This article assumes a basic understanding of MetaDAO's design, the concept of futarchy, and Internet Capital Markets.

We're not going to cover MetaDAO's overall design, explain the way it works, or provide an overview of the projects launched on it so far. Instead, we're going to highlight some market considerations that we think are under-discussed with respect to MetaDAO in particular and launchpads in general, as well as provide a valuation framework for everyone to play around with to test different assumptions.

If you have questions or feedback, feel free to reach out directly to the authors—we welcome the conversation.

Mark Leontev, Katarina Keller

We're not going to cover MetaDAO's overall design, explain the way it works, or provide an overview of the projects launched on it so far. Instead, we're going to highlight some market considerations that we think are under-discussed with respect to MetaDAO in particular and launchpads in general, as well as provide a valuation framework for everyone to play around with to test different assumptions.

If you have questions or feedback, feel free to reach out directly to the authors—we welcome the conversation.

Mark Leontev, Katarina Keller

It is 2025 and there's still no real crypto launchpad

Launchpads today are web2 funnels with token tickers bolted on. The only extent at which they actually use crypto rails is the mere fact of crypto tokens they offer for the clientele. Their products are not in any way impacted by anything cryptography and blockchains have to offer. They restrict access by jurisdiction, centralize discretion over unlock schedules and allocations, and offer investors little protection. Right now, they are pretty much what their name suggests: pads from which an asset bounces off exactly once, with functionality structured as part of the traditional financial stack.

The traditional financial stack -- with its KYC gauntlets, friction, curation, and geo‑blocking -- was designed very long ago for a very different world -- the world of chronic information asymmetry. Think 19th‑century railway manias and railroad stock/bond frauds -- unauthorised share certificates, watered stock, and speculative schemes retail investors had no real way to diligence. That’s what led us to the world of institutional control, curation, authorisations, underwritings, KYCs and AMLs.

That’s not the world we live in now. The price of knowledge is asymptotically zero: anyone with an internet connection and AI can be a reasonably informed investor. The bottleneck is no longer access to information; it’s attention and credible execution. Yet most crypto launchpads are still architected for the old regime.

MetaDAO is the first launchpad that builds a first principles correct substrate for the 21st‑century internet-native issuance market and the coming agentic economy. MetaDAO is the first ICO product in the space that delivers a suite of services that aim to utilize qualities at which blockchain rails are unequivocally superior: spanning tokenholder rights, value accrual, capital control, the launch itself, initial price discovery, and ongoing governance, all packaged together in what they call “ownership coins.”

The traditional financial stack -- with its KYC gauntlets, friction, curation, and geo‑blocking -- was designed very long ago for a very different world -- the world of chronic information asymmetry. Think 19th‑century railway manias and railroad stock/bond frauds -- unauthorised share certificates, watered stock, and speculative schemes retail investors had no real way to diligence. That’s what led us to the world of institutional control, curation, authorisations, underwritings, KYCs and AMLs.

That’s not the world we live in now. The price of knowledge is asymptotically zero: anyone with an internet connection and AI can be a reasonably informed investor. The bottleneck is no longer access to information; it’s attention and credible execution. Yet most crypto launchpads are still architected for the old regime.

MetaDAO is the first launchpad that builds a first principles correct substrate for the 21st‑century internet-native issuance market and the coming agentic economy. MetaDAO is the first ICO product in the space that delivers a suite of services that aim to utilize qualities at which blockchain rails are unequivocally superior: spanning tokenholder rights, value accrual, capital control, the launch itself, initial price discovery, and ongoing governance, all packaged together in what they call “ownership coins.”

Asset Issuance Market Considerations:

- Markets are moving onchain. This isn’t just our conjecture; it’s now explicitly acknowledged in SEC statements. Onchain rails are inherently global, permissionless, 24/7, and composable. Any platform that plugs into this stack can naturally extend into adjacent layers -- issuance, trading, settlement, governance --and capture more of the value chain than a single legacy venue. That directly expands its TAM, especially on the issuance side.

- Current launchpads are not positioned optimally for this. Most “launchpads” only touch a single point in that stack -- the primary sale -- and, by design, only capture that one market. A platform that spans more of the lifecycle -- legal incorporation and structuring, primary issuance, price discovery, secondary liquidity, and governance -- is literally plugged into more markets. It captures a bigger share of the Internet Capital Markets TAM because it intermediates more of the flow, more often, for longer.

- Launchpads are not a winner‑take‑most market. In many DeFi niches like perps, the products are almost perfectly overlapping: a perp is a perp. Feature sets blur, liquidity is mercenary, and competition is close to 100% overlap. Launchpads are the opposite. Startups, their founders, legal setups, traction, and risk profiles are not fungible; they are effectively “life itself” expressed as projects. A late‑stage, high‑profile team with revenue, a clean cap table, and regulatory sensitivity has very different needs from a weird, early, internet‑native experiment that wants to align deeply with tokenholders seeking for the durability of distribution rather than its sheer size. That’s why it’s easy to imagine highly curated, web2‑style launchpads thriving alongside something like MetaDAO that dominates permissionless launches for specific cohorts: earlier‑stage teams, more experimental ideas, projects that explicitly want ownership coins and stronger token alignment. A HumidiFi‑type project choosing a Jupiter DTF launchpad makes sense in that frame: some ideas don’t need to become ownership coins, others absolutely do. Distribution will fragment across these surfaces because the underlying demand is segmented by founder type, stage, risk, and ideology. The moat isn’t being “the one launchpad”; it’s being the right coordination mechanism for a specific slice of that diversity.

- Attention‑native issuance and trading are exploding. Throughout 2024-2025, issuance has found PMF in new modalities: fair launches, auctions, bonding curves, bots and feeds as distribution. “Memecoin mania” of recent months is often misread as financial nihilism; we read it as proof of a huge latent demand “to be truly early”, an option that mostly disappeared after the 2017 ICO era. Capital formation, distribution, price discovery, and community formation are the same loop, not separate departments. It makes sense to approach them as a whole via a bundled service that secures upside and delivers investor protection. Such cohort is bound to stand out as a whole new category of projects, inevitably catching attention.

