Authors: Katarina Keller, Mark Leontev

This report assumes basic familiarity with Helium's history, the DC/HNT mechanism, and the broader DePIN sector. We focus on the 2025–Q1 2026 inflection, where carrier-offload DC burn moved from partial emission coverage to full coverage over three quarters, culminating in Q1 2026 when burn exceeded HNT emissions for the first time. We then apply a sum-of-the-parts framework to estimate HNT's implied value under explicit operating assumptions.

Important note on valuation framework: our goal is not to arrive at a single "fair value," but to build a framework for thinking about what needs to be true for HNT to be worth 5x+ today on a discounted basis.

Important Caveat on Recent Developments

Two post-completion developments materially affect how to read this report. On June 2, 2026, Helium Mobile announced that it is being acquired by Noble Mobile, which has committed to use the Helium Network; terms, purchase price, closing structure, and implications for Nova Labs / HNT integration remain undisclosed. More important for HNT, HIP-149 would reset Mobile economics: lower carrier offload burn rates, eliminate PoC rewards, shift emissions toward usage-serving deployers and operations, and add a separate ~141M HNT capitalization stream over 36 months.

Our high-level read is: it is a token-holder-funded recapitalization plus a price-discovery experiment. That may be rational for Helium as an operating network: $0.50/GB appears to have validated carrier interest but not forced scaled adoption, and $0.10/GB may convert pilots into recurring volume. But it is a bearish HNT event unless that volume response arrives quickly enough to offset lower pricing, added issuance, and deployer sell pressure.

The report below should therefore be read as a pre-HIP-149 framework, not a current fair-value model. The investment question has changed from "is carrier demand real?" to "what share of carrier economics can HNT capture after repricing and recapitalization?" If HIP-149 passes as written, the old $0.42/GB protocol revenue path, 30% integration dilution assumption, and supply denominator are stale.

Thesis Summary

- Helium appears to be the first scaled DePIN to cross into structural net-deflation on its core protocol economics. Q1 2026 Coverage Ratio reached 149%, up from 54% in Q4 2025 and 17% in Q3 2025 — a three-quarter progression of sharply improving burn coverage. The mechanism is simple: network usage is paid in Data Credits, and Data Credits are created by burning HNT. That makes the supply effect automatic, transparent, and immediate.

- Carrier offload demand is concentrated on two Tier-1 partners (widely understood to be T-Mobile and AT&T) which together represent nearly 100% of identified offload volume. Q1 2026 throughput grew +63.8% QoQ on a +0.7% deployer-base expansion — the textbook signature of a maturing utility monetizing existing infrastructure rather than expanding capacity.

- HNT is structurally separate from Helium Mobile. HNT is exposed to Helium Network economics — mainly DC burn versus HNT emissions — while Helium Mobile, the retail MVNO, is operated by Nova Labs, a private company that raised $250M+ from a16z, Deutsche Telekom, and Tiger Global. This dual structure creates an alignment problem. The most discussed path to unifying the two is an equity-to-token integration, in which Nova Labs' Helium Mobile equity value would be bridged into HNT. To keep the valuation conservative, we model that integration as new HNT issuance equal to 30% of the pre-integration supply base.

- By 2030E, the combined entity generates ~$916M of revenue across the two blocks: Helium Mobile $708M revenue / $133M EBITDA (19% margin) and Helium Protocol $208M adjusted revenue / 93% net margin. The protocol forecast is anchored on a 5% share of the US Mobile Offload Market (WiseGuy Reports, $5.45B in 2030E).

- Our Base case implies $5.93 per HNT — a 7.4x upside from the current $0.80 price. The calculation takes combined SOTP enterprise value of $1.72bn (Helium Mobile PV of $559M at a 20% discount rate + Protocol PV of $1,161M at a 40% discount rate) and divides it by modeled post-integration supply of 289.9M HNT. The Protocol multiple of 30x EV/Revenue is set against DePIN FDV/Rev benchmarks (median ~42x, average ex-100x+ outliers ~48x) — a deliberately conservative reading relative to DePIN token comps at ~71% of the FDV/Rev median. HNT valuation has compressed ~80% from the start of 2025 ($4.00) and 98% from ATH ($54.88) while operating fundamentals have improved.

- Four upside catalysts are excluded from the Base case: (i) international scale (LATAM, Mexico, Brazil); (ii) deployer-base expansion through Helium Plus and Ameriband; (iii) carrier expansion beyond T-Mobile/AT&T (Verizon, international Tier-1s); and (iv) financial services layered onto the telecom subscriber base. Each is treated as embedded option value.

- The setup is structurally asymmetric: the operating business is deflationary and accelerating, while the token trades at multiples that imply survival risk. That risk is no longer supported by the carrier offload trajectory or post-halving economics. The question is what HNT is worth on these fundamentals, and what conditions would close the disconnect. The market still appears to treat HNT as a failed DePIN emissions story: IoT never became economically material, token incentives diluted holders, Helium Mobile value sits outside HNT, and carrier-offload revenue is still viewed as too early or too concentrated to underwrite. Our view is narrower and more falsifiable. Helium has crossed from subsidized supply-building into usage-funded economics: carrier-offload DC burn now covers HNT emissions, the post-halving emission base is lower, and the Base case does not require new carriers, international expansion, or financial-services upside. If offload burn continues scaling, HNT should be repriced from a survival-risk token to a revenue-backed infrastructure asset.

Section 1. The DePIN Sector at an Inflection Point

The Decentralized Physical Infrastructure Networks (DePIN) sector uses token incentives to deploy and operate physical infrastructure that has historically been built by capital-intensive incumbents: wireless networks, compute, storage, energy systems, sensor networks, mapping, and geospatial data. The premise is that token rewards bootstrap supply (operators deploying hardware), and that real-world demand for the underlying service generates the burn or buyback flows that close the economic loop. Helium is one of the longest-running and most operationally advanced examples of this model.

The DePIN Trade-Off

DePIN is often framed as a breakthrough in capital formation: a way to enter capital-intensive industries without raising and spending the full infrastructure budget upfront. That framing is directionally right, but too one-sided. From an investor's perspective, DePIN does not eliminate the cost of building supply. It shifts that cost from corporate capex to token issuance, with token holders funding the early network before demand is proven.

