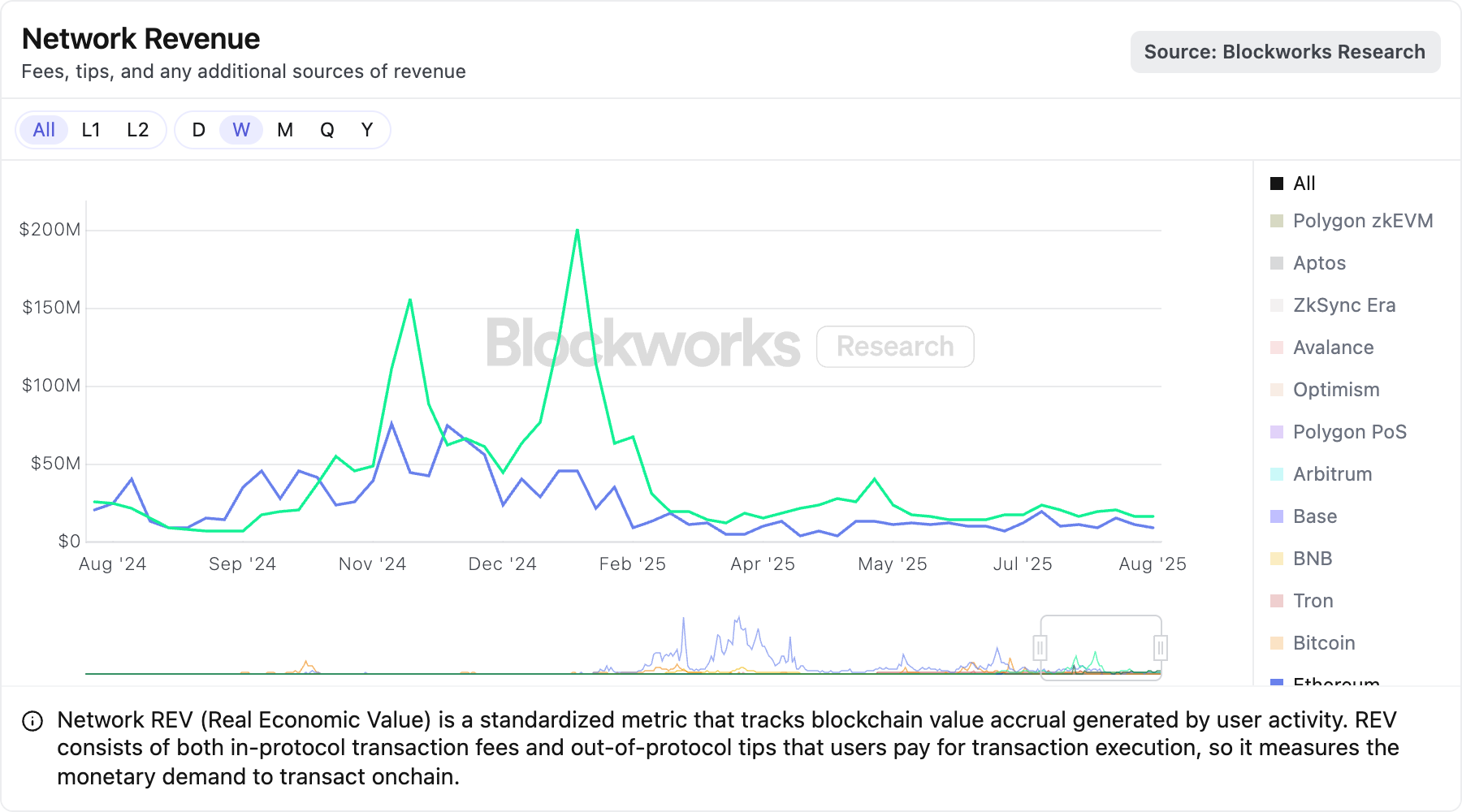

Solana’s rise in 2024 demonstrated the power of prioritising synchronization over pure decentralisation, outpacing the Ethereum ecosystem in revenue, throughput, and economic activity for over a year now.