- Futarchy as a governance mechanism remains under-explored and under-appreciated. If you believe the 21st‑century economy will be at all dominated by AI agents that act directly in markets rather than in comment sections, you’re implicitly betting on governance that machines can parse and enforce. Because they won't waste compute to argue in forums, it's inefficient. They’ll hit markets -- as it is a much more efficient way for a machine to express an opinion. Futarchy turns proposals into conditional orderflow: “I’m willing to bid X for asset Y if it implements Z.” Agents will express beliefs as prices on these if‑then markets, and contracts will wire execution -- unlocks, parameter changes, treasury moves -- directly to those outcomes. MetaDAO bakes this in so that whoever prices the future best doesn’t just win trades; they steer the roadmap.

- Under‑read design → self‑selecting users → future repricing. MetaDAO already has a bunch of intricacies and beautiful mechanics most of the first‑wave hype crowd hasn’t actually clocked -- because they don’t read. You still see people dropping into chat making lazy comparisons to old launchpads and their blow‑ups, as if this were just “another IDO pad.” It isn’t. There’s no big day‑one founder bag, no fixed pre‑grant; founder upside is earned via KPI‑gated mints/unlocks: hit X by time T → get Y. That makes founders behave less like lottery winners and more like a public‑company leadership team (CEO/CFO/IR) whose comp is tied to the performance and communication that drive long‑term valuation: if the business doesn’t deliver, the upside simply doesn’t materialize. On the other side, MetaDAO is the single worst‑positioned launchpad for people who won’t read: the futarchy + conditional markets learning curve is steep, so non‑readers show up, get confused, and churn out -- which effectively serves as an investor‑quality filter. The quality founders like quality investors. As the rules and incentives become understood better by more people and the information asymmetry closes, the comparison set and $META pricing consensus both change. And we are not at that stage yet.

$META Valuation Considerations:

Not all of the factors listed above can be conveniently expressed as numeric assumptions when performing an asset valuation. It's important to keep in mind that the valuation provided here is backward-looking in the sense that it treats MetaDAO as an established revenue-generating business operating across a fixed set of revenue streams. However, this may not hold true in the near future, as the startup is young and open to pivots.

It's also worth remembering that we typically don't conduct valuation exercises simply to pinpoint a target price for an "exit point" or similar milestone. Instead, these serve as a framework for thought experiments -- particularly in our case, where we're exploring what assumptions would be sufficient to conservatively project 10x growth over the next five years. This approach highlights which catalysts are omitted from our hypotheses, realistically revealing the degree of conservatism embedded in that 10x growth expectation for the project. As you'll see, the assumptions required for 10x growth in MetaDAO are arguably modest and almost entirely devoid of the forward-looking theses outlined in the section above.

We opened the file for everyone to make a copy and play around with their own assumptions. Enjoy.

It's also worth remembering that we typically don't conduct valuation exercises simply to pinpoint a target price for an "exit point" or similar milestone. Instead, these serve as a framework for thought experiments -- particularly in our case, where we're exploring what assumptions would be sufficient to conservatively project 10x growth over the next five years. This approach highlights which catalysts are omitted from our hypotheses, realistically revealing the degree of conservatism embedded in that 10x growth expectation for the project. As you'll see, the assumptions required for 10x growth in MetaDAO are arguably modest and almost entirely devoid of the forward-looking theses outlined in the section above.

We opened the file for everyone to make a copy and play around with their own assumptions. Enjoy.

Valuation Overview:

We built our MetaDAO valuation model following the launch of its crowdsale platform for “unruggable” ICOs — a new financial primitive for on-chain capital formation that enables high-quality founders to raise capital while sending a credible, on-chain signal about enforceable tokenholder rights.

By design, MetaDAO allows founders to differentiate themselves from “lemons” in an asymmetric “peaches-and-lemons” market for early-stage token offerings (see concept here). This structure ensures that investor capital cannot be “rugged” or misused, and that project execution remains transparently tied to on-chain governance outcomes. Each project launching through MetaDAO transfers its intellectual property rights and governance authority to a dedicated legal entity — effectively creating an enforceable legal wrapper around the token. The funds raised during the ICO are locked in a treasury contract and can only be accessed according to a predefined monthly budget, with any additional spending requiring approval through the Decision Market mechanism.