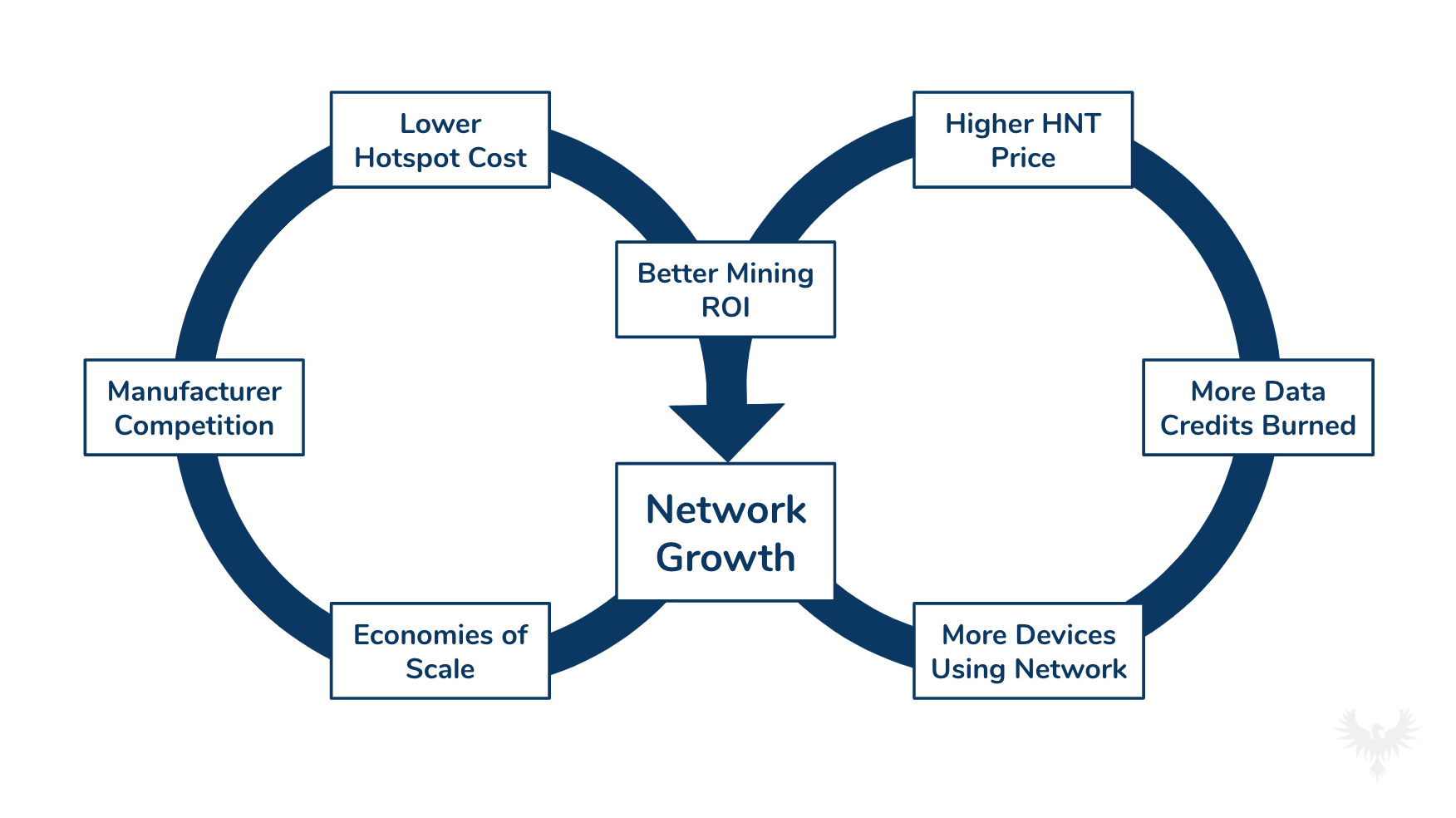

That trade-off matters most in industries where the chicken-and-egg problem is severe. Telecom is the cleanest example: users do not come without coverage, but coverage is prohibitively expensive to build before users arrive. Token incentives can solve that coordination problem by paying distributed participants to build supply first, letting a startup enter infrastructure markets that would normally be closed to it.

But the same mechanism can be unattractive for liquid token investors. For venture capital, early network formation may be acceptable if the entry valuation, structure, and time horizon compensate for the risk. For a liquid fund buying the token in the public market, the setup is different. The investor is exposed to ongoing emissions, operator selling, and dilution before the network has enough real demand to absorb the cost of bootstrapping. This is why many DePIN projects can show impressive supply growth while still destroying token-holder value: the network may be growing, but the cost of that growth is being pushed through the token.

The threshold arrives when real usage begins to pay for the network, shifting the debate from whether the project is exciting to whether it is investable. This is why Helium matters in the current DePIN cycle. As shown below, Helium appears to be the first scaled DePIN to cross the deflationary threshold on its primary business, and the move does not look like a one-quarter anomaly. Helium is no longer just proving it can create supply; carrier usage is beginning to pay for that supply. The quarterly progression points to something structural: carrier demand is rising, emissions have stepped down after the halving, and the network is beginning to fund itself through usage rather than subsidies.

Market Sizing

Public estimates of DePIN's addressable market vary by an order of magnitude depending on methodology and time horizon:

Together, these data points show rising measurable revenue alongside compressed token valuations.

Token Prices Have Decoupled From Revenue

The DePIN class of 2018–2022 — HNT, FIL, AKT, HONEY, DIMO, LPT — is down 94–99% from all-time highs, mirroring the broader crypto drawdown but compressed by additional sector-specific overhangs (regulatory uncertainty, narrative rotation, large-holder forced selling). The market is implicitly pricing in low survival probability across the sector.

The underlying revenue trajectory tells a different story. Per Messari, DePIN revenue growth has held up better than DeFi or Layer-1 comparables in the same drawdown window: the top-performing DePINs grew protocol revenue +801% and +170% YoY (December 2024 → December 2025), while DeFi and Layer-1 revenues compressed across the board. The distinction is not only growth, but revenue quality. The best DePIN revenue is tied to recurring real-world usage, not reflexive blockchain activity. That makes carrier offload closer to utility revenue than to trading-volume-driven protocol fees, and it is the central setup for the sector.

Several DePINs Are Converging on Net-Deflation

A small cohort of revenue-generating networks now have observable burn or buyback flows that can be measured against ongoing token issuance. Each is at a different point on the path to net-deflation:

These networks share a common pattern — token price drawdowns of 60–95% YTD masking accelerating fundamentals — and represent the most liquid expressions of the "DePIN with real revenue" thesis.

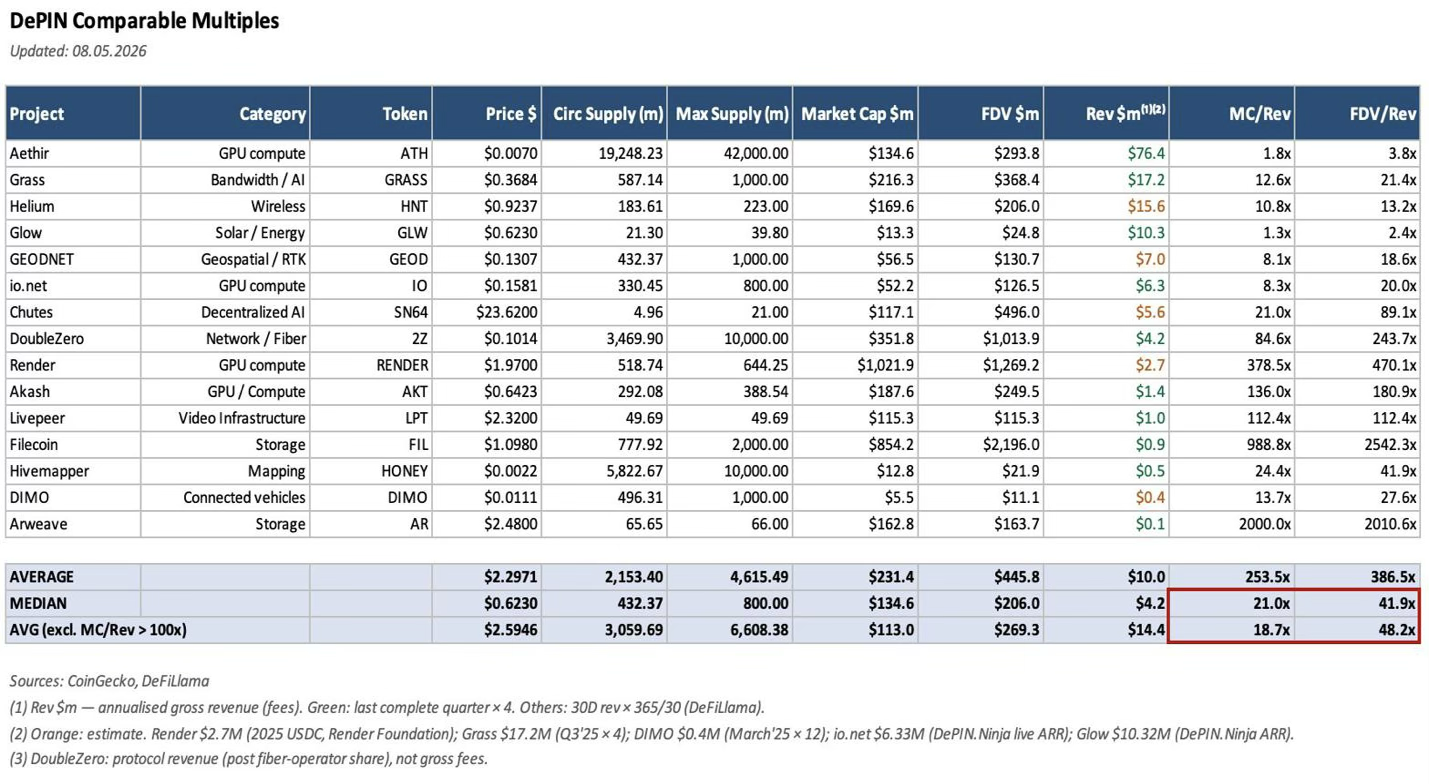

DePIN Comparable Multiples

The table below summarizes current trading multiples across revenue-generating DePIN tokens.

The DePIN Trade-Off

DePIN is often framed as a breakthrough in capital formation: a way to enter capital-intensive industries without raising and spending the full infrastructure budget upfront. That framing is directionally right, but too one-sided. From an investor's perspective, DePIN does not eliminate the cost of building supply. It shifts that cost from corporate capex to token issuance, with token holders funding the early network before demand is proven.