- Price Discovery: In a fragmented world, prices vary wildly across borders and venues due to regulatory barriers, time zones, and information asymmetries—think of emerging market stocks trading at discounts due to limited access or delayed information. A unified onchain ledger synchronises data in real-time, drawing in diverse participants to refine prices continuously. For instance, Hyperliquid's perpetuals markets already provide tighter spreads and deeper liquidity than many traditional derivatives exchanges, as global traders contribute to a single order book. A prime example is the 2025 Pump.fun ICO, where PUMP tokens were initially traded as perpetual futures on Hyperliquid before the Token Generation Event. The deep liquidity and global participation on Hyperliquid led to such efficient price discovery that the perpetuals price closely matched the spot price post-TGE, leaving traders expecting volatility rollercoasters with minimal arbitrage opportunities. Hyperliquid’s model demonstrates how synchronised, borderless markets reduce volatility from isolated shocks, foster accurate valuations, and enable efficient resource allocation worldwide by including diverse participants from the outset.

- Capital Formation: Traditional fundraising is slow and elitist, gated by venture capitalists, investment banks, and listing requirements that favour established players. Traditional IPOs like Circle and Figma in 2025 excluded retail investors from early pricing, locking in fixed offer prices through private markets and leaving significant value inaccessible due to regulatory silos and limited participation. Synchronization accelerates this by enabling direct, onchain mechanisms: tokenised equity raises via automated smart contracts, where liquidity is bootstrapped instantly through integrated DEXs and order books. Solana's pump.fun in 2024 showed a glimpse, launching memecoins with immediate trading, but scaled up, this means startups in underserved regions can tap global capital pools without intermediaries. By 2025, we've seen ventures raise billions in tokenized rounds, with atomic settlements slashing timelines from months to minutes, democratizing innovation and channeling funds to high-potential ideas regardless of geography.

- Global Participation: Finance has long been a club for the wealthy and connected, excluding billions due to borders, KYC hurdles, and capital controls. Synchronization collapses these barriers, turning participation into a borderless right. The Lagos teenager earning AI equity isn't hypothetical—platforms like Hyperliquid wrappers already enable micro-investments in derivatives from anywhere with internet. Zero-knowledge tech ensures privacy-compliant access, while unified ledgers allow seamless integration of real-world assets (RWAs) like tokenised farmland. This inclusivity boosts economic mobility: a Jakarta shopper's NFT mortgage leverages global lenders for better rates, a Tokyo pension fund diversifies into emerging assets without forex friction, and overall, it amplifies network effects, where more participants deepen liquidity and create virtuous cycles of growth. In essence, synchronization doesn't just connect markets; it weaves a global fabric where value flows freely, empowering the periphery as much as the core.

Solana’s rise in 2024 demonstrated the power of prioritising synchronization over pure decentralisation, outpacing the Ethereum ecosystem in revenue, throughput, and economic activity for over a year now.

By optimising for high-speed, low-latency transactions, Solana enabled developers to launch applications for millions without overhauling its infrastructure, proving that a unified ledger could tackle global finance’s fragmentation more effectively than slower, siloed systems.