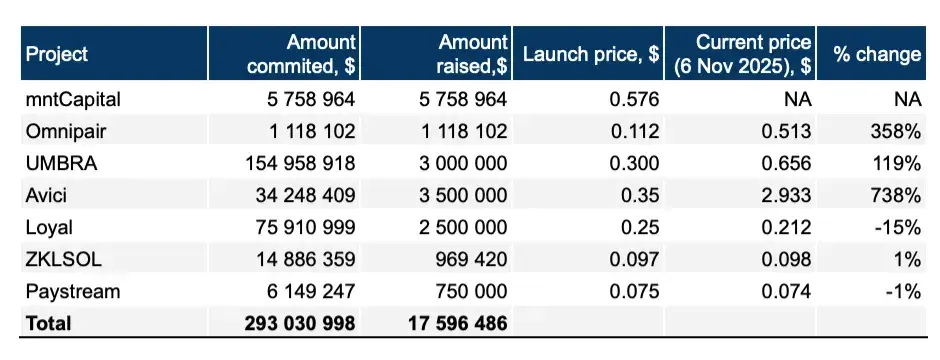

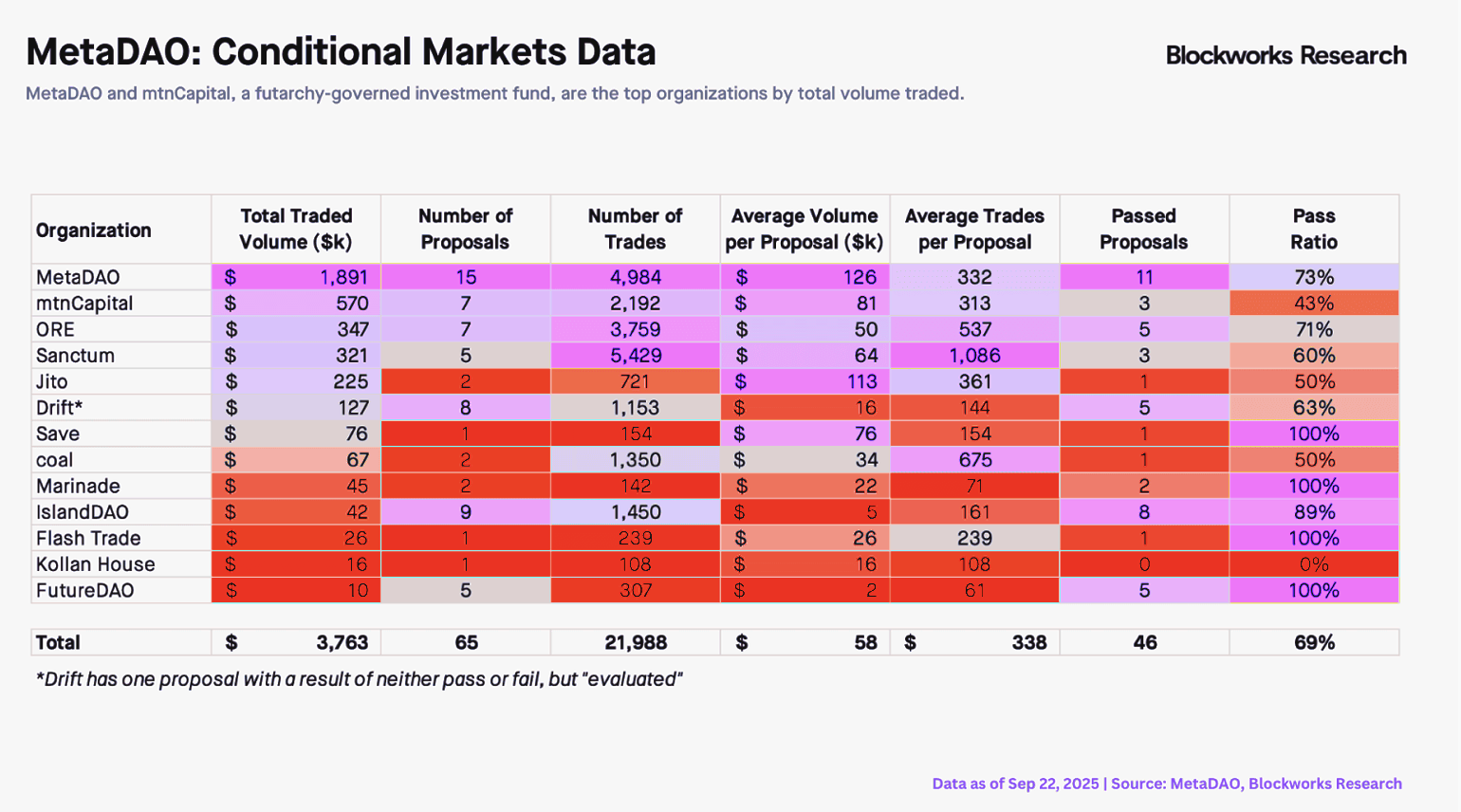

As of 6 Nov 2025, a total of seven ICOs have been launched on the platform, collectively raising $17.6m, with over $290m in total commitments. Although MetaDAO remains in its early stage and the dataset is still limited, early results already provide quantifiable signals that enable us to begin forward-looking revenue modelling.

By design, MetaDAO allows founders to differentiate themselves from “lemons” in an asymmetric “peaches-and-lemons” market for early-stage token offerings (see concept here). This structure ensures that investor capital cannot be “rugged” or misused, and that project execution remains transparently tied to on-chain governance outcomes. Each project launching through MetaDAO transfers its intellectual property rights and governance authority to a dedicated legal entity — effectively creating an enforceable legal wrapper around the token. The funds raised during the ICO are locked in a treasury contract and can only be accessed according to a predefined monthly budget, with any additional spending requiring approval through the Decision Market mechanism.

As of 6 Nov 2025, a total of seven ICOs have been launched on the platform, collectively raising $17.6m, with over $290m in total commitments. Although MetaDAO remains in its early stage and the dataset is still limited, early results already provide quantifiable signals that enable us to begin forward-looking revenue modelling.

Our forecasts for MetaDAO revenues are built around the protocol’s two primary products:

- ICO Launchpad — where MetaDAO acts as the launch and liquidity venue for new tokens.

- Decision Markets — governance- and proposal-based prediction markets powered by futarchy mechanics.

Based on historical market data for 9M25 and early on-chain volumes from MetaDAO ICOs and decision markets, we forecast protocol revenues for 2026 (1-year forward) and 2030 (5-year forward). To estimate MetaDAO’s 2030 fully diluted valuation (FDV), we apply an FDV/Revenue multiple methodology, using a 20× FDV/Rev multiple in the base case (consistent with Blockworks’ analysis) and discounting back to 2025 at a 40% annual rate to account for execution and market risk.

The Launchpad business model is driven by trading volumes in MetaDAO’s liquidity pools — primarily the Futarchy AMM and Meteora liquidity pools — which are created for each token after launch. Per protocol mechanics, approximately 2.9 million tokens are paired with 20% of the funds raised (in USDC) and deposited into AMMs to provide initial liquidity. For example, for Avici’s ICO, 2 million tokens and 20% of funds raised were locked in the Futarchy AMM, while 900k tokens were deposited into a single-sided pool on Meteora.