That trade-off matters most in industries where the chicken-and-egg problem is severe. Telecom is the cleanest example: users do not come without coverage, but coverage is prohibitively expensive to build before users arrive. Token incentives can solve that coordination problem by paying distributed participants to build supply first, letting a startup enter infrastructure markets that would normally be closed to it.

But the same mechanism can be unattractive for liquid token investors. For venture capital, early network formation may be acceptable if the entry valuation, structure, and time horizon compensate for the risk. For a liquid fund buying the token in the public market, the setup is different. The investor is exposed to ongoing emissions, operator selling, and dilution before the network has enough real demand to absorb the cost of bootstrapping. This is why many DePIN projects can show impressive supply growth while still destroying token-holder value: the network may be growing, but the cost of that growth is being pushed through the token.

The threshold arrives when real usage begins to pay for the network, shifting the debate from whether the project is exciting to whether it is investable. This is why Helium matters in the current DePIN cycle. As shown below, Helium appears to be the first scaled DePIN to cross the deflationary threshold on its primary business, and the move does not look like a one-quarter anomaly. Helium is no longer just proving it can create supply; carrier usage is beginning to pay for that supply. The quarterly progression points to something structural: carrier demand is rising, emissions have stepped down after the halving, and the network is beginning to fund itself through usage rather than subsidies.

Market Sizing

Public estimates of DePIN's addressable market vary by an order of magnitude depending on methodology and time horizon:

- World Economic Forum's Technology Convergence Report (June 2025) values the sector at $30–50bn today across 1,500+ active projects and projects it could expand to $3.5T by 2028, driven by the convergence of blockchain incentives with AI infrastructure demand.

- Token-market aggregators are more conservative. DePIN-tagged tokens on CoinMarketCap and CoinGecko represent roughly $9–10bn in circulating market cap as of mid-2026.

- Messari's State of DePIN (January 2026) marks the sector at $10bn in market cap and ~$72M in FY25 on-chain revenues — up from $5M in 2023 — with clear acceleration in monetization.

Together, these data points show rising measurable revenue alongside compressed token valuations.

Token Prices Have Decoupled From Revenue

The DePIN class of 2018–2022 — HNT, FIL, AKT, HONEY, DIMO, LPT — is down 94–99% from all-time highs, mirroring the broader crypto drawdown but compressed by additional sector-specific overhangs (regulatory uncertainty, narrative rotation, large-holder forced selling). The market is implicitly pricing in low survival probability across the sector.

The underlying revenue trajectory tells a different story. Per Messari, DePIN revenue growth has held up better than DeFi or Layer-1 comparables in the same drawdown window: the top-performing DePINs grew protocol revenue +801% and +170% YoY (December 2024 → December 2025), while DeFi and Layer-1 revenues compressed across the board. The distinction is not only growth, but revenue quality. The best DePIN revenue is tied to recurring real-world usage, not reflexive blockchain activity. That makes carrier offload closer to utility revenue than to trading-volume-driven protocol fees, and it is the central setup for the sector.

Several DePINs Are Converging on Net-Deflation

A small cohort of revenue-generating networks now have observable burn or buyback flows that can be measured against ongoing token issuance. Each is at a different point on the path to net-deflation:

- Helium crossed into net-deflation on its core protocol economics in Q1 2026, with Coverage Ratio reaching 149% (up from 54% in Q4 2025). This is the second consecutive quarter of structural improvement and the most advanced position among DePINs of comparable size.

- GEODNET sits at 93.2% of issuance offset by burns as of early May 2026 (per Blockworks data). The network generates ~$7M+ ARR (December 2025) with 80% of revenue routed to GEOD buyback-and-burn — putting net deflation within reach in the coming quarters.

- Hivemapper has now mapped approximately 33% of the global road network, and signed enterprise customers including Volkswagen ADMT (autonomous fleet) and Lyft. Revenue remains modest (~$0.5M annualized) but the burn-and-mint structure is in place.

- DIMO has expanded to 190K+ connected vehicles (+42% YoY), 800 developers, and ~$250K ARR (per Messari State of DePIN, Jan 2026). Protocol monetization is earlier-stage, but the developer licensing model is showing traction.

These networks share a common pattern — token price drawdowns of 60–95% YTD masking accelerating fundamentals — and represent the most liquid expressions of the "DePIN with real revenue" thesis.

DePIN Comparable Multiples

The table below summarizes current trading multiples across revenue-generating DePIN tokens.

Setting aside the narrative-era names trading at 100x+ revenue — Render (378x), Akash (136x), Filecoin (988x), Arweave (2,000x), and Livepeer (112x) — the remaining revenue-generating DePIN tokens cluster in a 1.3–25x MC/Rev band, with a median of 21x and an average of 18.7x excluding >100x outliers. That is infrastructure-style pricing, not crypto-style pricing. Networks like Aethir (1.8x), Glow (1.3x), GEODNET (8.1x), io.net (8.3x), Helium (10.8x), and Grass (12.6x) are being valued on multiples closer to public infrastructure and growth-stage software businesses than to narrative-driven crypto assets. FDV/Rev multiples are higher — median ~42x, average ex-outliers ~48x — and we use FDV/Rev as the relevant forward benchmark because expected supply growth, halvings, and modeled issuance matter for HNT valuation.

This marks a shift in how the sector is being valued. Revenue-generating DePINs now trade closer to infrastructure multiples, creating rerating potential if usage-backed revenue continues to grow from compressed token prices. The narrative-era cohort faces the opposite dynamic.

By absolute protocol revenue, Helium is one of the largest revenue generators on this list at $15.6M annualized (Q1 2026 run-rate; Helium Network protocol revenue, excluding Helium Mobile retail subscription revenue), and appears to be the only scaled DePIN that has crossed into net-deflation on its primary business.

Where Helium Sits

Among this cohort, Helium combines several distinctive characteristics:

This marks a shift in how the sector is being valued. Revenue-generating DePINs now trade closer to infrastructure multiples, creating rerating potential if usage-backed revenue continues to grow from compressed token prices. The narrative-era cohort faces the opposite dynamic.

By absolute protocol revenue, Helium is one of the largest revenue generators on this list at $15.6M annualized (Q1 2026 run-rate; Helium Network protocol revenue, excluding Helium Mobile retail subscription revenue), and appears to be the only scaled DePIN that has crossed into net-deflation on its primary business.

Where Helium Sits

Among this cohort, Helium combines several distinctive characteristics:

- The most advanced position on net-deflation. Helium appears to be the only scaled DePIN to have crossed into burn coverage above 100% on its primary revenue stream, following two consecutive quarters of sharply improving coverage.

- A direct line from network usage to token deflation. Unlike buyback-and-burn structures (GEODNET, Render Foundation), where revenue must first be collected in fiat or stablecoin and then deployed to repurchase tokens, Helium's DC mechanism creates Data Credits by burning HNT. The supply effect is automatic, transparent, and immediate.

- An identifiable, recurring enterprise demand source. Helium's revenue acceleration is driven by Tier-1 carrier offload partnerships (widely understood to include T-Mobile and AT&T), not crypto-native customers. That matters because the demand source is usage-based and operational, not speculative. It is the kind of demand base that survives crypto cycles.

Section 2. What is Helium and How It Works

Origins and Evolution

Helium was founded in 2013 by Amir Haleem, Shawn Fanning, and Sean Carey to build peer-to-peer wireless networks. The defining feature of the project — and the one most relevant for understanding its current economics — is that the network has cycled through three distinct underlying wireless technologies, each with materially different capex requirements, unit economics, and addressable markets. Helium today operates very differently from how it was originally designed, and the trajectory between phases explains both the historical revenue gap and the recent inflection.

Phase 1: IoT / LoRaWAN (2019–2022). Helium launched its native Layer-1 blockchain in 2019 around LoRaWAN, a low-power long-range protocol designed for sensor networks. Operators were rewarded in HNT for deploying dedicated IoT hotspots and providing coverage. The IoT phase served as the proof-of-concept for the entire DePIN category — token incentives demonstrably bootstrapped a globally distributed physical network at scale. The economic flaw was on the demand side: sensor traffic generated minimal data volume and therefore minimal DC burn, leaving the network rich in coverage but structurally under-monetized.

That distinction still matters for valuation. IoT can remain useful and still be economically immaterial to HNT because LoRaWAN messages are tiny and priced in small packet increments. Usage would need to scale by orders of magnitude before IoT DC burn could rival mobile offload. We therefore treat IoT as a legacy/maintenance network rather than a core valuation driver.