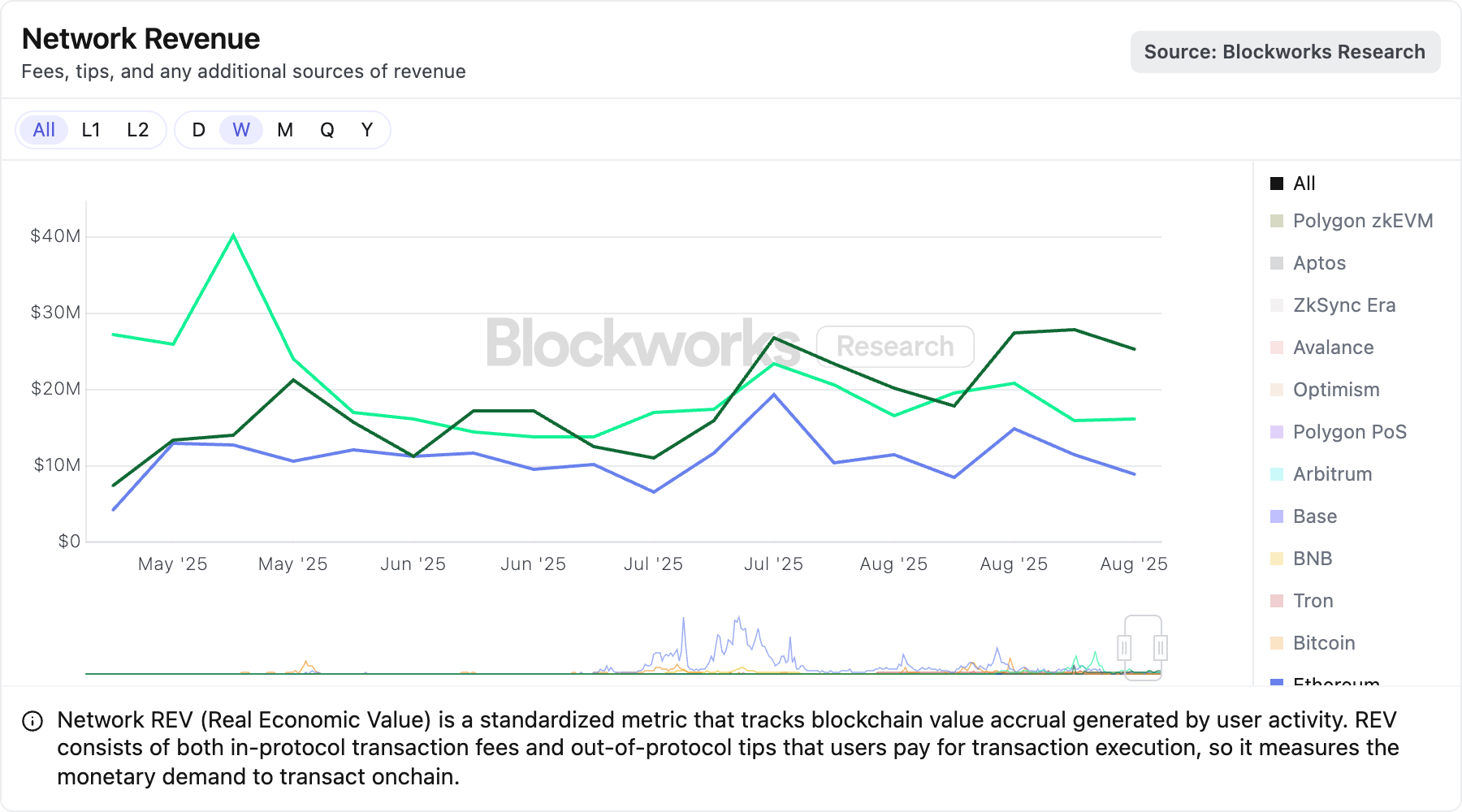

However, in 2025, Hyperliquid pushed this trend to an extreme, further accelerating outperformance and surpassing Solana’s derivatives trading volume and, subsequently, total revenue.

However, in 2025, Hyperliquid pushed this trend to an extreme, further accelerating outperformance and surpassing Solana’s derivatives trading volume and, subsequently, total revenue.

Hyperliquid's dominance highlights a core trade-off while exposing Solana's architectural limitations: by leveraging a single collocated sequencer for superior latency, Hyperliquid sacrifices decentralization, resembling a centralised database more than a transformative ledger.

However, Hyperliquid acknowledges this as a starting point, with explicit intentions to decentralize over time, viewing its current setup as a pragmatic step toward scaling rather than a permanent model. This approach contrasts with Solana, which, despite its versatile ecosystem, lacks the native, decentralized central limit order book infrastructure needed to compete for large-scale trading, pushing sophisticated traders toward purpose-built but temporarily centralised alternatives like Hyperliquid.

This dynamic reveals a broader flaw in 2025 crypto markets: by chasing speed at the expense of censorship resistance, onchain trading venues risk recreating the siloed, centralised systems they aim to replace, failing to address global wealth fragmentation.

True synchronization demands a decentralized, globally accessible ledger that unifies liquidity without relying on a single point of control. Solana has made strides toward this balance, while Hyperliquid's roadmap signals a commitment to evolve beyond its centralized starting point. This underscores that decentralisation, alongside speed, is critical for a unified financial system.