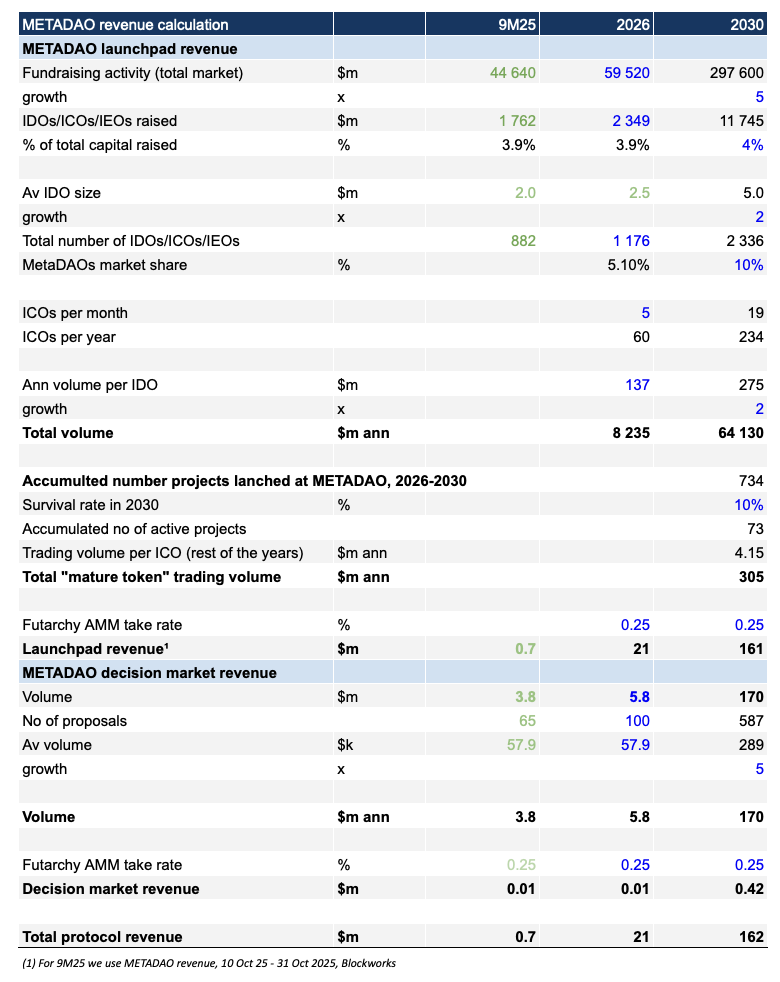

By 2030, we assume that the majority of MetaDAO’s revenues will come from ICO-related activity, while governance-linked volumes grow as more DAOs integrate futarchy mechanisms. In our model, launchpad revenue is calculated as: number of ICOs × average trading volume per ICO × take rate (25 bps).

For decision markets, we forecast the number of active markets in 2030 and apply an average trading volume per proposal × take rate (25 bps). Each new capital raise expands MetaDAO’s on-chain footprint and increases the number of DAOs governed via its futarchy-based system. According to the founding team, every project conducting an ICO through MetaDAO is expected to launch 2–4 decision markets per year to manage its governance decisions — not including additional markets created by external projects that did not conduct their ICOs through MetaDAO (such as ORE, Jito, Drift, or Marinade).

We believe the timing of this valuation update is particularly relevant. The early traction from MetaDAO’s first ICOs demonstrates that the protocol has moved beyond the experimental stage — showing clear market validation and investor demand. As a result, MetaDAO is evolving from a theoretical governance experiment into a functioning layer of Internet-native capital markets, with emerging revenues, identifiable growth drivers, and a scalable economic structure — making it possible to build a grounded valuation model - albeit with appropriate caution given the project’s early stage of development.

The Launchpad business model is driven by trading volumes in MetaDAO’s liquidity pools — primarily the Futarchy AMM and Meteora liquidity pools — which are created for each token after launch. Per protocol mechanics, approximately 2.9 million tokens are paired with 20% of the funds raised (in USDC) and deposited into AMMs to provide initial liquidity. For example, for Avici’s ICO, 2 million tokens and 20% of funds raised were locked in the Futarchy AMM, while 900k tokens were deposited into a single-sided pool on Meteora.

By 2030, we assume that the majority of MetaDAO’s revenues will come from ICO-related activity, while governance-linked volumes grow as more DAOs integrate futarchy mechanisms. In our model, launchpad revenue is calculated as: number of ICOs × average trading volume per ICO × take rate (25 bps).

For decision markets, we forecast the number of active markets in 2030 and apply an average trading volume per proposal × take rate (25 bps). Each new capital raise expands MetaDAO’s on-chain footprint and increases the number of DAOs governed via its futarchy-based system. According to the founding team, every project conducting an ICO through MetaDAO is expected to launch 2–4 decision markets per year to manage its governance decisions — not including additional markets created by external projects that did not conduct their ICOs through MetaDAO (such as ORE, Jito, Drift, or Marinade).

We believe the timing of this valuation update is particularly relevant. The early traction from MetaDAO’s first ICOs demonstrates that the protocol has moved beyond the experimental stage — showing clear market validation and investor demand. As a result, MetaDAO is evolving from a theoretical governance experiment into a functioning layer of Internet-native capital markets, with emerging revenues, identifiable growth drivers, and a scalable economic structure — making it possible to build a grounded valuation model - albeit with appropriate caution given the project’s early stage of development.