Phase 2: CBRS / cellular small cells (2023–early 2025). Helium pivoted to LTE cellular coverage using Citizens Broadband Radio Service (CBRS), a shared U.S. spectrum band. The architecture required operators to deploy dedicated indoor small-cell hardware to extend cellular coverage in dense urban areas. Structurally, the model did not work: the hardware was expensive, deployment was operationally complex, and indoor cells generated limited actual offload because most handsets and carriers were not configured to authenticate against CBRS coverage without explicit carrier-side integration. Coverage existed; utilization didn't follow. The community ultimately passed HIP 139 in early 2025 to phase out CBRS support entirely.

Phase 3: Wi-Fi offload (early 2025–present). The current phase reorients the network around Wi-Fi offload — and is the first architecture where Helium has demonstrated genuine product-market fit. The thesis is grounded in a basic reality of mobile data traffic: 70–80% of usage originates indoors, where cellular signals are weak and handsets already default to Wi-Fi by design. The advantage is not better radio technology in isolation; it is a different deployment model. Helium turns low-ROI indoor coverage into distributed supply that carriers can tap only when data is actually flowing, rather than requiring them to fund dense, fragmented locations themselves. That makes the model complementary to carriers rather than directly adversarial.

Helium does not need to replace nationwide carrier infrastructure to matter. It only needs to monetize offload demand in the indoor locations carriers least want to overbuild. Carrier offload through Helium's hotspot network became the dominant revenue source, accounting for over 85% of DC burn by mid-2025 and continuing to accelerate through Q1 2026. This is the phase that produced the inflection in the network's economics, and is the one being underwritten in this report.

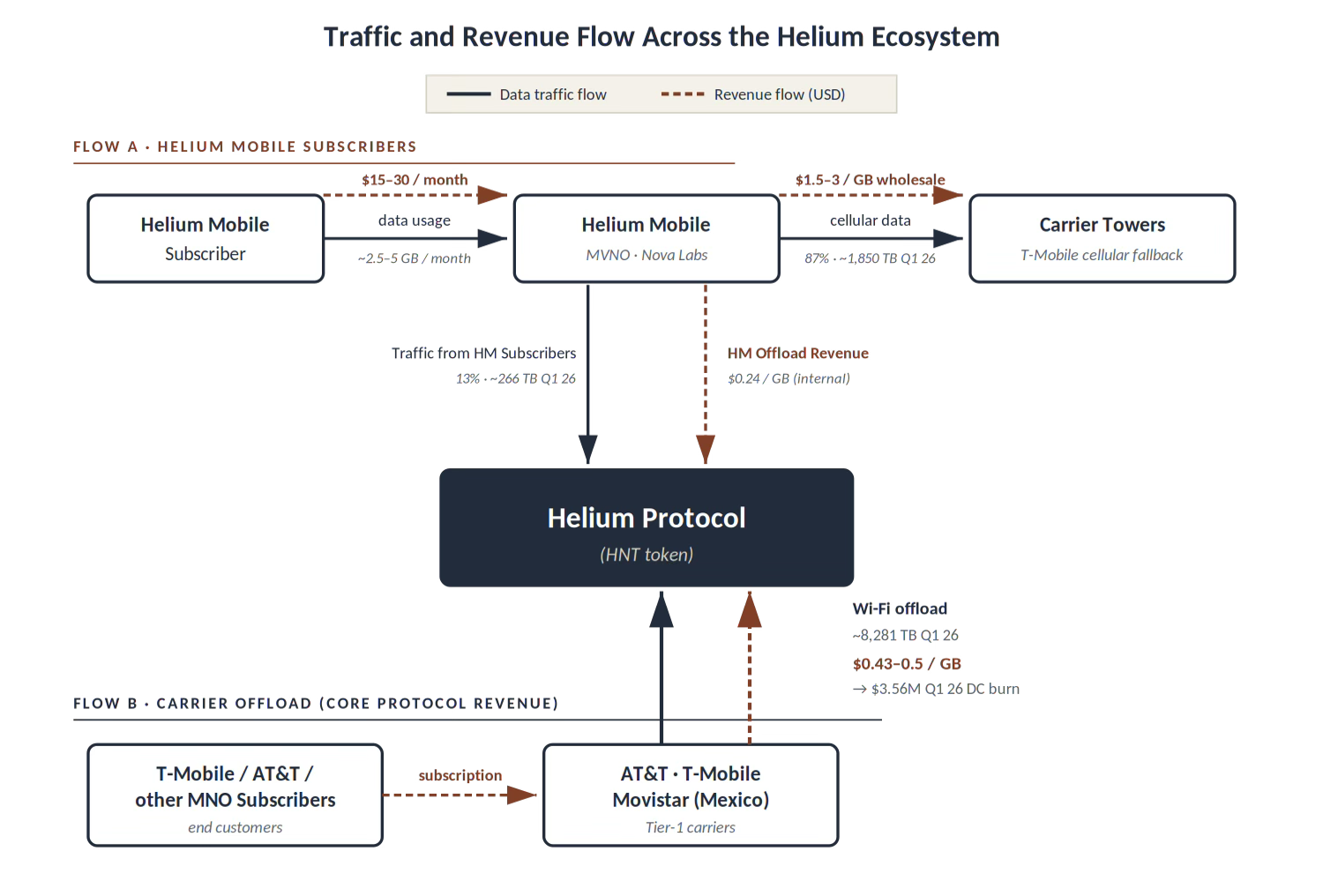

Helium Network and Helium Mobile: Two Distinct Entities

A common point of confusion — and one that materially affects how HNT should be valued — is that "Helium" refers to two structurally separate things. Throughout this report, we treat them as distinct economic entities and analyze each on its own terms.

Helium Network is the protocol: the HNT token, the deployed hotspot infrastructure, and the DC/HNT burn mechanism. The Network's revenue is the DC burn that flows through it — whether the source is a wholesale carrier paying per gigabyte for offload, an IoT device, or a retail subscriber consuming data. Its main cost is HNT emissions paid to deployers. HNT holders are economically exposed to the spread between those two flows: DC burn reduces token supply, while emissions increase it.

Helium Mobile is a retail MVNO operated by Nova Labs (formerly Helium Inc., the founding entity) as the first Service Provider on the Network. It sells $15–30/month plans to consumers, pays T-Mobile for fallback cellular data, and creates DC burn when subscriber traffic is carried on Helium hotspots. Helium Mobile sits inside Nova Labs, a private company that has raised over $250M across multiple rounds, including a $200M Series D led by a16z, Deutsche Telekom, and Tiger Global at a $1.2–1.5B valuation. Its retail business value belongs to Nova Labs shareholders, not HNT holders.

Helium was founded in 2013 by Amir Haleem, Shawn Fanning, and Sean Carey to build peer-to-peer wireless networks. The defining feature of the project — and the one most relevant for understanding its current economics — is that the network has cycled through three distinct underlying wireless technologies, each with materially different capex requirements, unit economics, and addressable markets. Helium today operates very differently from how it was originally designed, and the trajectory between phases explains both the historical revenue gap and the recent inflection.

Phase 1: IoT / LoRaWAN (2019–2022). Helium launched its native Layer-1 blockchain in 2019 around LoRaWAN, a low-power long-range protocol designed for sensor networks. Operators were rewarded in HNT for deploying dedicated IoT hotspots and providing coverage. The IoT phase served as the proof-of-concept for the entire DePIN category — token incentives demonstrably bootstrapped a globally distributed physical network at scale. The economic flaw was on the demand side: sensor traffic generated minimal data volume and therefore minimal DC burn, leaving the network rich in coverage but structurally under-monetized.

That distinction still matters for valuation. IoT can remain useful and still be economically immaterial to HNT because LoRaWAN messages are tiny and priced in small packet increments. Usage would need to scale by orders of magnitude before IoT DC burn could rival mobile offload. We therefore treat IoT as a legacy/maintenance network rather than a core valuation driver.

Phase 2: CBRS / cellular small cells (2023–early 2025). Helium pivoted to LTE cellular coverage using Citizens Broadband Radio Service (CBRS), a shared U.S. spectrum band. The architecture required operators to deploy dedicated indoor small-cell hardware to extend cellular coverage in dense urban areas. Structurally, the model did not work: the hardware was expensive, deployment was operationally complex, and indoor cells generated limited actual offload because most handsets and carriers were not configured to authenticate against CBRS coverage without explicit carrier-side integration. Coverage existed; utilization didn't follow. The community ultimately passed HIP 139 in early 2025 to phase out CBRS support entirely.