From here, three roadmaps emerge for the dominant chain that aims to synchronise global wealth markets:

1. Multi-Chain Federation Strategy

However, Hyperliquid acknowledges this as a starting point, with explicit intentions to decentralize over time, viewing its current setup as a pragmatic step toward scaling rather than a permanent model. This approach contrasts with Solana, which, despite its versatile ecosystem, lacks the native, decentralized central limit order book infrastructure needed to compete for large-scale trading, pushing sophisticated traders toward purpose-built but temporarily centralised alternatives like Hyperliquid.

This dynamic reveals a broader flaw in 2025 crypto markets: by chasing speed at the expense of censorship resistance, onchain trading venues risk recreating the siloed, centralised systems they aim to replace, failing to address global wealth fragmentation.

True synchronization demands a decentralized, globally accessible ledger that unifies liquidity without relying on a single point of control. Solana has made strides toward this balance, while Hyperliquid's roadmap signals a commitment to evolve beyond its centralized starting point. This underscores that decentralisation, alongside speed, is critical for a unified financial system.

From here, three roadmaps emerge for the dominant chain that aims to synchronise global wealth markets:

1. Multi-Chain Federation Strategy

Spin up multiple chains, each replicating traditional finance silos but with superior infrastructure. This approach proceeds from the assumption that building everything within a single general-purpose ledger is fundamentally impossible—that specialisation and federation are necessary given the inherent trade-offs between different financial use cases. Success hinges entirely on solving interoperability completely—creating seamless cross-chain communication and unified user experiences that make the underlying complexity invisible. This approach leverages familiar specialization while requiring shared settlement layers and coordination mechanisms. This strategy operates from strength, building upon mature ecosystems like Ethereum, Arbitrum, and Polygon that already host substantial DeFi infrastructure, developer communities, and established user bases.