ICO Market Overview and Forecast

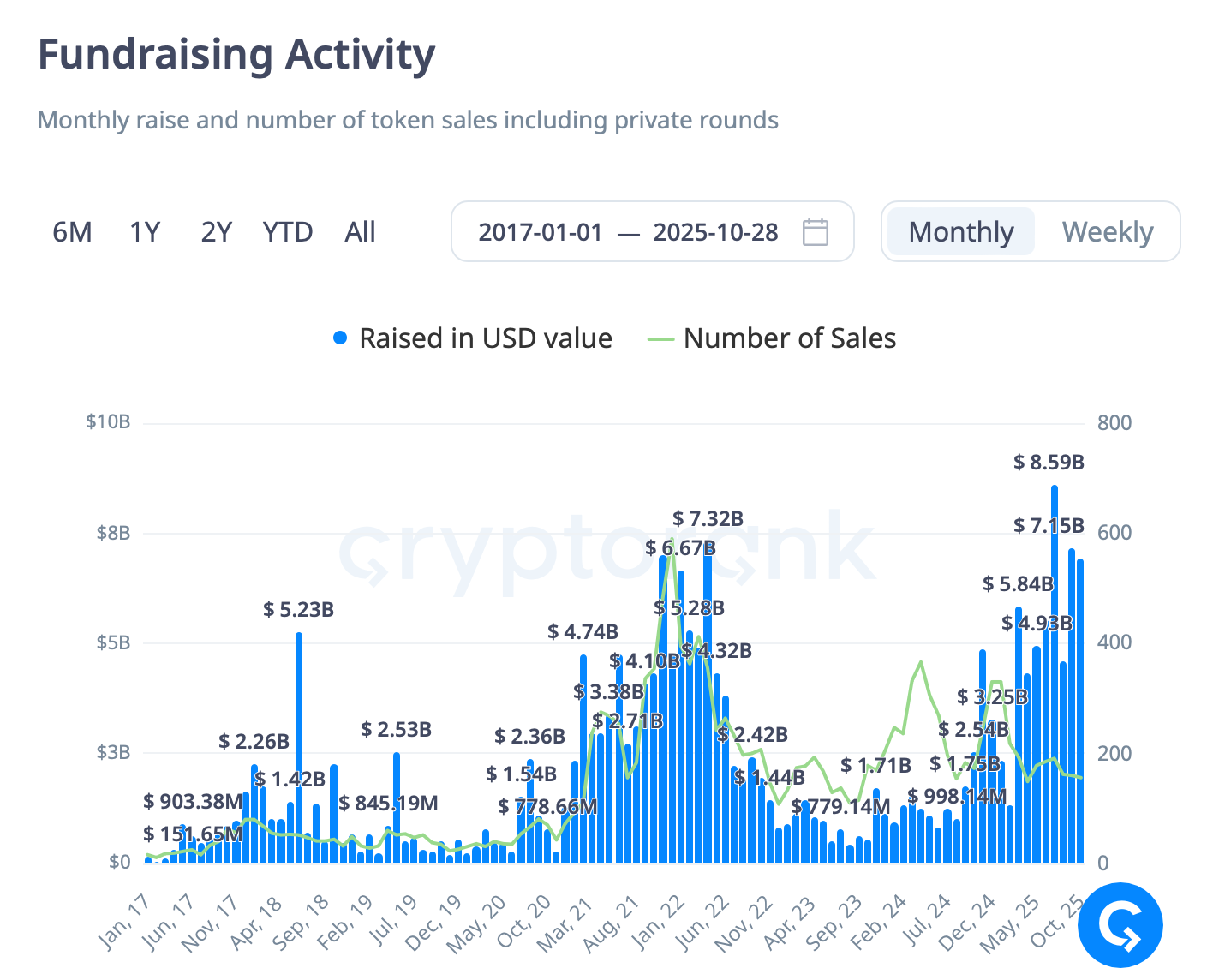

Over 9M25, around $45b has been raised across digital markets, with approximately $1.7b coming through ICO and IDO offerings. In total, 882 IDOs/ICOs/IEOs have taken place during this period, averaging around $2m per raise.

Looking ahead, we assume that the on-chain fundraising market — including ICOs, private placements, and other token-based financing mechanisms — will continue to expand in line with broader crypto adoption, reaching a total of $298 billion by 2030, representing roughly 5x growth over the next five years.

We consider this assumption consistent with the broader trajectory of the digital asset industry. According to a16z’s State of Crypto 2025 report, perpetual futures volumes, for example, are up nearly 8x year-on-year while tokenized real-world assets (RWAs) have reached around $30bn, up 4x over the past two years. The stablecoin market — the core liquidity backbone of on-chain activity — is projected by Citi to grow from $326bn today to $1.6–3.7t by 2030, implying 5–11x expansion in circulating supply. Taken together, these data points provide a robust macro foundation for our assumption of approximately 5x growth in on-chain fundraising activity by 2030.

We estimate that the share of capital raised via IDO/ICO mechanisms will remain broadly stable at around 4% of total digital-asset fundraising by 2030, in line with the historical six-year average. This translates into a total addressable market (TAM) of approximately $12bn in token launches by 2030, or roughly 2,300 ICOs per year, with an average raise size of $5m — 2x higher than today, driven primarily by inflation and rising institutional participation.

Within this market, we expect MetaDAO’s share to reach around 10%, implying 250 launches per year by 2030, or about 20 ICOs per month.

We acknowledge that forecasting the total number of ICOs and estimating market share remains a highly technical exercise. Nevertheless, we view it as a reasonable way to frame the potential market opportunity for MetaDAO within the broader on-chain fundraising landscape.

At the same time, MetaDAO has the potential to become a credible, high-quality launch venue for founders while expanding the pool of investors willing to participate in early-stage on-chain capital formation. Its architecture introduces a distinct structural advantage by embedding enforceable tokenholder rights directly at the protocol level — a mechanism that addresses the core investor risks historically associated with early-stage token offerings, including rug pulls, token-equity misalignment, and second-token dilution events.

As a result, we believe MetaDAO is well positioned to capture a meaningful share of the market and sustain a higher cadence of launches across market cycles — regardless of broader crypto conditions.

We consider this assumption consistent with the broader trajectory of the digital asset industry. According to a16z’s State of Crypto 2025 report, perpetual futures volumes, for example, are up nearly 8x year-on-year while tokenized real-world assets (RWAs) have reached around $30bn, up 4x over the past two years. The stablecoin market — the core liquidity backbone of on-chain activity — is projected by Citi to grow from $326bn today to $1.6–3.7t by 2030, implying 5–11x expansion in circulating supply. Taken together, these data points provide a robust macro foundation for our assumption of approximately 5x growth in on-chain fundraising activity by 2030.

We estimate that the share of capital raised via IDO/ICO mechanisms will remain broadly stable at around 4% of total digital-asset fundraising by 2030, in line with the historical six-year average. This translates into a total addressable market (TAM) of approximately $12bn in token launches by 2030, or roughly 2,300 ICOs per year, with an average raise size of $5m — 2x higher than today, driven primarily by inflation and rising institutional participation.

Within this market, we expect MetaDAO’s share to reach around 10%, implying 250 launches per year by 2030, or about 20 ICOs per month.

We acknowledge that forecasting the total number of ICOs and estimating market share remains a highly technical exercise. Nevertheless, we view it as a reasonable way to frame the potential market opportunity for MetaDAO within the broader on-chain fundraising landscape.

At the same time, MetaDAO has the potential to become a credible, high-quality launch venue for founders while expanding the pool of investors willing to participate in early-stage on-chain capital formation. Its architecture introduces a distinct structural advantage by embedding enforceable tokenholder rights directly at the protocol level — a mechanism that addresses the core investor risks historically associated with early-stage token offerings, including rug pulls, token-equity misalignment, and second-token dilution events.

As a result, we believe MetaDAO is well positioned to capture a meaningful share of the market and sustain a higher cadence of launches across market cycles — regardless of broader crypto conditions.