Phase 3: Wi-Fi offload (early 2025–present). The current phase reorients the network around Wi-Fi offload — and is the first architecture where Helium has demonstrated genuine product-market fit. The thesis is grounded in a basic reality of mobile data traffic: 70–80% of usage originates indoors, where cellular signals are weak and handsets already default to Wi-Fi by design. The advantage is not better radio technology in isolation; it is a different deployment model. Helium turns low-ROI indoor coverage into distributed supply that carriers can tap only when data is actually flowing, rather than requiring them to fund dense, fragmented locations themselves. That makes the model complementary to carriers rather than directly adversarial.

Helium does not need to replace nationwide carrier infrastructure to matter. It only needs to monetize offload demand in the indoor locations carriers least want to overbuild. Carrier offload through Helium's hotspot network became the dominant revenue source, accounting for over 85% of DC burn by mid-2025 and continuing to accelerate through Q1 2026. This is the phase that produced the inflection in the network's economics, and is the one being underwritten in this report.

Helium Network and Helium Mobile: Two Distinct Entities

A common point of confusion — and one that materially affects how HNT should be valued — is that "Helium" refers to two structurally separate things. Throughout this report, we treat them as distinct economic entities and analyze each on its own terms.

Helium Network is the protocol: the HNT token, the deployed hotspot infrastructure, and the DC/HNT burn mechanism. The Network's revenue is the DC burn that flows through it — whether the source is a wholesale carrier paying per gigabyte for offload, an IoT device, or a retail subscriber consuming data. Its main cost is HNT emissions paid to deployers. HNT holders are economically exposed to the spread between those two flows: DC burn reduces token supply, while emissions increase it.

Helium Mobile is a retail MVNO operated by Nova Labs (formerly Helium Inc., the founding entity) as the first Service Provider on the Network. It sells $15–30/month plans to consumers, pays T-Mobile for fallback cellular data, and creates DC burn when subscriber traffic is carried on Helium hotspots. Helium Mobile sits inside Nova Labs, a private company that has raised over $250M across multiple rounds, including a $200M Series D led by a16z, Deutsche Telekom, and Tiger Global at a $1.2–1.5B valuation. Its retail business value belongs to Nova Labs shareholders, not HNT holders.

Two distinct flows of traffic and revenue. Helium Mobile subscribers generate retail subscription revenue for Nova Labs; when their traffic is carried on the Helium Network, it also creates DC burn for the Protocol. Carrier offload traffic comes from partner MNO/MVNO subscribers and generates wholesale DC burn for the Protocol, making it the core protocol revenue source.

Why this distinction matters. HNT is exposed to Helium Network economics, not to Helium Mobile's full subscription business. When Helium Mobile collects $30 of monthly subscription revenue, the Protocol only receives the DC burn tied to that subscriber's actual usage on Helium hotspots, typically a small fraction of headline ARPU. The retail margin, brand, customer relationships, and MVNO equity value sit with Nova Labs.

Nova Labs sits on both sides of this structure. It operates Helium Mobile, has influence in Network governance through its founding role, and holds an HNT-denominated treasury. Its incentives are partly aligned with HNT — Amir Haleem has publicly stated that Nova Labs has refrained from token sales — but the separation between Nova Labs equity and HNT can still create tension. The clearest pressure point is pricing: how much should Helium Mobile and other Service Providers pay the Network per GB? A lower rate preserves more value inside Nova Labs or the Service Provider; a higher rate sends more value to HNT through DC burn.

Resolving the consolidation problem. Because Helium Mobile's economics sit outside HNT, the most discussed structural fix is some form of equity-to-token integration. In plain terms, that means bringing some or all of Nova Labs' Helium Mobile equity value into HNT, so the retail business and the protocol are economically tied to the same token. The clearest public articulation has come from Amir Haleem, Nova Labs CEO, who has stated he is "spending 99% of [his] time" working through how to merge the company's equity and token structures. In a Discord exchange (June 2025), Haleem acknowledged the central tension explicitly:

"You'd have to create more HNT, which is certainly the most contentious part of this conversation."

— Amir Haleem, Helium Discord, June 2025

The mechanism, structure, and timing remain open. Possibilities discussed across the community range from a structured equity-conversion at a defined dilution ratio (Blockworks Research reports an indicative 5–50% range under consideration internally), to converting Nova Labs into a nonprofit channeling all revenues into the HNT economy, to a more incremental approach via stablecoin-denominated infrastructure payments and gradual on-chain revenue routing. No formal governance proposal has been advanced.

Our Valuation Framework: Sum-of-the-Parts

Given the two structurally distinct entities and the open question of how — and whether — they will eventually be combined, we model HNT under a sum-of-the-parts (SOTP) approach. The framework consists of three building blocks:

This is a modeling choice, not a forecast. The eventual outcome may take a different form, occur on a different timeline, involve a different mechanism (a nonprofit conversion, a buyback structure, gradual on-chain routing), or not occur at all. The approach makes the embedded option visible and quantifiable: if integration happens at roughly this magnitude, what is HNT worth, and what does it imply about today's price?

The 30% issuance assumption sits within the 5–50% range indicated by Blockworks Research. We choose this level because it balances two constraints: enough value transfer for HNT to capture meaningful exposure to the combined business, and enough consideration for Nova Labs equity holders for a governance proposal to be realistic.

Nova Labs sits on both sides of this structure. It operates Helium Mobile, has influence in Network governance through its founding role, and holds an HNT-denominated treasury. Its incentives are partly aligned with HNT — Amir Haleem has publicly stated that Nova Labs has refrained from token sales — but the separation between Nova Labs equity and HNT can still create tension. The clearest pressure point is pricing: how much should Helium Mobile and other Service Providers pay the Network per GB? A lower rate preserves more value inside Nova Labs or the Service Provider; a higher rate sends more value to HNT through DC burn.

Resolving the consolidation problem. Because Helium Mobile's economics sit outside HNT, the most discussed structural fix is some form of equity-to-token integration. In plain terms, that means bringing some or all of Nova Labs' Helium Mobile equity value into HNT, so the retail business and the protocol are economically tied to the same token. The clearest public articulation has come from Amir Haleem, Nova Labs CEO, who has stated he is "spending 99% of [his] time" working through how to merge the company's equity and token structures. In a Discord exchange (June 2025), Haleem acknowledged the central tension explicitly:

"You'd have to create more HNT, which is certainly the most contentious part of this conversation."

— Amir Haleem, Helium Discord, June 2025

The mechanism, structure, and timing remain open. Possibilities discussed across the community range from a structured equity-conversion at a defined dilution ratio (Blockworks Research reports an indicative 5–50% range under consideration internally), to converting Nova Labs into a nonprofit channeling all revenues into the HNT economy, to a more incremental approach via stablecoin-denominated infrastructure payments and gradual on-chain revenue routing. No formal governance proposal has been advanced.

Our Valuation Framework: Sum-of-the-Parts

Given the two structurally distinct entities and the open question of how — and whether — they will eventually be combined, we model HNT under a sum-of-the-parts (SOTP) approach. The framework consists of three building blocks:

- Helium Network (standalone). Valued on the basis of DC burn from carrier offload and protocol-level economics, with value flowing entirely through HNT. This component captures the deflationary mechanics of the wholesale offload business and is independent of any equity-side decisions.

- Helium Mobile (standalone). Valued as an MVNO business, based on subscriber count, blended ARPU, gross margin assumptions, and a relevant comp-set multiple. Today, this value sits with Nova Labs equity holders rather than HNT holders.

- Integration assumption. We model equity-to-token integration as new HNT issuance equal to 30% of the pre-integration supply base. The issuance represents the consideration paid to bridge Nova Labs' Helium Mobile equity value into HNT-denominated terms. Under this assumption, Helium Mobile value is brought into the HNT valuation, and the combined SOTP value is shared by existing and newly issued HNT holders.

This is a modeling choice, not a forecast. The eventual outcome may take a different form, occur on a different timeline, involve a different mechanism (a nonprofit conversion, a buyback structure, gradual on-chain routing), or not occur at all. The approach makes the embedded option visible and quantifiable: if integration happens at roughly this magnitude, what is HNT worth, and what does it imply about today's price?

The 30% issuance assumption sits within the 5–50% range indicated by Blockworks Research. We choose this level because it balances two constraints: enough value transfer for HNT to capture meaningful exposure to the combined business, and enough consideration for Nova Labs equity holders for a governance proposal to be realistic.