2. Bottom-Up Strategy

2. Bottom-Up Strategy

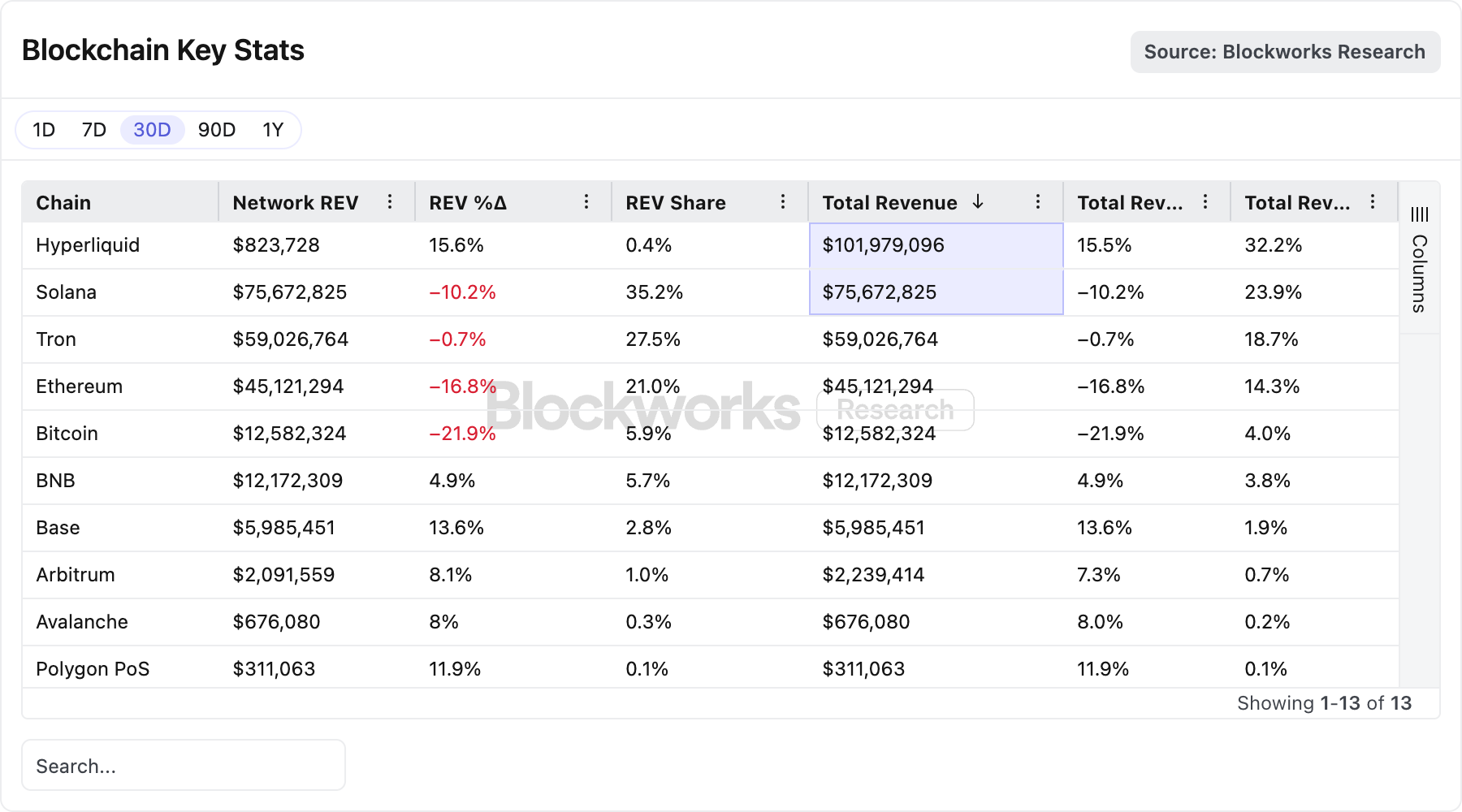

Bootstrap liquidity by dominating one core use case—such as derivatives—then expand from that foundation. Success depends on transcending the initial professional trader base, attracting institutional market makers, and constructing a general-purpose environment encompassing developers, applications, social platforms, gaming, and real-world assets. Initial trading volume becomes the engine funding comprehensive ecosystem development. This represents the cold start problem in its purest form—Hyperliquid has seemingly captured derivatives but operates with only 30-60k daily active addresses, a remarkably small user base that, regardless of how much these users spend, provides insufficient foundation for ecosystem development. The platform now faces the monumental challenge of building an entire ecosystem from this narrow starting point, despite achieving strong product-market fit in their vertical.

3. Infrastructure Optimisation Strategy

3. Infrastructure Optimisation Strategy

Solve technical bottlenecks preventing specific use cases like derivatives within existing ecosystems, enabling professional traders to migrate to already-built infrastructure. This strategy proceeds on the assumption that performance gaps are merely technical bugs that can be resolved within fat, general-purpose ledgers—that the right engineering talent can optimize existing systems to match or exceed specialized solutions. Success relies entirely on technical talent capable of addressing fundamental scaling, latency, and MEV challenges without starting fresh. This strategy leverages warm ecosystems—Solana's vibrant community, Ethereum L1’s deep liquidity, or Base's growing adoption - but requires overcoming entrenched technical debt while competing against purpose-built solutions.

Each path presents distinct trade-offs and starting positions. Federation models (1) and optimisation strategies (3) both operate from positions of strength with established ecosystems—existing liquidity, developer communities, and user bases provide significant advantages. The federation approach risks recreating fragmentation at higher levels but benefits from mature infrastructure, while optimisation strategies leverage existing network effects but must navigate entrenched technical debt and governance complexities.

The bottom-up approach (2) presents the starkest contrast: Hyperliquid has conquered derivatives through superior execution, yet now confronts the classic cold start dilemma of ecosystem development. With only 30-60k daily active addresses, the platform operates with a remarkably concentrated user base that, while high-value, represents a narrow foundation for broader ecosystem expansion. Building developer tooling, attracting applications, fostering community, and expanding beyond professional traders demands entirely different competencies than optimising trading infrastructure. The critical question becomes whether derivatives dominance provides sufficient momentum and resources to bootstrap a general-purpose blockchain ecosystem from such a limited starting point.

The prevailing investment conundrum in crypto centers on evaluating these three roadmaps, with capital allocators attempting to assess which path offers the most favorable risk-saturation profile and clearest execution pathway.