Volume Forecast per ICO

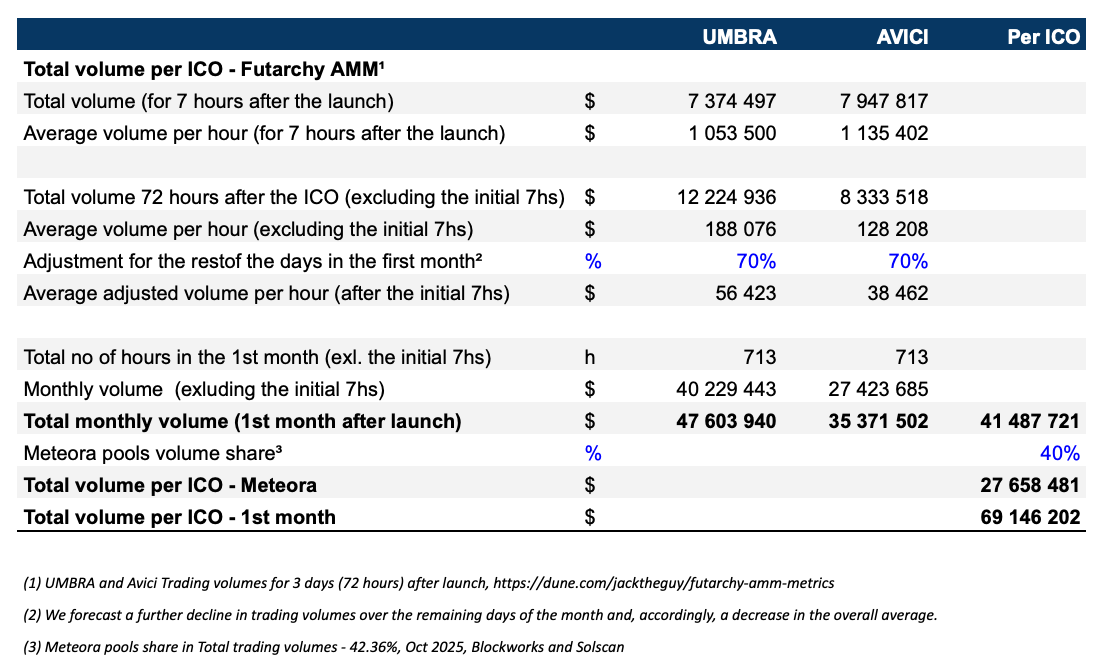

To estimate annualized trading volumes per ICO, we analyzed volumes data from MetaDAO’s early launches, including Umbra and Avici.

Trading activity consistently peaks within the first 7 hours following the ICO, before gradually stabilizing as liquidity providers rebalance and price discovery occurs.

Based on this behavior, we used data from the Futarchy AMM during the first 72 hours after each ICO, segmenting it into two phases — elevated trading during the first 7 hours and normalized activity over the subsequent 65 hours. We then calculated an average volume across both phases. For the remaining days of the month, we assumed that average daily volumes represent 30% of this initial post-launch average (70% adjustment in the table below), reflecting the typical decay in trading intensity observed across early launches. Under these assumptions, the average first-month trading volume via the Futarchy AMM amounts to approximately $41.5m.

To this figure, we added an estimated $27.7m in additional trading activity through liquidity pools at Meteora. Based on October 2025 data, the split between Futarchy AMM and Meteora volumes stood at roughly 58% / 42%. For simplicity, our model assumes a 60/40 distribution, resulting in a total projected first-month trading volume of $69.1m per ICO.

Trading activity consistently peaks within the first 7 hours following the ICO, before gradually stabilizing as liquidity providers rebalance and price discovery occurs.

Based on this behavior, we used data from the Futarchy AMM during the first 72 hours after each ICO, segmenting it into two phases — elevated trading during the first 7 hours and normalized activity over the subsequent 65 hours. We then calculated an average volume across both phases. For the remaining days of the month, we assumed that average daily volumes represent 30% of this initial post-launch average (70% adjustment in the table below), reflecting the typical decay in trading intensity observed across early launches. Under these assumptions, the average first-month trading volume via the Futarchy AMM amounts to approximately $41.5m.

To this figure, we added an estimated $27.7m in additional trading activity through liquidity pools at Meteora. Based on October 2025 data, the split between Futarchy AMM and Meteora volumes stood at roughly 58% / 42%. For simplicity, our model assumes a 60/40 distribution, resulting in a total projected first-month trading volume of $69.1m per ICO.

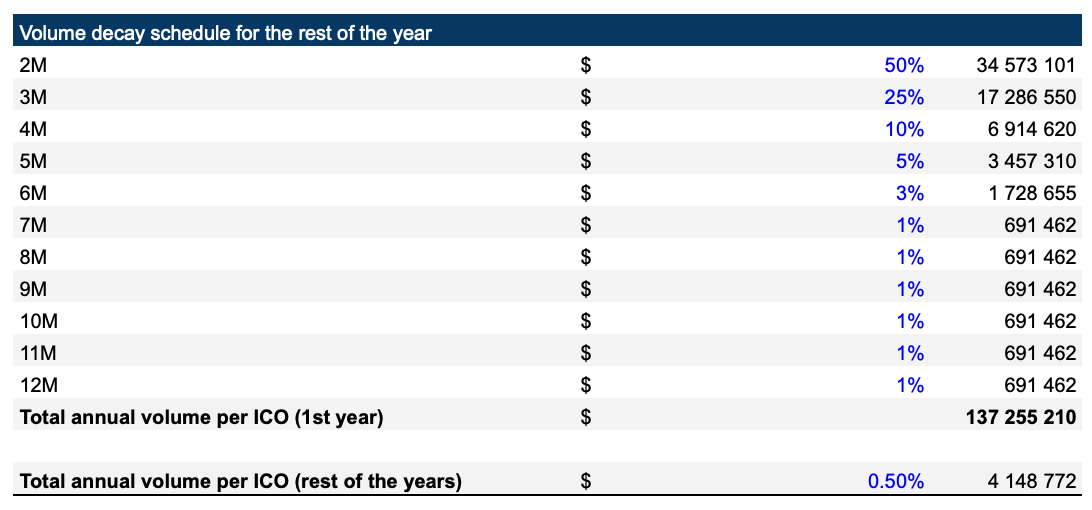

We apply the following simplified decay curve to approximate total first-year trading volume per token:

From these dynamics, we estimate an average first-year trading volume of $137m per token, nearly 2x higher than Blockworks’ assumption of $65m (median daily volume $180k based on Omnipair data). We expect this figure to double by 2030, driven by inflation, participation of larger LPs, integration of additional external liquidity pools, and additional CEX listings.