Section 3. Tokenomics

HNT and Data Credits

Helium operates a two-token economic model that mechanically links network usage to supply contraction:

The two are connected by a one-way burn: network usage is paid in DC, and DC are created by burning HNT. Because DC carry a fixed USD price while HNT trades freely, every dollar of network usage translates into a deterministic amount of HNT burn at the prevailing market price. There is no buyback decision, treasury deployment, or governance step required. The supply effect is automatic and immediate.

Helium operates a two-token economic model that mechanically links network usage to supply contraction:

- HNT is the protocol's native token — the unit of reward for hotspot operators, the burn asset for network access, and the basis for governance.

- Data Credits (DC) are non-tradable settlement units pegged at $0.00001 each. DC cannot be transferred between wallets and exist solely to pay for bandwidth at a reference price of $0.50/GB.

The two are connected by a one-way burn: network usage is paid in DC, and DC are created by burning HNT. Because DC carry a fixed USD price while HNT trades freely, every dollar of network usage translates into a deterministic amount of HNT burn at the prevailing market price. There is no buyback decision, treasury deployment, or governance step required. The supply effect is automatic and immediate.

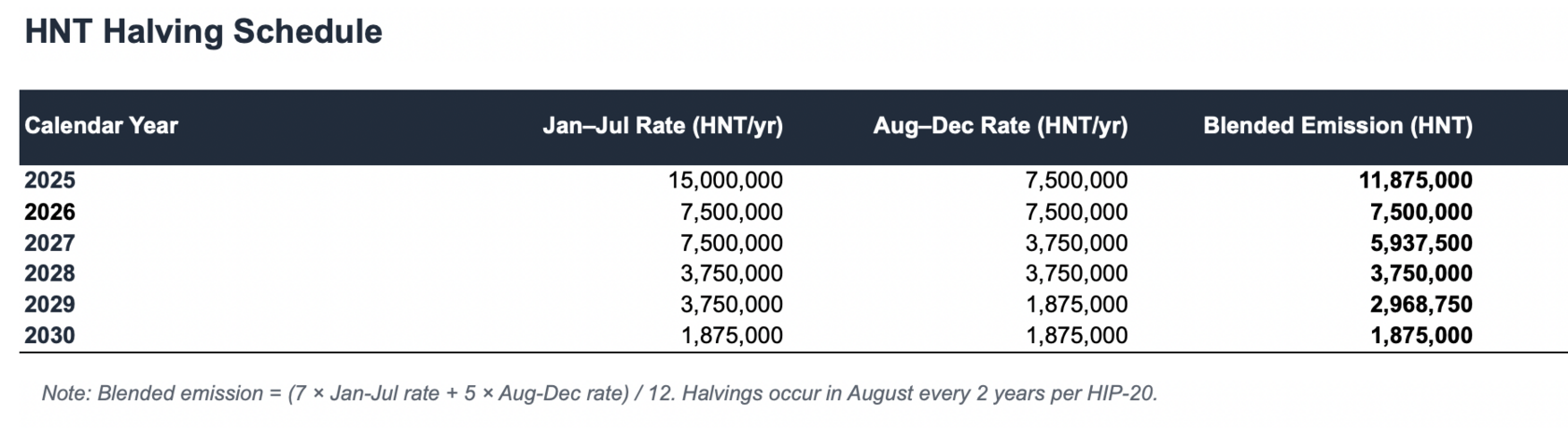

Emissions, Halvings, and Hard Cap

HNT issuance follows a Bitcoin-style halving schedule, with emissions cut by 50% every two years. The first halving in August 2025 reduced annual emissions from 15M to 7.5M tokens; the next, in August 2027, will reduce them to 3.75M. Under current protocol rules, HNT supply is capped at approximately 223M tokens, with ordinary rewards following the scheduled halving path.

HNT issuance follows a Bitcoin-style halving schedule, with emissions cut by 50% every two years. The first halving in August 2025 reduced annual emissions from 15M to 7.5M tokens; the next, in August 2027, will reduce them to 3.75M. Under current protocol rules, HNT supply is capped at approximately 223M tokens, with ordinary rewards following the scheduled halving path.

The protocol also embeds a Net Emissions mechanism that recycles a portion of burned HNT back into operator rewards. The mechanism works at the epoch level: the protocol tracks how much HNT was burned for Data Credits in a given epoch (~daily) and re-mints up to a cap of approximately 1,644 HNT per day (~600K annually). Burned HNT up to the cap can be re-minted as Net Emissions. Any burn above the cap is not re-minted, so it permanently reduces supply while preserving the 223M ceiling. If there is no burn, nothing is re-minted.

This mechanism keeps operators economically incentivized over the long run, even after scheduled halvings drive new issuance toward zero (projected ~2070). As long as the network is being used, operators receive recycled rewards; when burn exceeds emissions — as it did in Q1 2026 — the excess burn permanently reduces supply. This combination of a hard cap, a halving schedule, and a recycled-burn floor makes HNT structurally deflationary in periods of high network usage while preserving operational viability.

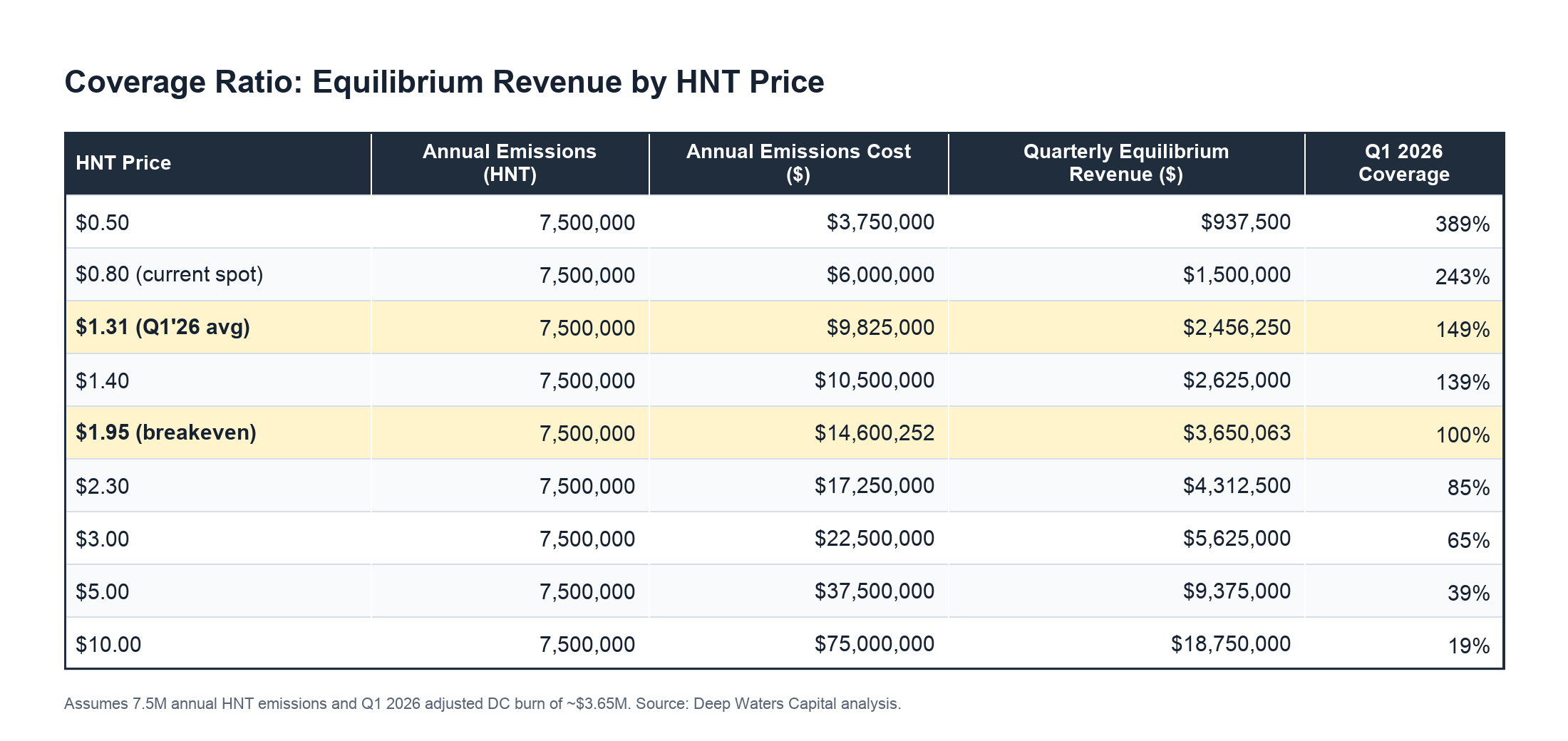

The Coverage Ratio Framework

Protocol-level burn coverage reduces to a single ratio: DC burn divided by HNT emissions, measured in USD. Above 100%, the network is structurally deflationary; below 100%, it dilutes token holders to subsidize coverage. The equilibrium revenue level — what the network must generate for coverage to equal 100% — is a direct function of HNT price. At post-halving emissions of 7.5M tokens annually:

This mechanism keeps operators economically incentivized over the long run, even after scheduled halvings drive new issuance toward zero (projected ~2070). As long as the network is being used, operators receive recycled rewards; when burn exceeds emissions — as it did in Q1 2026 — the excess burn permanently reduces supply. This combination of a hard cap, a halving schedule, and a recycled-burn floor makes HNT structurally deflationary in periods of high network usage while preserving operational viability.