Each strategy presents distinct risk complexities: federation models require conviction in cross-chain infrastructure maturation and regulatory harmonisation across jurisdictions; bottom-up approaches involve backing teams capable of both technical excellence and ecosystem orchestration while scaling from minimal user bases; optimisation strategies depend on existing networks' capacity for fundamental evolution without fracturing established market share.

Despite divergent execution paths, all three strategies target the same ultimate system: a unified global ledger where a retail investor in Seoul allocates to reinsurance, swaps rates, and posts it as mortgage collateral inside a government app. Where a driver in Nairobi tokenises their car's telemetry and streams it for yield. Where an American clicks "buy" on a Brazilian startup like it's an ETF, and an ETF launches as casually as a memecoin.

This is financial infrastructure that treats every asset—from derivatives to real estate to intellectual property—as programmable units on a single, globally accessible ledger. The fragmentation of today's markets, where geographic boundaries, asset classes, and regulatory jurisdictions create artificial barriers, dissolves into seamless composability.

The correct investment framework evaluates each strategy through the pace of execution toward this end state. Strategy 3 offers the shortest path by building upon existing network effects and solving concrete technical challenges. Strategy 1 provides redundancy and specialisation but risks perpetuating into analysis-paralysis on the development side while people figure out who should build what. Strategy 2 demands building everything from scratch despite demonstrating only narrow product-market fit.

In this race to collapse global financial boundaries into programmable infrastructure, velocity of execution becomes the primary valuation metric. The network that first achieves seamless, scalable access to global wealth will capture the coordination premium of the entire financial system.

Unless, we all stop caring.

Each path presents distinct trade-offs and starting positions. Federation models (1) and optimisation strategies (3) both operate from positions of strength with established ecosystems—existing liquidity, developer communities, and user bases provide significant advantages. The federation approach risks recreating fragmentation at higher levels but benefits from mature infrastructure, while optimisation strategies leverage existing network effects but must navigate entrenched technical debt and governance complexities.

The bottom-up approach (2) presents the starkest contrast: Hyperliquid has conquered derivatives through superior execution, yet now confronts the classic cold start dilemma of ecosystem development. With only 30-60k daily active addresses, the platform operates with a remarkably concentrated user base that, while high-value, represents a narrow foundation for broader ecosystem expansion. Building developer tooling, attracting applications, fostering community, and expanding beyond professional traders demands entirely different competencies than optimising trading infrastructure. The critical question becomes whether derivatives dominance provides sufficient momentum and resources to bootstrap a general-purpose blockchain ecosystem from such a limited starting point.

The prevailing investment conundrum in crypto centers on evaluating these three roadmaps, with capital allocators attempting to assess which path offers the most favorable risk-saturation profile and clearest execution pathway.

Each strategy presents distinct risk complexities: federation models require conviction in cross-chain infrastructure maturation and regulatory harmonisation across jurisdictions; bottom-up approaches involve backing teams capable of both technical excellence and ecosystem orchestration while scaling from minimal user bases; optimisation strategies depend on existing networks' capacity for fundamental evolution without fracturing established market share.

Despite divergent execution paths, all three strategies target the same ultimate system: a unified global ledger where a retail investor in Seoul allocates to reinsurance, swaps rates, and posts it as mortgage collateral inside a government app. Where a driver in Nairobi tokenises their car's telemetry and streams it for yield. Where an American clicks "buy" on a Brazilian startup like it's an ETF, and an ETF launches as casually as a memecoin.

This is financial infrastructure that treats every asset—from derivatives to real estate to intellectual property—as programmable units on a single, globally accessible ledger. The fragmentation of today's markets, where geographic boundaries, asset classes, and regulatory jurisdictions create artificial barriers, dissolves into seamless composability.

The correct investment framework evaluates each strategy through the pace of execution toward this end state. Strategy 3 offers the shortest path by building upon existing network effects and solving concrete technical challenges. Strategy 1 provides redundancy and specialisation but risks perpetuating into analysis-paralysis on the development side while people figure out who should build what. Strategy 2 demands building everything from scratch despite demonstrating only narrow product-market fit.

In this race to collapse global financial boundaries into programmable infrastructure, velocity of execution becomes the primary valuation metric. The network that first achieves seamless, scalable access to global wealth will capture the coordination premium of the entire financial system.

Unless, we all stop caring.