In our model, we also account for trading activity in subsequent years for projects that remain active. Assuming a linear growth trajectory, more than 700 ICOs are expected to be launched through the MetaDAO launchpad over the next five years, of which roughly 10% are likely to remain actively traded. Starting from the second year after launch, we estimate an average annual trading volume of $4.1m per token. According to our projections, by 2030 the cumulative trading volume of “mature” tokens (i.e., those beyond their initial post-ICO year) will reach approximately $305m, in addition to the trading volume generated by newly launched tokens described above.

Applying a 25 bps protocol take rate, we estimate $21 million in annualised revenue (1-year forward) and $161 million in 2030 under the base-case scenario.

In our model, we also account for trading activity in subsequent years for projects that remain active. Assuming a linear growth trajectory, more than 700 ICOs are expected to be launched through the MetaDAO launchpad over the next five years, of which roughly 10% are likely to remain actively traded. Starting from the second year after launch, we estimate an average annual trading volume of $4.1m per token. According to our projections, by 2030 the cumulative trading volume of “mature” tokens (i.e., those beyond their initial post-ICO year) will reach approximately $305m, in addition to the trading volume generated by newly launched tokens described above.

Applying a 25 bps protocol take rate, we estimate $21 million in annualised revenue (1-year forward) and $161 million in 2030 under the base-case scenario.

Decision Markets Forecast

In addition to revenues from token launches, MetaDAO also monetizes activity from decision markets — governance-linked prediction markets that allow tokenholders to trade outcomes of DAO proposals. Each organization integrated into MetaDAO can create a set of conditional markets, with all trading executed through the same Futarchy AMM infrastructure.

Since Q224, approximately $3.8m in cumulative trading volume has passed through MetaDAO’s decision markets across 65 proposals, with an average trading volume of $58k per proposal.

Since Q224, approximately $3.8m in cumulative trading volume has passed through MetaDAO’s decision markets across 65 proposals, with an average trading volume of $58k per proposal.

For our 2030 projections, we assume that the total number of proposals traded on MetaDAO’s decision markets will grow to approximately 590, up from the current 65. To estimate this figure, we assume that each of the 73 active projects launched through MetaDAO (10% of total projects launched for 5 years) will, by 2030, create on average four governance proposals per year (founder’s comment here, at 1:01:30 — “2–4 decision markets per project per year”). We then double this number to account for decision markets originating from partner projects that collaborate with MetaDAO but did not launch their token through the platform. This results in a total of roughly 587 decision markets projected for 2030.

We further assume an average trading volume of $289k per proposal, representing a 5x increase from current levels — driven by inflation, the inflow of new participants, and broader adoption of futarchy-based governance mechanisms across both on-chain and off-chain organisations.

Under these assumptions, the aggregate trading volume processed through decision markets in 2030 would reach approximately $170m. Applying a 25 bps (0.25%) take rate, this corresponds to an estimated protocol revenue of $0.42m generated from decision markets by 2030 — a relatively modest contribution from today, but one expected to grow meaningfully over time as more governance experiments are launched and adoption within the MetaDAO ecosystem deepens.

We further assume an average trading volume of $289k per proposal, representing a 5x increase from current levels — driven by inflation, the inflow of new participants, and broader adoption of futarchy-based governance mechanisms across both on-chain and off-chain organisations.

Under these assumptions, the aggregate trading volume processed through decision markets in 2030 would reach approximately $170m. Applying a 25 bps (0.25%) take rate, this corresponds to an estimated protocol revenue of $0.42m generated from decision markets by 2030 — a relatively modest contribution from today, but one expected to grow meaningfully over time as more governance experiments are launched and adoption within the MetaDAO ecosystem deepens.

Summary

In summary, our base case assumptions for MetaDAO are as follows:

- The on-chain fundraising market — including ICOs, IDOs, and other token-based offerings — is projected to grow 5x by 2030, reaching approximately $298bn in total volume.

- MetaDAO’s market share is expected to expand to 10% by 2030, supported by strong early traction, product differentiation (unruggable ICOs and enforceable tokenholder rights), and its growing reputation as a credible on-chain launch venue. Based on these assumptions, we project that the platform will be able to facilitate around 19 ICOs per month in 2030.

- Based on trading data from Umbra and Avici, we estimate an average first-year trading volume of $137m per ICO, nearly 2x higher than Blockworks’ 1-year forward assumption ($65m). We project that this figure will double by 2030, reflecting inflation, the participation of larger LPs, and the addition of external liquidity venues (including potential CEX listings).

- Assuming a linear growth trajectory, approximately 734 ICOs are expected to be launched through the MetaDAO platform between 2026 and 2030, of which roughly 10% (73 projects) are likely to remain active by 2030. For these “mature” tokens, we model an average annual trading volume of $4.1m beyond their launch year, resulting in an additional $305m in cumulative secondary-market trading volume in 2030.

- Applying a 25 bps take rate, we estimate launchpad revenue of $21m (2026) and $161m (2030) under the base case.

- For decision markets, we assume roughly 587 active proposals by 2030, each generating an average trading volume of $289k, or $170m total volume across all markets. With the same 0.25% take rate, this results in an additional $0.42m in protocol revenue by 2030 — modest today, but likely to be readjusted as futarchy-based governance gains traction.

- Combining both revenue streams, we forecast total MetaDAO protocol revenue of ~$162m by 2030 under the base case scenario.

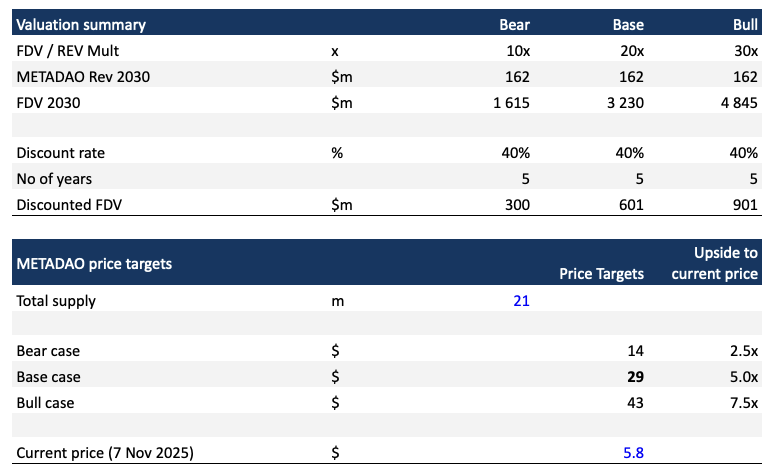

- For valuation purposes, we apply a 20× FDV/Revenue multiple in our base case, consistent with Blockworks’ analysis. In the bear and bull scenarios, we adjust the revenue multiple to 10× and 30×, respectively, while keeping other assumptions constant.