The Coverage Ratio Framework

Protocol-level burn coverage reduces to a single ratio: DC burn divided by HNT emissions, measured in USD. Above 100%, the network is structurally deflationary; below 100%, it dilutes token holders to subsidize coverage. The equilibrium revenue level — what the network must generate for coverage to equal 100% — is a direct function of HNT price. At post-halving emissions of 7.5M tokens annually:

Equilibrium revenue = HNT Price x Annual Emissions (7.5M HNT post-Aug 2025 halving). Above 100% Coverage Ratio = network structurally deflationary; below 100% = dilutes token holders. Q1 2026 Coverage column = Q1 2026 actual adjusted DC burn (~$3.65M quarterly, excluding one-off discretionary burn) ÷ Quarterly Equilibrium Revenue at given HNT price. Two anchors highlighted: $1.31 (Q1 2026 average HNT price — matches the historical 149% Coverage) and $1.95 (forward breakeven at current ~$3.65M quarterly revenue).

The deflation claim is therefore price-sensitive, not unconditional. Q1 2026 burn covered emissions at the observed HNT price; if HNT rises while DC burn stays flat, the dollar value of emissions rises and Coverage Ratio falls. The investment case requires continued DC burn growth and scheduled halvings to absorb a higher HNT price over time.

The deflation claim is therefore price-sensitive, not unconditional. Q1 2026 burn covered emissions at the observed HNT price; if HNT rises while DC burn stays flat, the dollar value of emissions rises and Coverage Ratio falls. The investment case requires continued DC burn growth and scheduled halvings to absorb a higher HNT price over time.

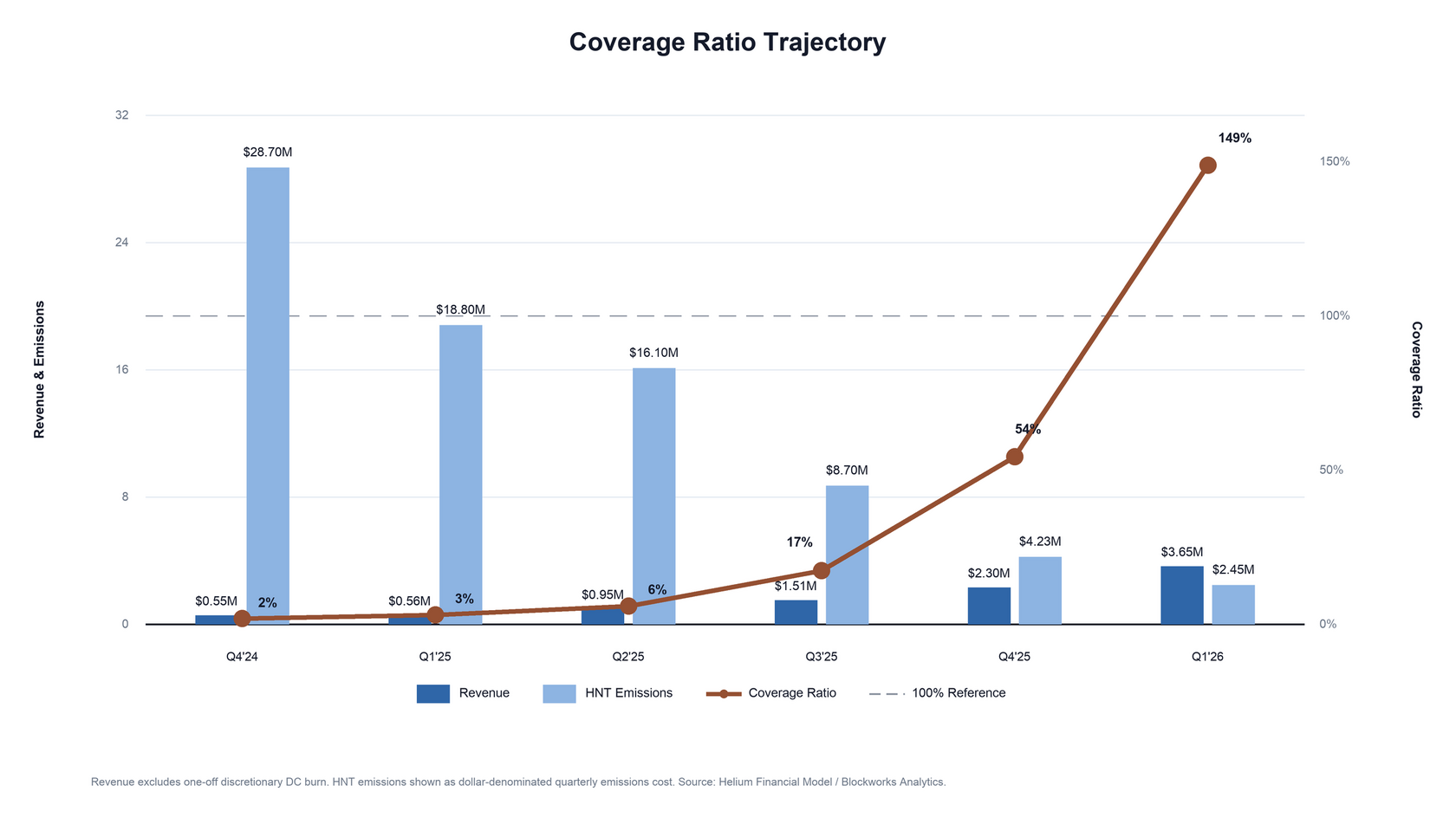

The trajectory of actual coverage has been sharp. Across the past six quarters, two forces converged: revenue grew as carrier offload partnerships scaled, while dollar-denominated emissions contracted following the August 2025 halving and HNT price decline. The result is a Coverage Ratio that rose from low single digits in 2024 to net-deflation by Q1 2026:

Coverage Ratio Trajectory: Carrier-Driven Revenue vs HNT Emissions (Q4 2024 – Q1 2026). Revenue = Total revenue excluding one-off DC burn. HNT Emissions = quarterly HNT issuance x average HNT price.

Q1 2026 marked the first quarter where carrier offload demand alone exceeded HNT emissions in dollar terms. This is the most important fundamental shift in Helium's history: the network is no longer subsidizing coverage with token issuance — it is monetizing it. This framework — coverage ratio, equilibrium revenue, and sensitivity to HNT price — is the core lens we apply in the financial model and valuation.

Q1 2026 marked the first quarter where carrier offload demand alone exceeded HNT emissions in dollar terms. This is the most important fundamental shift in Helium's history: the network is no longer subsidizing coverage with token issuance — it is monetizing it. This framework — coverage ratio, equilibrium revenue, and sensitivity to HNT price — is the core lens we apply in the financial model and valuation.

Section 4. 2025 in Review and Q1 2026 Update

2025 was the year Helium converted a multi-year strategic pivot — from CBRS cellular to Wi-Fi offload — into measurable operating leverage. Network usage scaled, governance consolidated, regulatory overhangs cleared, and the protocol crossed into structural deflation by Q1 2026. The token, however, traded in the opposite direction.