- We then discount these values from 2030 to 2025 using a 40% annual discount rate to reflect execution, competitive, and regulatory risks. The discount factor is (1 + 0.4)^5 = 5.38

Based on all these calculations, we found out that METADAO appeared undervalued across all 3 scenarios:

- Bear case (10x multiple) → implied discounted FDV of $300m, corresponding to a $14 META price target (2.5x upside).

- Base case (20x multiple) → implied discounted FDV of $601m, or a $29 META price target (5.0x upside).

- Bull case (30x multiple) → implied discounted FDV of $901bn, or a $43 META price target (7.5× upside).

Sensitivity Analysis

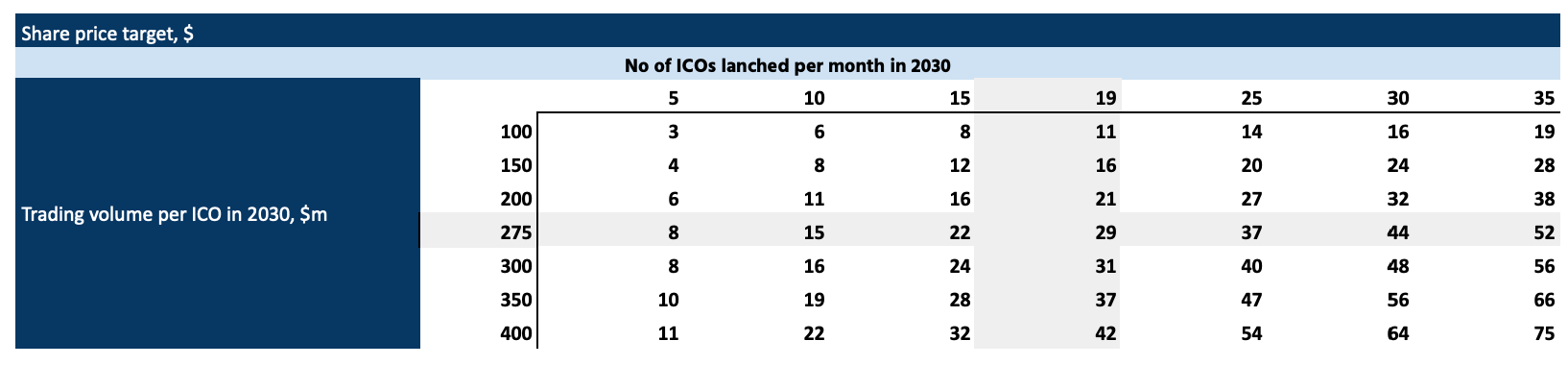

- We stress-tested our valuation model by varying two key inputs — the number of ICOs launched per month in 2030 and the average trading volume per ICO — to evaluate the sensitivity of MetaDAO’s price target under different growth scenarios.

- Under conservative assumptions — with only five ICOs per month in 2030 (in line with MetaDAO’s current launch cadence) and an average trading volume of $100 million per ICO (less than current 1-month volumes) — the model implies a META token price of approximately $3 by 2030, or about 50% below the current market price.

- This highlights that MetaDAO’s valuation is highly sensitive to the number of launches and trading activity — metrics that will be normalizing as the platform gains traction. As the platform matures and more data becomes available, forecast accuracy will improve, but current projections should still be interpreted with caution.

Upside potential

Although all three valuation scenarios already imply a premium to the current market price of META, we view our assumptions as conservative. Below, we outline several upside factors that are not fully reflected in the base case and could meaningfully increase MetaDAO’s fair value over time.

- Number of Launches

Moreover, the team has announced that its top development priority is the introduction of permissionless launches, which will allow any project to initiate an ICO directly on MetaDAO without prior approval. This change is expected to significantly increase launch throughput, lower operational friction, and accelerate network effects by enabling a self-sustaining pipeline of new projects.

- Trading Volume per ICO

As MetaDAO scales, several high-profile launches may emerge with trading volumes many times higher than the median, pushing total platform activity upward.

Currently, MetaDAO’s liquidity is sourced not only from its own Futarchy AMM, but also from external liquidity pools, primarily on Meteora. Over time, additional integrations may be introduced to expand access of new tokens for more investors and increase trading volumes — potentially including centralized exchanges or other third-party liquidity venues.

Additional upside could also come from greater participation by institutional LPs and funds, improved allocation mechanisms, and better handling of oversubscriptions — all of which would support higher liquidity both for ICOs and decision markets.

- Take rate and other fees

- Decision Markets

Institutional “insider” traders could generate substantially higher trading volumes than currently assumed for important decision markets leveraging their governance power in their favour. As futarchy-based governance gains adoption, key governance proposals could drive large, event-driven trading activity, producing periodic spikes far above the conservative averages used in our model.

Risks

- Despite the strong early traction, MetaDAO remains a nascent and experimental project. The product continues to evolve, and the team is actively iterating based on community and projects’ feedback.

- The launchpad currently drives the majority of projected revenues, making the model sensitive to market cycles. A prolonged bear market could reduce fundraising activity and slow new launches.

- All forecasts rely on a limited data set — only seven ICOs in total, with detailed trading data available for just two (Umbra and Avici). More data for new projects could materially shift key inputs and valuation outcomes.

- Competition represents another material risk. The ICO and token launch landscape has become increasingly crowded, with projects such as Sonar, Metaplex Genesis, and Kaito’s Capital Launchpad targeting similar markets. However, MetaDAO’s focus on enforceable tokenholder rights and on-chain governance differentiates it meaningfully from most peers.

Final Thoughts

Futarchy itself remains an ongoing governance experiment, and its long-term evolution is still not fully understood. MetaDAO’s role within this framework could develop in unexpected and fascinating ways, potentially giving rise to new market behaviors and valuation paradigms.

With every new launch, MetaDAO not only drives revenue growth but also deepens its role as a core layer of on-chain capital markets — establishing itself as a distinctive venue where high-quality projects meet engaged long-term investors.

- If you would like to explore our assumptions in more detail, we have attached our calculation model here. We have intentionally left all underlying data visible, so the readers can easily follow our model and understand the logic and data behind our projections.