Operational Milestones

Major governance and product events from Q1 2025 through Q1 2026:

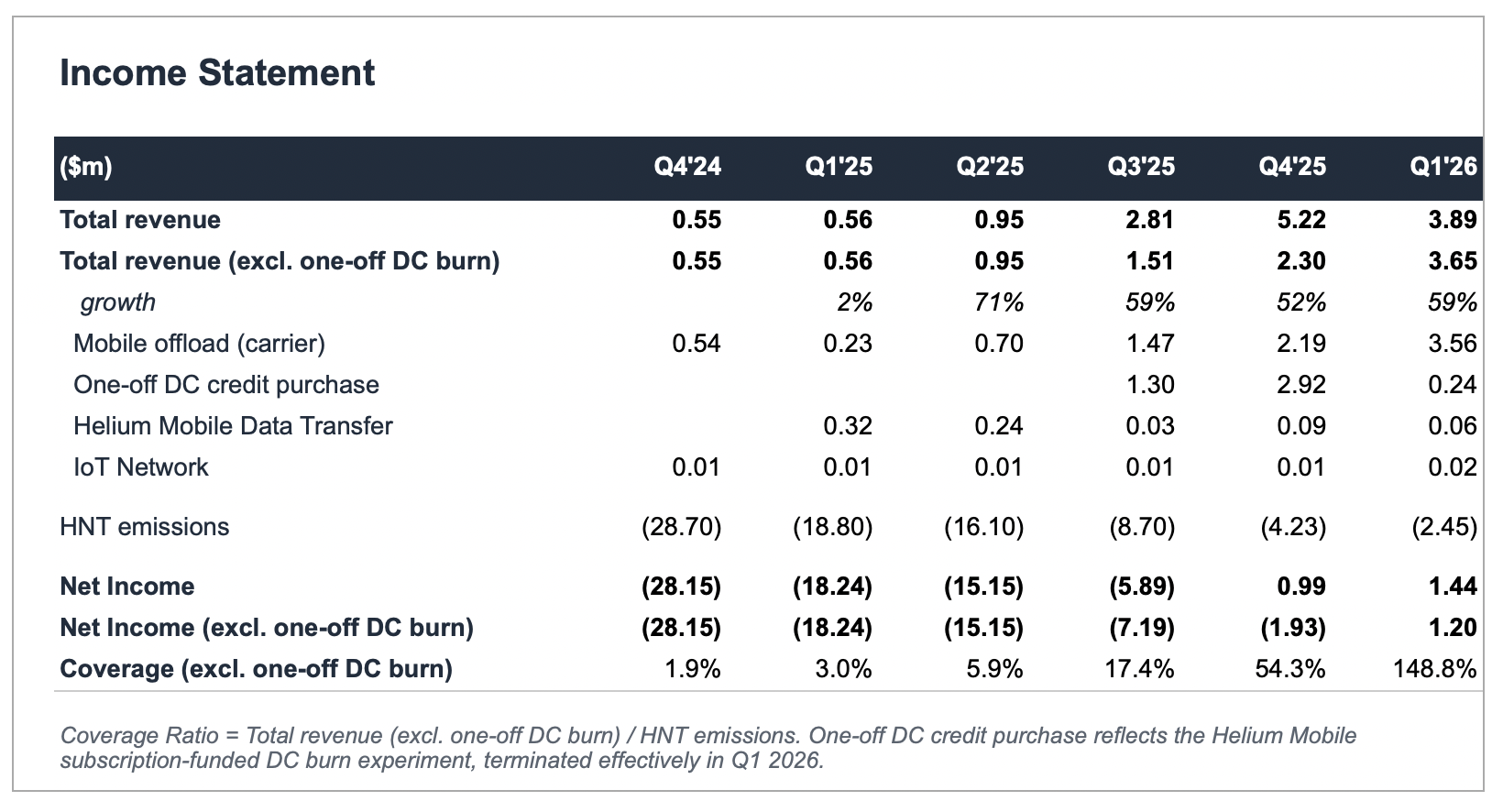

Financial Trajectory

The income statement progression over six quarters reflects the strategic shift toward Wi-Fi offload:

Operational Milestones

Major governance and product events from Q1 2025 through Q1 2026:

- Q1 2025. HIP 138 ("Return to HNT") consolidated the IOT and MOBILE subDAO tokens back into a single HNT, simplifying liquidity and governance. HIP 139 phased out CBRS small-cell deployments in favor of Wi-Fi offload, dramatically reducing operator capex requirements. HIP 141 implemented single-token governance.

- April 2025. SEC dismissed its January 2025 complaint against Nova Labs with a $200K settlement, removing the largest regulatory overhang. AT&T carrier offload partnership publicly announced.

- Q2 2025. HIP 142 onboarded Inversion Capital as a second authorized Service Provider focused on LATAM MVNO consolidation, passing with 99.68% approval from veHNT holders. Helium Plus launched, removing hardware requirements for operator participation.

- August 2025. First HNT halving — annual emissions cut from 15M to 7.5M tokens. Helium Mobile separately began an experimental program of discretionary DC burn, routing 100% of subscription revenue into open-market HNT purchases through Jupiter dollar-cost averaging.

- Q4 2025. HIP 148 reallocated mapping rewards to data transfer, further weighting emissions toward operators producing measurable throughput. Helium Mobile terminated the discretionary burn experiment in favor of organic monetization focus, leaving carrier offload as the protocol's recurring go-forward revenue baseline.

- Q1 2026. Adjusted DC burn reached ~$3.65M, excluding one-off discretionary burn, and exceeded HNT emissions for the first time on a recurring basis.

Financial Trajectory

The income statement progression over six quarters reflects the strategic shift toward Wi-Fi offload:

Three structural shifts stand out:

Token Performance and the Fundamental Disconnect

While operating fundamentals improved meaningfully through 2025, HNT moved in the opposite direction. The token traded near $4.00 entering 2025 and declined to roughly $1.22 at year-end — a ~70% drawdown — even as carrier offload revenue grew ~7x and coverage ratio went from low single digits to 54.3%. As of May 2026, HNT trades at approximately $0.80, extending the disconnect into a second period of fundamental improvement.

Three factors plausibly explain the divergence:

The setup is structurally asymmetric: the operating business is deflationary and accelerating, while the token trades at multiples that imply survival risk. That risk is no longer supported by the carrier offload trajectory or post-halving economics.

See Part 2 for $HNT valuation and forecasts.

- Revenue is growing organically. Stripping out the discontinued discretionary burn, Q1 2026 adjusted DC burn (~$3.65M) continued a multi-quarter sequence of 50%+ QoQ growth in recurring usage. The Q1 2026 print of ~$3.9M total DC burn is a cleaner baseline than Q4's $5.2M optical peak because the Q4 number included $2.92M of discretionary subscription-funded burn.

- Emissions are collapsing. Two effects combined: the August halving cut token emissions by 50%, and HNT price decline reduced the USD value of remaining emissions further. The result was a 91% reduction in dollar-denominated emissions from Q4 2024 ($28.7M) to Q1 2026 ($2.45M).

- Net income flipped positive. Q4 2025 produced the first positive headline Net Income, but the quarter remained negative on a recurring basis after excluding the $2.92M one-off discretionary DC burn from the now-terminated Helium Mobile subscription program. Q1 2026 was different: the protocol was positive even after excluding the residual $0.24M one-off, producing $1.4M headline Net Income and $1.2M adjusted Net Income. Operating cash flow followed the same trajectory.

Token Performance and the Fundamental Disconnect

While operating fundamentals improved meaningfully through 2025, HNT moved in the opposite direction. The token traded near $4.00 entering 2025 and declined to roughly $1.22 at year-end — a ~70% drawdown — even as carrier offload revenue grew ~7x and coverage ratio went from low single digits to 54.3%. As of May 2026, HNT trades at approximately $0.80, extending the disconnect into a second period of fundamental improvement.

Three factors plausibly explain the divergence:

- Forced selling from a large holder. Amir Haleem has publicly referenced "forced selling from a large token holder" in mid-2025 commentary. The shape of the drawdown — sustained downward pressure across multiple quarters of accelerating fundamentals — is more consistent with technical supply pressure than with deteriorating economics.

- No active buyback mechanism. Unlike GEODNET or Render (where 80% of revenue is deployed as open-market buybacks), Helium's deflationary mechanism operates through DC burn — supply contracts via destruction of HNT used to mint Data Credits, with no visible spot demand. The supply contraction is real but mechanically invisible to traders watching order books.

- DePIN sector rotation. The broader DePIN drawdown documented in Section 1 (94-99% from ATH for the 2018-2022 cohort) reflects sector-level risk-off rather than asset-specific concerns. Helium is being repriced alongside networks that lack its operating profile.

The setup is structurally asymmetric: the operating business is deflationary and accelerating, while the token trades at multiples that imply survival risk. That risk is no longer supported by the carrier offload trajectory or post-halving economics.

See Part 2 for $HNT valuation and forecasts.